Question: I got the wrong answer to part A and I don't know why. If you could supply the answers to parts A-D that would be

I got the wrong answer to part A and I don't know why. If you could supply the answers to parts A-D that would be appreciated. Also, please write the solutions so I can see where I went wrong and how to do the problems myself in the future. Thank you.

I got the wrong answer to part A and I don't know why. If you could supply the answers to parts A-D that would be appreciated. Also, please write the solutions so I can see where I went wrong and how to do the problems myself in the future. Thank you.

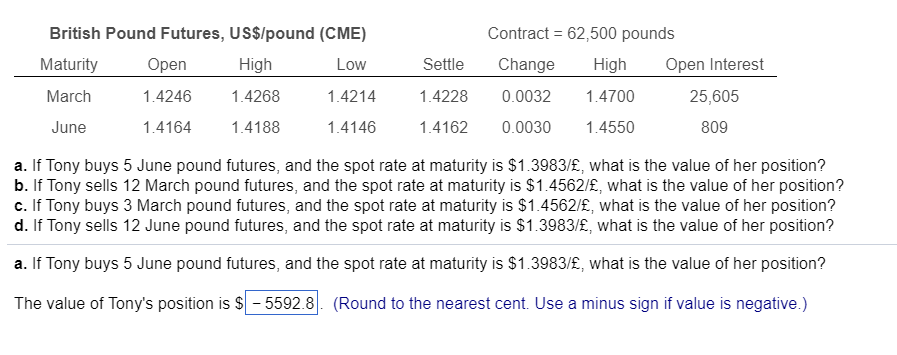

British Pound Futures, USS/pound (CME) Maturity Open High Contract- 62,500 pounds Settle Change High Open Interest 25,605 809 Low March 1.4246 1.4268 1.42141.42280.0032 1.4700 June 1.41641.4188 1.4146 1.4162 0.0030 1.4550 a. If Tony buys 5 June pound futures, and the spot rate at maturity is $1.3983/E, what is the value of her position? b. If Tony sells 12 March pound futures, and the spot rate at maturity is $1.4562/E, what is the value of her position? c. If Tony buys 3 March pound futures, and the spot rate at maturity is $1.4562/E, what is the value of her position? d. If Tony sells 12 June pound futures, and the spot rate at maturity is $1.3983/E, what is the value of her position? a. If Tony buys 5 June pound futures, and the spot rate at maturity is $1.3983/E, what is the value of her position'? The value of Tony's position is S-5592.8. (Round to the nearest cent. Use a minus sign if value is negative.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts