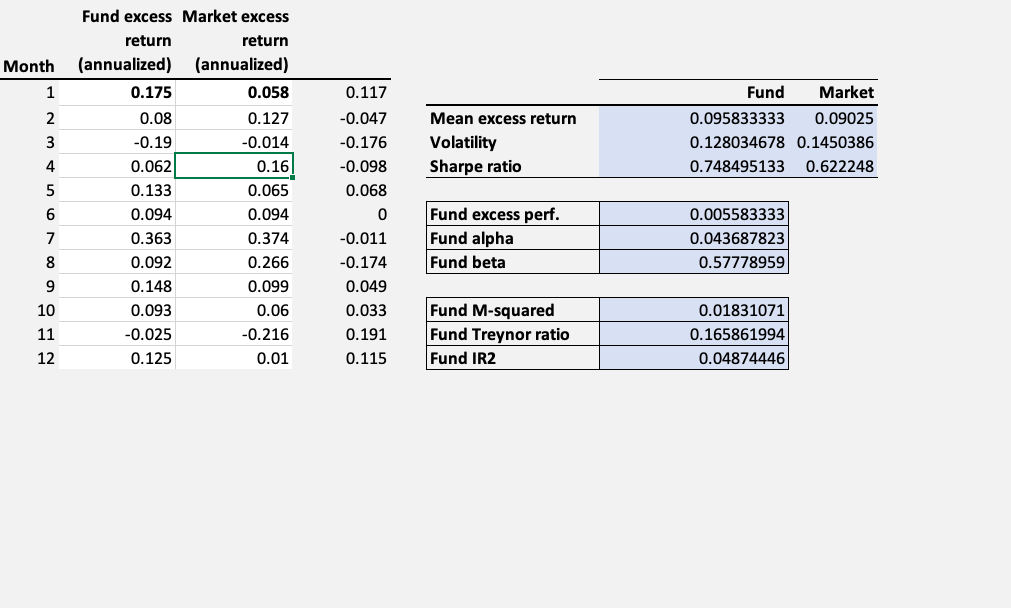

Question: I cannot figure out what I am doing wrong for the Fund-M sqared, Fund Treynor ratio or Fund IR2 Month 1 0.117 2 Fund Market

I cannot figure out what I am doing wrong for the Fund-M sqared, Fund Treynor ratio or Fund IR2

I cannot figure out what I am doing wrong for the Fund-M sqared, Fund Treynor ratio or Fund IR2

Month 1 0.117 2 Fund Market 0.095833333 0.09025 0.128034678 0.1450386 0.748495133 0.622248 Mean excess return Volatility Sharpe ratio 3 4 5 6 Fund excess Market excess return return (annualized) (annualized) 0.175 0.058 0.08 0.127 -0.19 -0.014 0.062 0.16 0.133 0.065 0.094 0.094 0.363 0.374 0.092 0.266 0.148 0.099 0.093 0.06 -0.025 -0.216 0.125 0.01 7 -0.047 -0.176 -0.098 0.068 0 -0.011 -0.174 0.049 0.033 0.191 0.115 Fund excess perf. Fund alpha Fund beta 0.005583333 0.043687823 0.57778959 8 9 10 11 Fund M-squared Fund Treynor ratio Fund IR2 0.01831071 0.165861994 0.04874446 12

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts