Question: @ https www.chegg.com homework help/questions-anu-answer analy Chegg Study Textbook Solutions Expert Q&A Study Pack Practice m. Analysis question: Suppose that you are going to construct

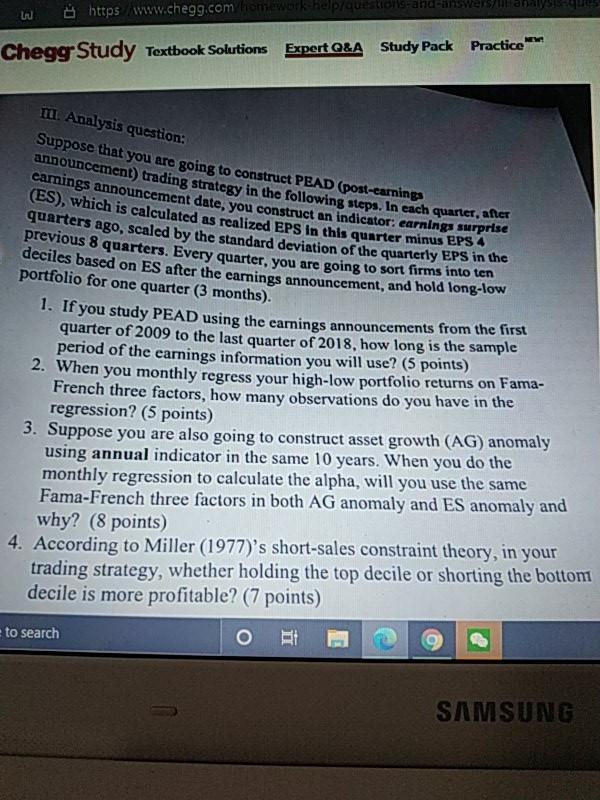

@ https www.chegg.com homework help/questions-anu-answer analy Chegg Study Textbook Solutions Expert Q&A Study Pack Practice m. Analysis question: Suppose that you are going to construct PEAD (post-earnings announcement) trading strategy in the following steps. In each quarter, after eamings announcement date, you construct an indicator: earnings surprise (ES), which is calculated as realized EPS in this quarter minus EPS quarters ago, scaled by the standard deviation of the quarterly EPS in the previous 8 quarters. Every quarter, you are going to sort firms into ten deciles based on ES after the carnings announcement, and hold long-low portfolio for one quarter (3 months). 1. If you study PEAD using the earnings announcements from the first quarter of 2009 to the last quarter of 2018, how long is the sample period of the earnings information you will use? (5 points) 2. When you monthly regress your high-low portfolio returns on Fama- French three factors, how many observations do you have in the regression? (5 points) 3. Suppose you are also going to construct asset growth (AG) anomaly using annual indicator in the same 10 years. When you do the monthly regression to calculate the alpha, will you use the same Fama-French three factors in both AG anomaly and ES anomaly and why? (8 points) 4. According to Miller (1977)'s short-sales constraint theory, in your trading strategy, whether holding the top decile or shorting the bottom decile is more profitable? (7 points) to search SAMSUNG @ https www.chegg.com homework help/questions-anu-answer analy Chegg Study Textbook Solutions Expert Q&A Study Pack Practice m. Analysis question: Suppose that you are going to construct PEAD (post-earnings announcement) trading strategy in the following steps. In each quarter, after eamings announcement date, you construct an indicator: earnings surprise (ES), which is calculated as realized EPS in this quarter minus EPS quarters ago, scaled by the standard deviation of the quarterly EPS in the previous 8 quarters. Every quarter, you are going to sort firms into ten deciles based on ES after the carnings announcement, and hold long-low portfolio for one quarter (3 months). 1. If you study PEAD using the earnings announcements from the first quarter of 2009 to the last quarter of 2018, how long is the sample period of the earnings information you will use? (5 points) 2. When you monthly regress your high-low portfolio returns on Fama- French three factors, how many observations do you have in the regression? (5 points) 3. Suppose you are also going to construct asset growth (AG) anomaly using annual indicator in the same 10 years. When you do the monthly regression to calculate the alpha, will you use the same Fama-French three factors in both AG anomaly and ES anomaly and why? (8 points) 4. According to Miller (1977)'s short-sales constraint theory, in your trading strategy, whether holding the top decile or shorting the bottom decile is more profitable? (7 points) to search SAMSUNG

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts