Question: I am unsure how to answer question e as there are two variable changes. In each of the following, you are given two options with

I am unsure how to answer question e as there are two variable changes.

I am unsure how to answer question e as there are two variable changes.

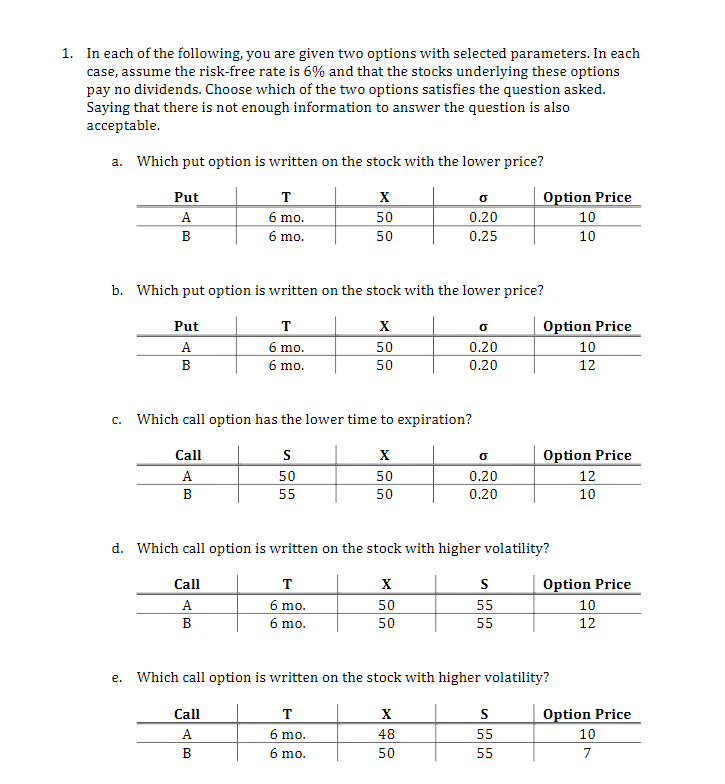

In each of the following, you are given two options with selected parameters. In each case, assume the risk-free rate is 6% and that the stocks underlying these options pay no dividends. Choose which of the two options satisfies the question asked. Saying that there is not enough information to answer the question is also acceptable. 1. Which put option is written on the stock with the lower price? a. Option Price Put X 6 mo 50 0.20 10 6 mo. 50 0.25 10 b. Which put option is written on the stock with the lower price? Put Option Price 6 mo A 50 0.20 10 6 mo 50 0.20 12 Which call option has the lower time to expiration? C. Option Price Call X A 50 50 0.20 12 55 50 0.20 10 d. Which call option is written on the stock with higher volatility? Call Option Price 6 mo A 50 55 10 6 mo 50 55 12 Which call option is written on the stock with higher volatility? e. Option Price Call 6 mo 48 55 10 6 mo. 50 55 7 Ln In each of the following, you are given two options with selected parameters. In each case, assume the risk-free rate is 6% and that the stocks underlying these options pay no dividends. Choose which of the two options satisfies the question asked. Saying that there is not enough information to answer the question is also acceptable. 1. Which put option is written on the stock with the lower price? a. Option Price Put X 6 mo 50 0.20 10 6 mo. 50 0.25 10 b. Which put option is written on the stock with the lower price? Put Option Price 6 mo A 50 0.20 10 6 mo 50 0.20 12 Which call option has the lower time to expiration? C. Option Price Call X A 50 50 0.20 12 55 50 0.20 10 d. Which call option is written on the stock with higher volatility? Call Option Price 6 mo A 50 55 10 6 mo 50 55 12 Which call option is written on the stock with higher volatility? e. Option Price Call 6 mo 48 55 10 6 mo. 50 55 7 Ln

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts