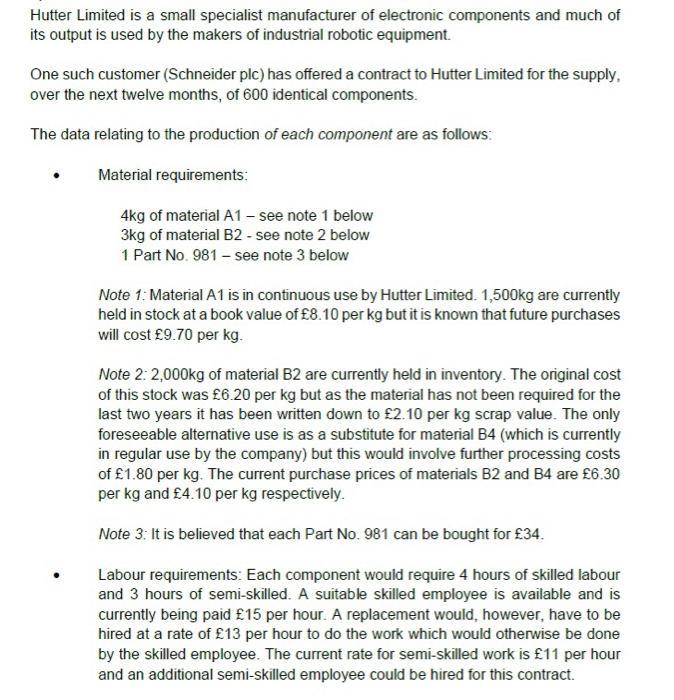

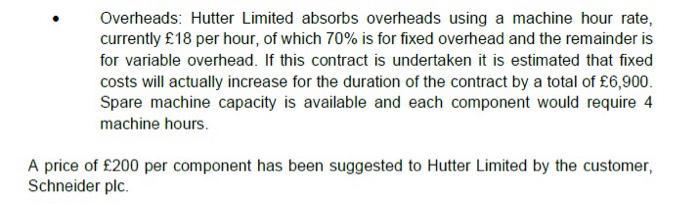

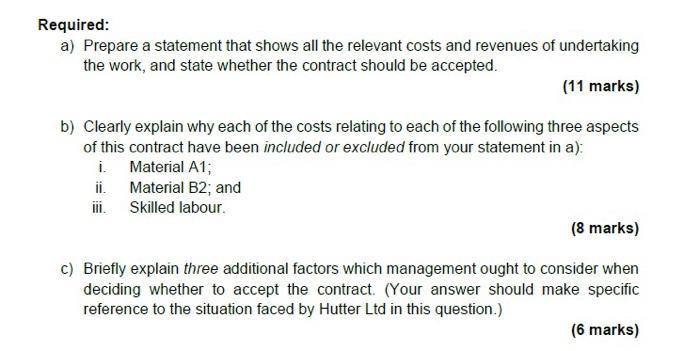

Hutter Limited is a small specialist manufacturer of electronic components and much of its output is...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Solution a Relevant cost for the production of 400 component is Direct Material M1 1200 Kg 55 per Kg ... View the full answer

Related Book For

Posted Date: