Question: I can't figure out how to do the adjusted basis. Please help me on the circled ones. Thank you. Problem 9-22 (Algorithmic) (LO. 2) On

I can't figure out how to do the adjusted basis. Please help me on the circled ones. Thank you.

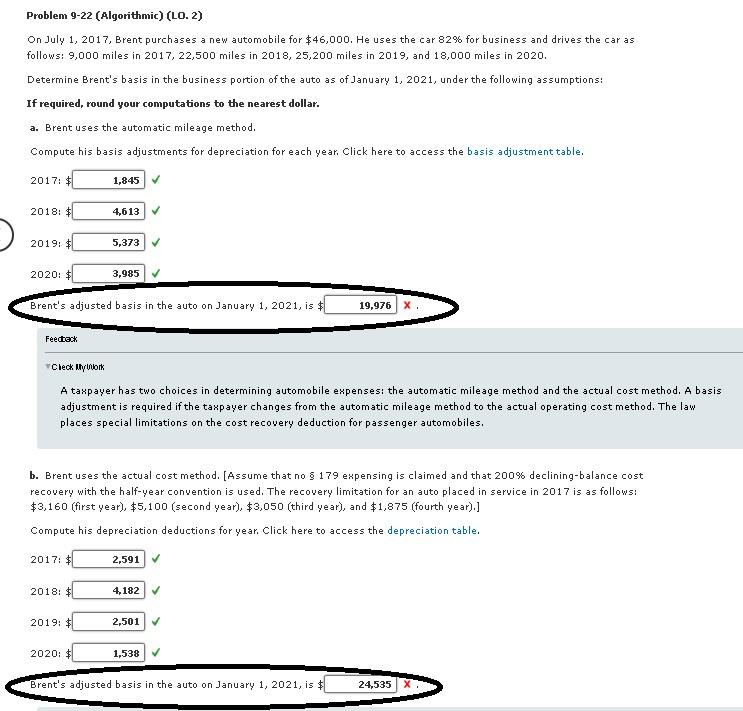

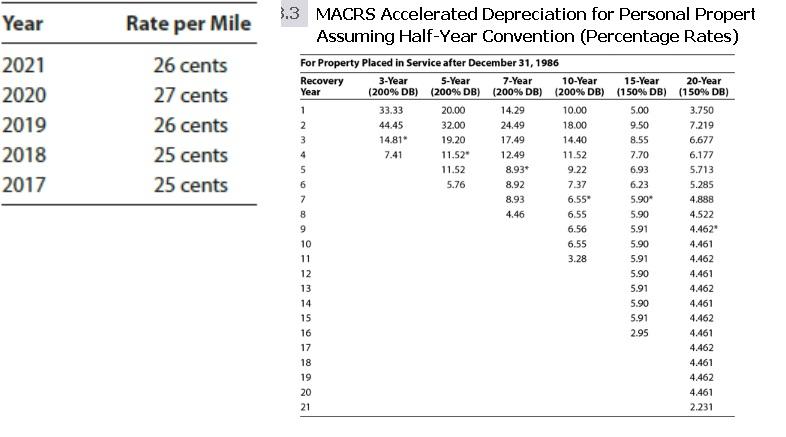

Problem 9-22 (Algorithmic) (LO. 2) On July 1, 2017, Brent purchases a new automobile for $46,000. He uses the car 82% for business and drives the car as follows: 9,000 miles in 2017, 22,500 miles in 2018, 25,200 miles in 2019, and 18,000 miles in 2020. Determine Brent's basis in the business portion of the auto as of January 1, 2021, under the following assumptions: If required, round your computations to the nearest dollar. a. Brent uses the automatic mileage method. Compute his basis adjustments for depreciation for each year. Click here to access the basis adjustment table. 2017: $ 2018: $ 2019: $ 2020: $ Feedback Brent's adjusted basis in the auto on January 1, 2021, is $ 2017: $ 1,845 2018: $ 4,613 2019: $ 5,373 Check My Work A taxpayer has two choices in determining automobile expenses: the automatic mileage method and the actual cost method. A basis adjustment is required if the taxpayer changes from the automatic mileage method to the actual operating cost method. The law places special limitations on the cost recovery deduction for passenger automobiles. 2020: $ 3,985 b. Brent uses the actual cost method. [Assume that no 179 expensing is claimed and that 200% declining-balance cost recovery with the half-year convention is used. The recovery limitation for an auto placed in service in 2017 is as follows: $3,160 (first year), $5,100 (second year), $3,050 (third year), and $1,875 (fourth year).] Compute his depreciation deductions for year. Click here to access the depreciation table. 2,591 4,182 2,501 19,976 X. 1,538 Brent's adjusted basis in the auto on January 1, 2021, is $ 24,535 X Year 2021 2020 2019 2018 2017 Rate per Mile 26 cents 27 cents 26 cents 25 cents 25 cents 3.3 MACRS Accelerated Depreciation for Personal Propert Assuming Half-Year Convention (Percentage Rates) For Property Placed in Service after December 31, 1986 3-Year 5-Year (200% DB) (200 % DB) Recovery Year 1 2 3 4 5 6 7 8 9 10 11 12 13 14 S61898 15 17 20 21 33.33 44.45 14.81* 7.41 20.00 32.00 19.20 11.52" 11.52 5.76 7-Year (200 % DB) 14.29 24.49 17.49 12.49 8.93* 8.92 8.93 4.46 10-Year (200 % DB) 10.00 18.00 14.40 11.52 9.22 7.37 6.55* 6.55 6.56 6.55 3.28 15-Year (150 % DB) 5.00 9.50 8.55 7.70 6.93 6.23 5.90* 5.90 5.91 5.90 5.91 5.90 5.91 5.90 5.91 2.95 20-Year (150% DB) 3.750 7.219 6.677 6.177 5.713 5.285 4.888 4.522 4.462" 4.461 4.462 4.461 4.462 4.461 4.462 4.461 4.462 4.461 4.462 4.461 2.231

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts