Question: (i) (a) State the no-arbitrage principle. (b) Explain why only a few arbitrageurs are required in a market to enforce the no-arbitrage condition (ii) The

(i) (a) State the no-arbitrage principle. (b) Explain why only a few arbitrageurs are required in a market to enforce the no-arbitrage condition

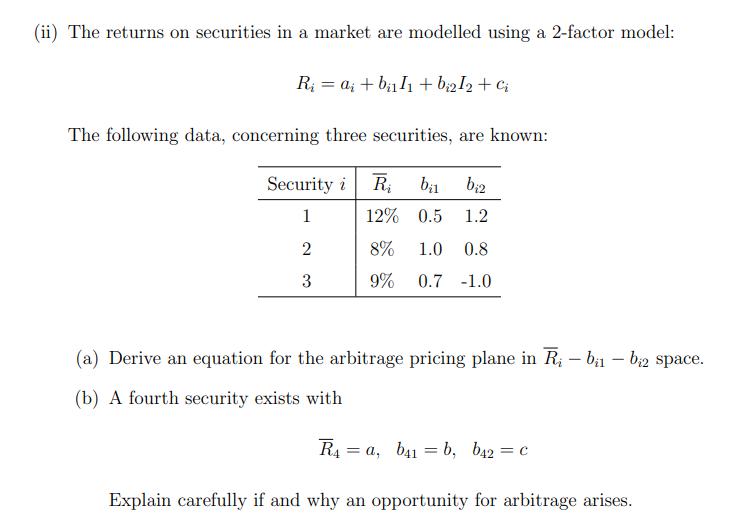

(ii) The returns on securities in a market are modelled using a 2-factor model: Ri=a+b+bi212 + Ci The following data, concerning three securities, are known: Security i Ri Ri bil bi2 1 12% 0.5 1.2 2 8% 1.0 0.8 3 9% 0.7 -1.0 (a) Derive an equation for the arbitrage pricing plane in Ri - bil - bi2 space. (b) A fourth security exists with R4 a, b41b, b42 = c = Explain carefully if and why an opportunity for arbitrage arises.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock