Question: I am having difficulty on solving the problem. Could you help me with it? II Constructing Arbitrage Portfolios The following scenario creates arbitrage opportunities for

I am having difficulty on solving the problem. Could you help me with it?

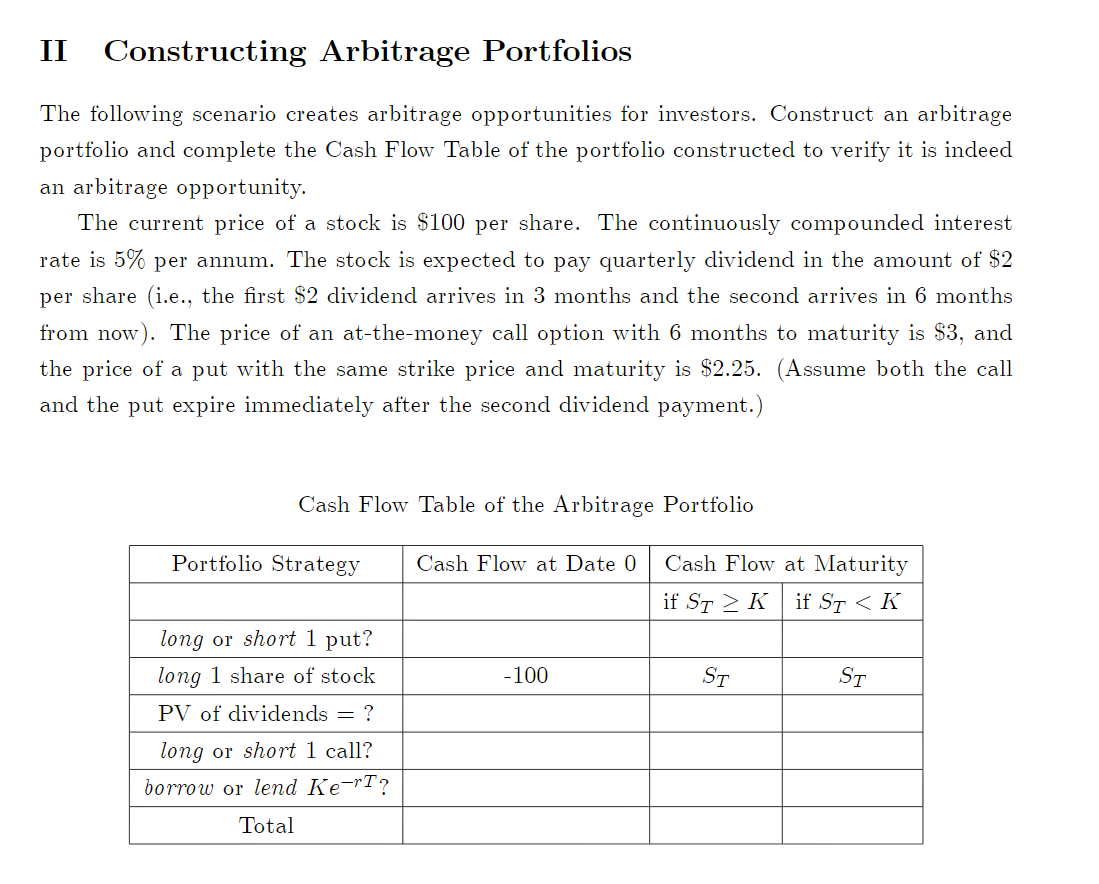

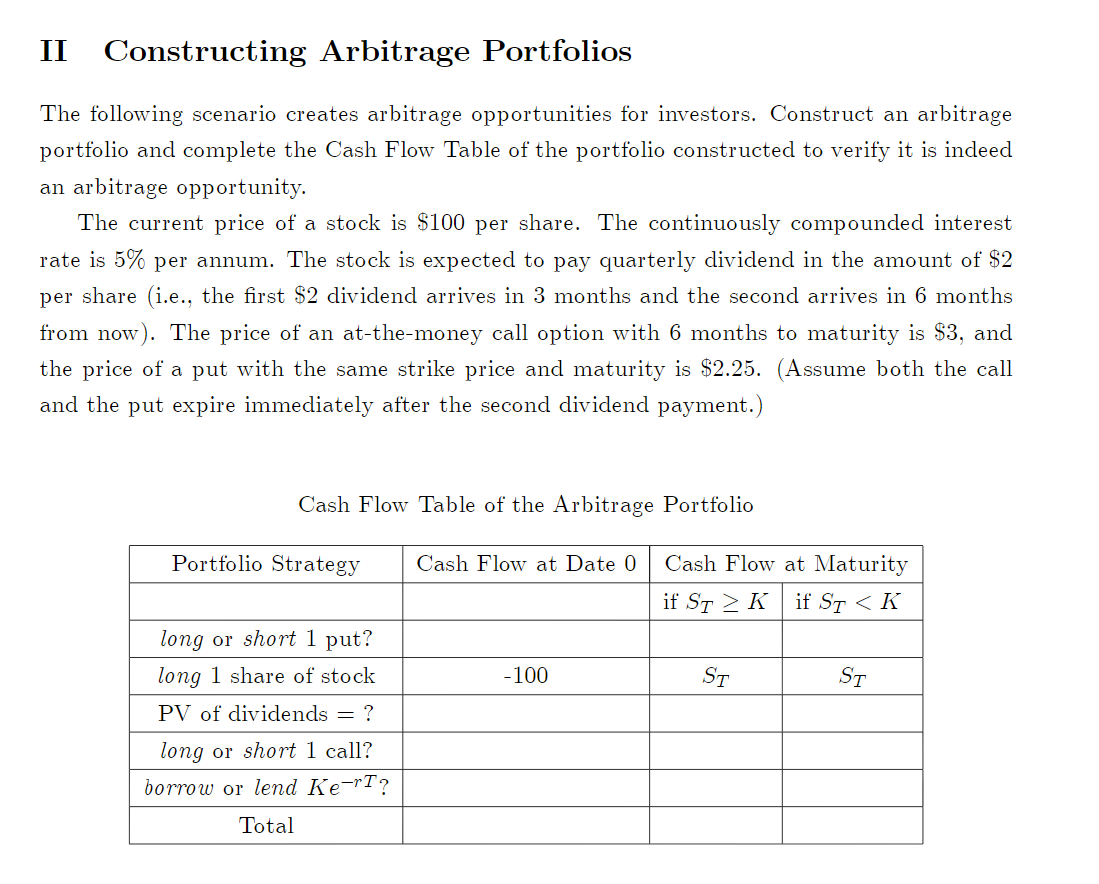

II Constructing Arbitrage Portfolios The following scenario creates arbitrage opportunities for investors. Construct an arbitrage portfolio and complete the Cash Flow Table of the portfolio constructed to verify it is indeed an arbitrage opportunity. The current price of a stock is $100 per share' The continuously compounded interest rate is 5% per annum. The stock is expected to pay quarterly dividend in the amount of $2 per share (i'en the rst $2 dividend arrives in 3 months and the second arrives in 6 months from now). The price of an at-themoney call option with 6 months to maturity is $3, and the price of a put with the same strike price and maturity is $2.25. (Assume both the call and the put expire immediately after the second dividend payment.) Cash Flow Table of the Arbitrage Portfolio Portfolio Strategy Cash Flow at Date 0 Cash Flow at Maturity ifSTZK ifST

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts