Question: I am not having issues answering the problems but on how to cite them correctly. I am not sure of the paragraph number and would

I am not having issues answering the problems but on how to cite them correctly. I am not sure of the paragraph number and would like them check. Do I include the Note as a paragraph? Do I go by definitions as paragraphs?

1. Access the glossary (Master Glossary) to answer the following.

(a) What are cash equivalents?

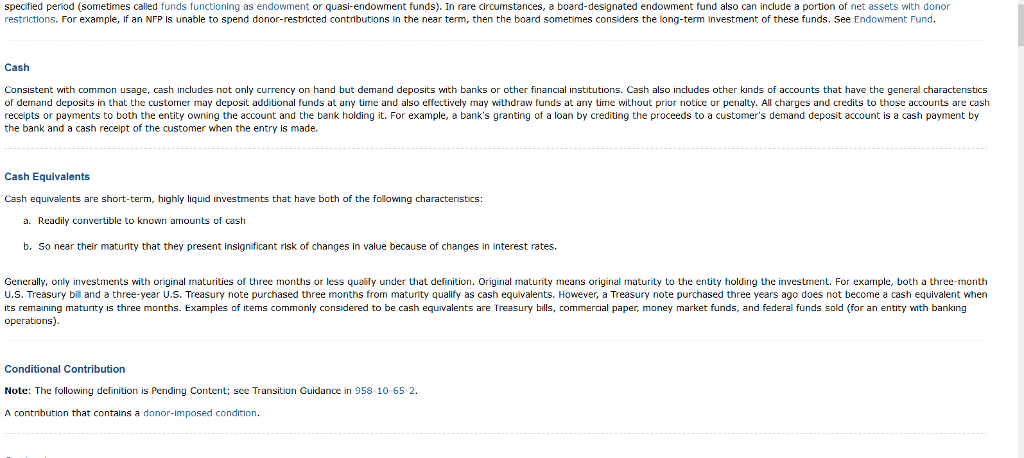

Cash equivalents are short-term, highly liquid investments that have both of the following characteristics:

a. Readily convertible to known amounts of cash

b. So near their maturity that they present insignificant risk of changes in value because of changes in interest rates

(FASB 230-10-20-5)

(b) What are financing activities?

Financing activities include obtaining resources from owners and providing them with a return on, and a return of, their investment; receiving restricted resources that by donor stipulation must be used for long-term purposes; borrowing money and repaying amounts borrowed, or otherwise settling the obligation; and obtaining and paying for other resources obtained from creditors on long-term credit (FASB 230-10-20-16).

(c) What are investing activities?

(d) What are operating activities?.

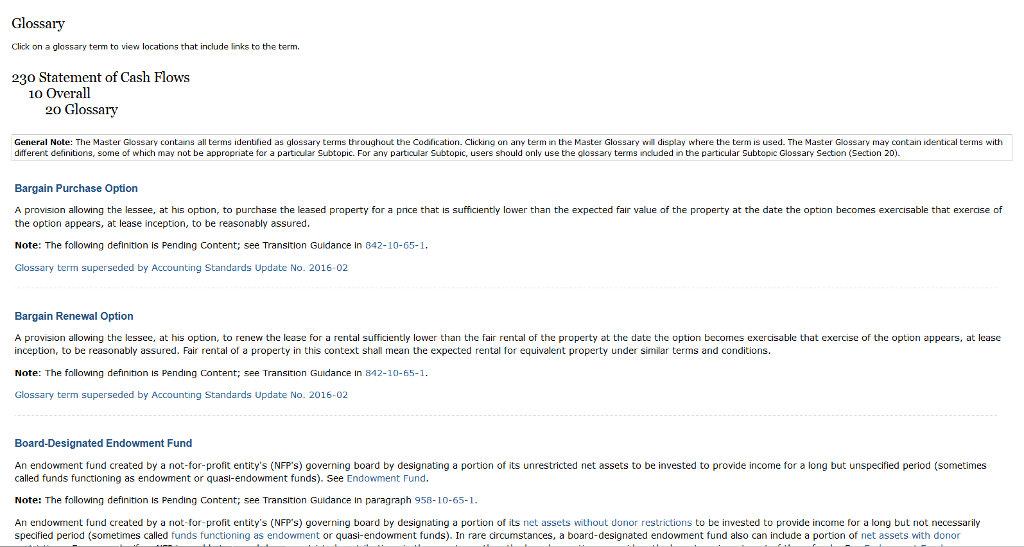

Glossary Click on a glossary term to view locations that include Iinks to the term. 230 Statement of Cash Flows 10 Overall 20 Glossary General Note: The Master Glossary contains all terms identified as glossary terms throughout the Codification. Clicking on any term in the Master Glossary wl display where the term is used. The Master Glossary may contain identical terms with different definitions, some of which may not be appropriate for a particular Subtopic. For any particular Subtopic, users should only use the glossary terms indluded in the particular Subtopic Glossary Section (Section 20). Bargain Purchase Option A provision allowing the lessee, at his option, to purchase the leased property for a price that is sufficiently lower than the expected fair value of the property at the date the option becomes exercisable that exercise of the option appears, at lease inception, to be reasonably assured. Note: The following definition is Pending Content; see Transition Guidance in 842-10-65-1. Glossary term superseded by Accounting Standards Update No. 2016-02 Bargain Renewal Option A provision allowing the lessee, at his option, to renew the lease for a rental sufficiently lower than the fair rental of the property at the date the option becomes exercisable that exercise of the option appears, at lease inception, to be reasonably assured. Fair rental of a property in this context shall mean the expected rental for equivalent property under similar terms and conditions. Note: The following definition is Pending Content; see Transition Guidance in 842-10-65-1 Glossary term superseded by Accounting Standards Update No. 2016-02 Board-Designated Endowment Fund An endowment fund created by a not-for-profit entity's (NFP's) governing board by designating a portion of its unrestricted net assets to be invested to provide income for a long but unspecified period (sometimes called funds functioning as endowment or quasi-endowment funds). See Endowment Fund. Note: The following definition is Pending Content; see Transition Guidance in paragraph 958-10-65-1 An endowment fund created by a not-for-profit entity's (NFP's)governing board by designating a portion of its net assets without donor restrictions to be invested to provide income for a long but not necessarily specified period (sometimes called funds functioning as endowment or quasi-endowment funds). In rare circumstances, a board-designated endowment fund also can include a portion of net assets with donor

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts