Question: I already know the answer for (a) to (c). Please solve (d) and (e). I wiil definitely upvote. Thank you! = = A liability of

I already know the answer for (a) to (c). Please solve (d) and (e). I wiil definitely upvote. Thank you!

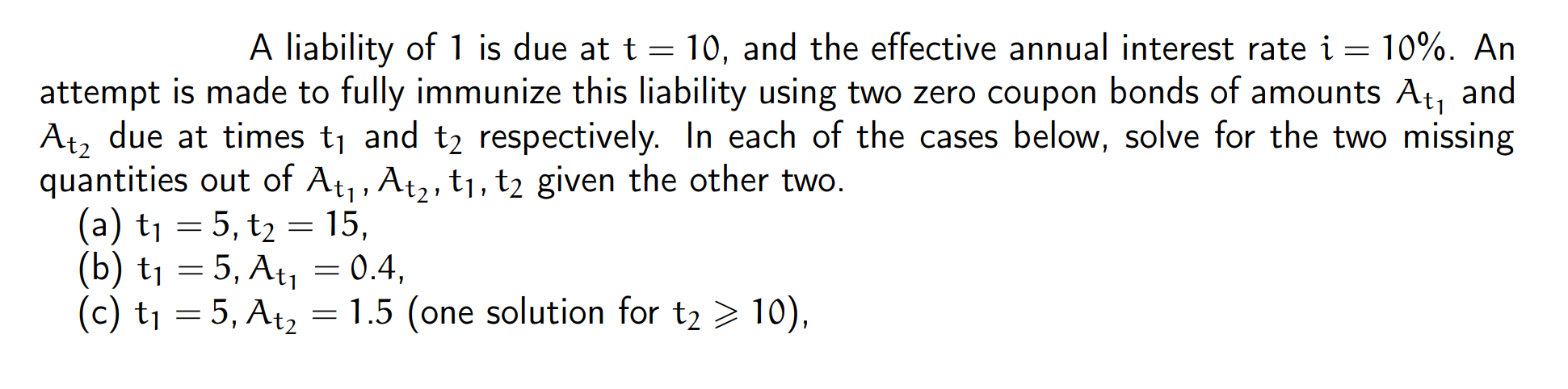

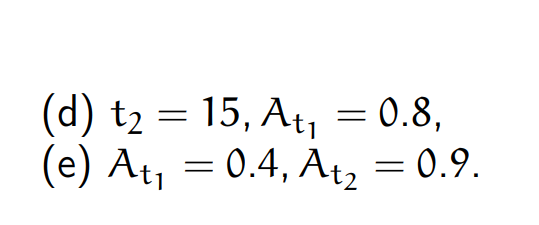

= = A liability of 1 is due at t = 10, and the effective annual interest rate i = 10%. An attempt is made to fully immunize this liability using two zero coupon bonds of amounts At, and Atz due at times tj and t2 respectively. In each of the cases below, solve for the two missing quantities out of At, Atz, t, t2 given the other two. (a) ty = 5, t2 = 15, (b) tj = 5, Aty = 0.4, (c) tj = 5, Atz = 1.5 (one solution for t2 > 10), 1 1 = 1 = 1 = (d) t2 = 15, At = 0.8, (e) Aty = 0.4, Atz = 0.9. e = = = = A liability of 1 is due at t = 10, and the effective annual interest rate i = 10%. An attempt is made to fully immunize this liability using two zero coupon bonds of amounts At, and Atz due at times tj and t2 respectively. In each of the cases below, solve for the two missing quantities out of At, Atz, t, t2 given the other two. (a) ty = 5, t2 = 15, (b) tj = 5, Aty = 0.4, (c) tj = 5, Atz = 1.5 (one solution for t2 > 10), 1 1 = 1 = 1 = (d) t2 = 15, At = 0.8, (e) Aty = 0.4, Atz = 0.9. e = =

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts