Question: I got 21.92-0.32 (xt-1) which is incorrect. can someone please provide the answers for all the questions with an explanation. thanks in advance The data

I got 21.92-0.32 (xt-1) which is incorrect. can someone please provide the answers for all the questions with an explanation. thanks in advance

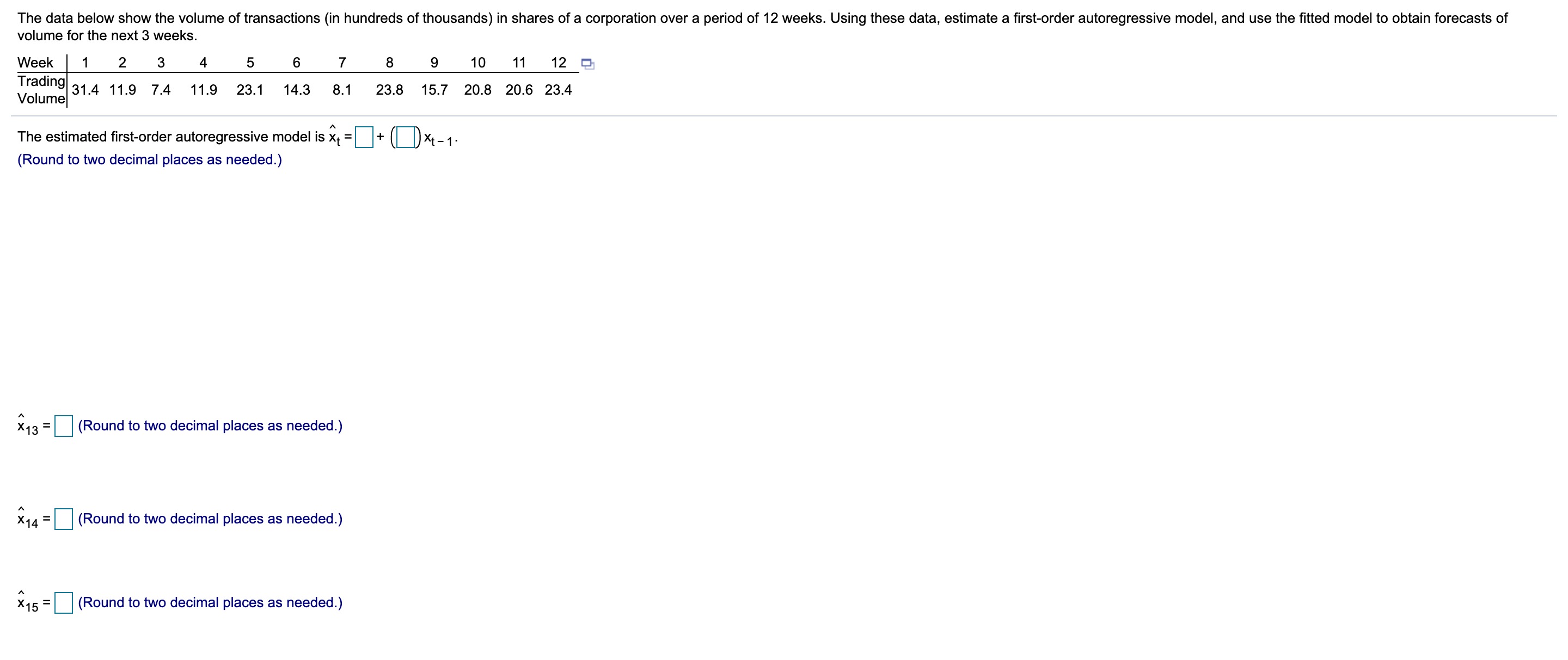

The data below show the volume of transactions (in hundreds at thousands) in shares ofa corporation over a period of 12 weeks. Using these data, estimate a rst-order autoregressive model, and use the tted model to obtain forecasts of volume for the next 3 weeks. Week I 1 2 3 4 5 6 T 8 9 10 11 12 D dem 31.4 11.9 7.4 11.9 23.1 14.3 5.1 23.3 15.7 20.8 20.6 23.4 Volume The estimated first-order autoregressive model is :1 = + | art, 1. (Round to two decimal places as needed.) x13 = (Round to two decimal places as needed.) x14 = (Round to two decimal places as needed.) x15 = (Round to two decimal places as needed.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts