Question: I am having trouble with the formula for question E. All others have been solved for and are provided in BOLD: Anne-Marie and Yancy calculate

I am having trouble with the formula for question E. All others have been solved for and are provided in BOLD:

Anne-Marie and Yancy calculate their current living expenditures to be $66,000 a year. During retirement, they plan to take one cruise a year that will cost $5,000 in today's dollars. Anne-Marie estimated that their average tax rate in retirement would be 18 percent. Yancy estimated their Social Security income to be about $21,212 and their retirement benefits are approximately $32,156.

Use this information to answer the following questions:

a. How much income, in today's dollars, will Anne-Marie and Yancy need in retirement assuming 70 percent replacement and an additional $5,000 for the cruise? A: $51,200

b. Assuming the 18 percent income tax estimate during retirement, what is their tax-adjusted need from part a? A: $62,439

c. Calculate their projected annual income shortfall in today's dollars. A: $9,071

d. Determine, in dollars, the future value of the shortfall 33 years from now, assuming an inflation rate of 4 percent. A: $33,095

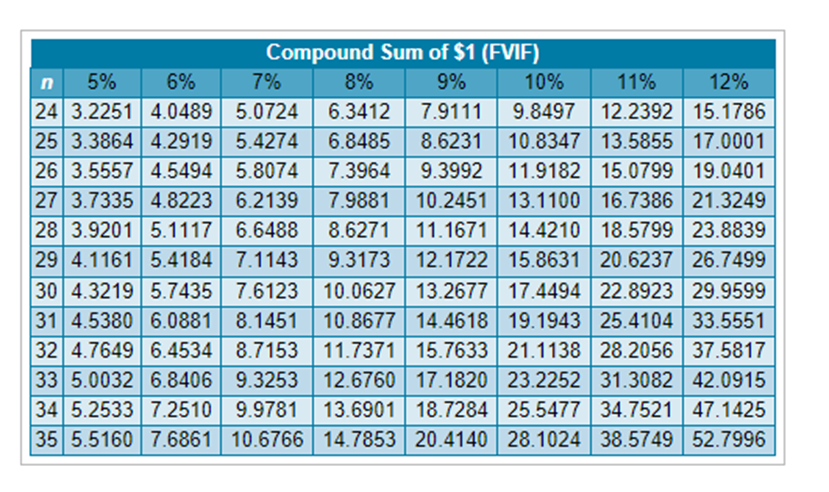

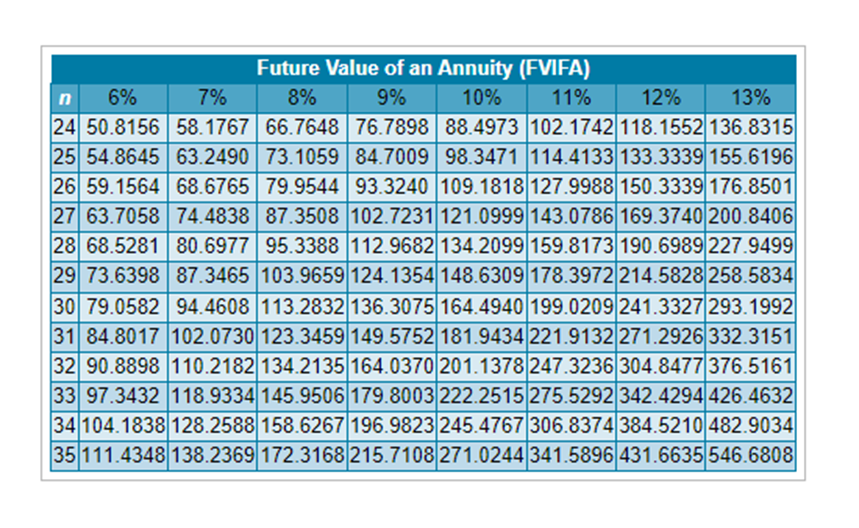

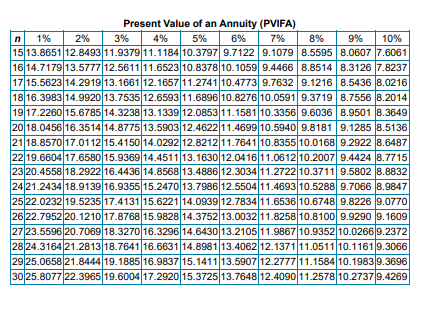

e. Assuming a nominal rate of return of 12 percent and 23 years in retirement, calculate their necessary annual investment to reach their retirement goals. A:???

\begin{tabular}{|c|c|c|c|c|c|c|c|c|} \hline \multicolumn{10}{|c|}{ Compound Sum of \$1 (FVIF) } & & \\ \hline n & 5% & 6% & 7% & 8% & 9% & 10% & 11% & 12% \\ \hline 24 & 3.2251 & 4.0489 & 5.0724 & 6.3412 & 7.9111 & 9.8497 & 12.2392 & 15.1786 \\ \hline 25 & 3.3864 & 4.2919 & 5.4274 & 6.8485 & 8.6231 & 10.8347 & 13.5855 & 17.0001 \\ \hline 26 & 3.5557 & 4.5494 & 5.8074 & 7.3964 & 9.3992 & 11.9182 & 15.0799 & 19.0401 \\ \hline 27 & 3.7335 & 4.8223 & 6.2139 & 7.9881 & 10.2451 & 13.1100 & 16.7386 & 21.3249 \\ \hline 28 & 3.9201 & 5.1117 & 6.6488 & 8.6271 & 11.1671 & 14.4210 & 18.5799 & 23.8839 \\ \hline 29 & 4.1161 & 5.4184 & 7.1143 & 9.3173 & 12.1722 & 15.8631 & 20.6237 & 26.7499 \\ \hline 30 & 4.3219 & 5.7435 & 7.6123 & 10.0627 & 13.2677 & 17.4494 & 22.8923 & 29.9599 \\ \hline 31 & 4.5380 & 6.0881 & 8.1451 & 10.8677 & 14.4618 & 19.1943 & 25.4104 & 33.5551 \\ \hline 32 & 4.7649 & 6.4534 & 8.7153 & 11.7371 & 15.7633 & 21.1138 & 28.2056 & 37.5817 \\ \hline 33 & 5.0032 & 6.8406 & 9.3253 & 12.6760 & 17.1820 & 23.2252 & 31.3082 & 42.0915 \\ \hline 34 & 5.2533 & 7.2510 & 9.9781 & 13.6901 & 18.7284 & 25.5477 & 34.7521 & 47.1425 \\ \hline 35 & 5.5160 & 7.6861 & 10.6766 & 14.7853 & 20.4140 & 28.1024 & 38.5749 & 52.7996 \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|c|c|c|c|c|} \hline \multicolumn{10}{|c|}{ Future Value of an Annuity (FVIFA) } \\ \hline n & 6% & 7% & 8% & 9% & 10% & 11% & 12% & 13% \\ \hline 24 & 50.8156 & 58.1767 & 66.7648 & 76.7898 & 88.4973 & 102.1742 & 118.1552 & 136.8315 \\ \hline 25 & 54.8645 & 63.2490 & 73.1059 & 84.7009 & 98.3471 & 114.4133 & 133.3339 & 155.6196 \\ \hline 26 & 59.1564 & 68.6765 & 79.9544 & 93.3240 & 109.1818 & 127.9988 & 150.3339 & 176.8501 \\ \hline 27 & 63.7058 & 74.4838 & 87.3508 & 102.7231 & 121.0999 & 143.0786 & 169.3740 & 200.8406 \\ \hline 28 & 68.5281 & 80.6977 & 95.3388 & 112.9682 & 134.2099 & 159.8173 & 190.6989 & 227.9499 \\ \hline 29 & 73.6398 & 87.3465 & 103.9659 & 124.1354 & 148.6309 & 178.3972 & 214.5828 & 258.5834 \\ \hline 30 & 79.0582 & 94.4608 & 113.2832 & 136.3075 & 164.4940 & 199.0209 & 241.3327 & 293.1992 \\ \hline 31 & 84.8017 & 102.0730 & 123.3459 & 149.5752 & 181.9434 & 221.9132 & 271.2926 & 332.3151 \\ \hline 32 & 90.8898 & 110.2182 & 134.2135 & 164.0370 & 201.1378 & 247.3236 & 304.8477 & 376.5161 \\ \hline 33 & 97.3432 & 118.9334 & 145.9506 & 179.8003 & 222.2515 & 275.5292 & 342.4294 & 426.4632 \\ \hline 34 & 104.1838 & 128.2588 & 158.6267 & 196.9823 & 245.4767 & 306.8374 & 384.5210 & 482.9034 \\ \hline 35 & 111.4348 & 138.2369 & 172.3168 & 215.7108 & 271.0244 & 341.5896 & 431.6635 & 546.6808 \\ \hline \end{tabular} Present Value of an Annuity (PVIFA) \begin{tabular}{|c|c|c|c|c|c|c|c|c|c|c|} \hline n & 1% & 2% & 3% & 4% & 5% & 6% & 7% & 8% & 9% & 10% \\ \hline 15 & 13.8651 & 12.8493 & 11.9379 & 11.1184 & 10.3797 & 9.7122 & 9.1079 & 8.5595 & 8.0607 & 7.6061 \\ \hline 16 & 14.7179 & 13.5777 & 12.5611 & 11.6523 & 10.8378 & 10.1059 & 9.4466 & 8.8514 & 8.3126 & 7.8237 \\ \hline 17 & 15.5623 & 14.2919 & 13.1661 & 12.1657 & 11.2741 & 10.4773 & 9.7632 & 9.1216 & 8.5436 & 8.0216 \\ \hline 18 & 16.3983 & 14.9920 & 13.7535 & 12.6593 & 11.6896 & 10.8276 & 10.0591 & 9.3719 & 8.7556 & 8.2014 \\ \hline 19 & 17.2260 & 15.6785 & 14.3238 & 13.1339 & 12.0853 & 11.1581 & 10.3356 & 9.6036 & 8.9501 & 8.3649 \\ \hline 20 & 18.0456 & 16.3514 & 14.8775 & 13.5903 & 12.4622 & 11.4699 & 10.5940 & 9.8181 & 9.1285 & 8.5136 \\ \hline 21 & 18.8570 & 17.0112 & 15.4150 & 14.0292 & 12.8212 & 11.7641 & 10.8355 & 10.0168 & 9.2922 & 8.6487 \\ \hline 22 & 19.6604 & 17.6580 & 15.9369 & 14.4511 & 13.1630 & 12.0416 & 11.0612 & 10.2007 & 9.4424 & 8.7715 \\ \hline 23 & 20.4558 & 18.2922 & 16.4436 & 14.8568 & 13.4886 & 12.3034 & 11.2722 & 10.3711 & 9.5802 & 8.8832 \\ \hline 24 & 21.2434 & 18.9139 & 16.9355 & 15.2470 & 13.7986 & 12.5504 & 11.4693 & 10.5288 & 9.7066 & 8.9847 \\ \hline 25 & 22.0232 & 19.5235 & 17.4131 & 15.6221 & 14.0939 & 12.7834 & 11.6536 & 10.6748 & 9.8226 & 9.0770 \\ \hline 26 & 22.7952 & 20.1210 & 17.8768 & 15.9828 & 14.3752 & 13.0032 & 11.8258 & 10.8100 & 9.9290 & 9.1609 \\ \hline 27 & 23.5596 & 20.7069 & 18.3270 & 16.3296 & 14.6430 & 13.2105 & 11.9867 & 10.9352 & 10.0266 & 9.2372 \\ \hline 28 & 24.3164 & 21.2813 & 18.7641 & 16.6631 & 14.8981 & 13.4062 & 12.1371 & 11.0511 & 10.1161 & 9.3066 \\ \hline 29 & 25.0658 & 21.8444 & 19.1885 & 16.9837 & 15.1411 & 13.5907 & 12.2777 & 11.1584 & 10.1983 & 9.3696 \\ \hline 30 & 25.8077 & 22.3965 & 19.6004 & 17.2920 & 15.3725 & 13.7648 & 12.4090 & 11.2578 & 10.2737 & 9.4269 \\ \hline \end{tabular}

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts