Question: I have a question about CDO's from asset backed securities . Below i will provide context to my question with picture. I have no idea

I have a question about CDO's from asset backed securities Below i will provide context to my question with picture. I have no idea how i can calculate losses in different tranches. Below is an example of a mezzanine CDO, how would i go about calculation losses in the tranches?

Assets Are divided between senior tranche AAA Mezzanine tranche BBB Equity tranche not rated

Then this BBB mezzanine tranche is divided into: senior tranche AAA mezzanine tranche BBB and an equity tranche

the picture i added has the answers, Thanks in advance!

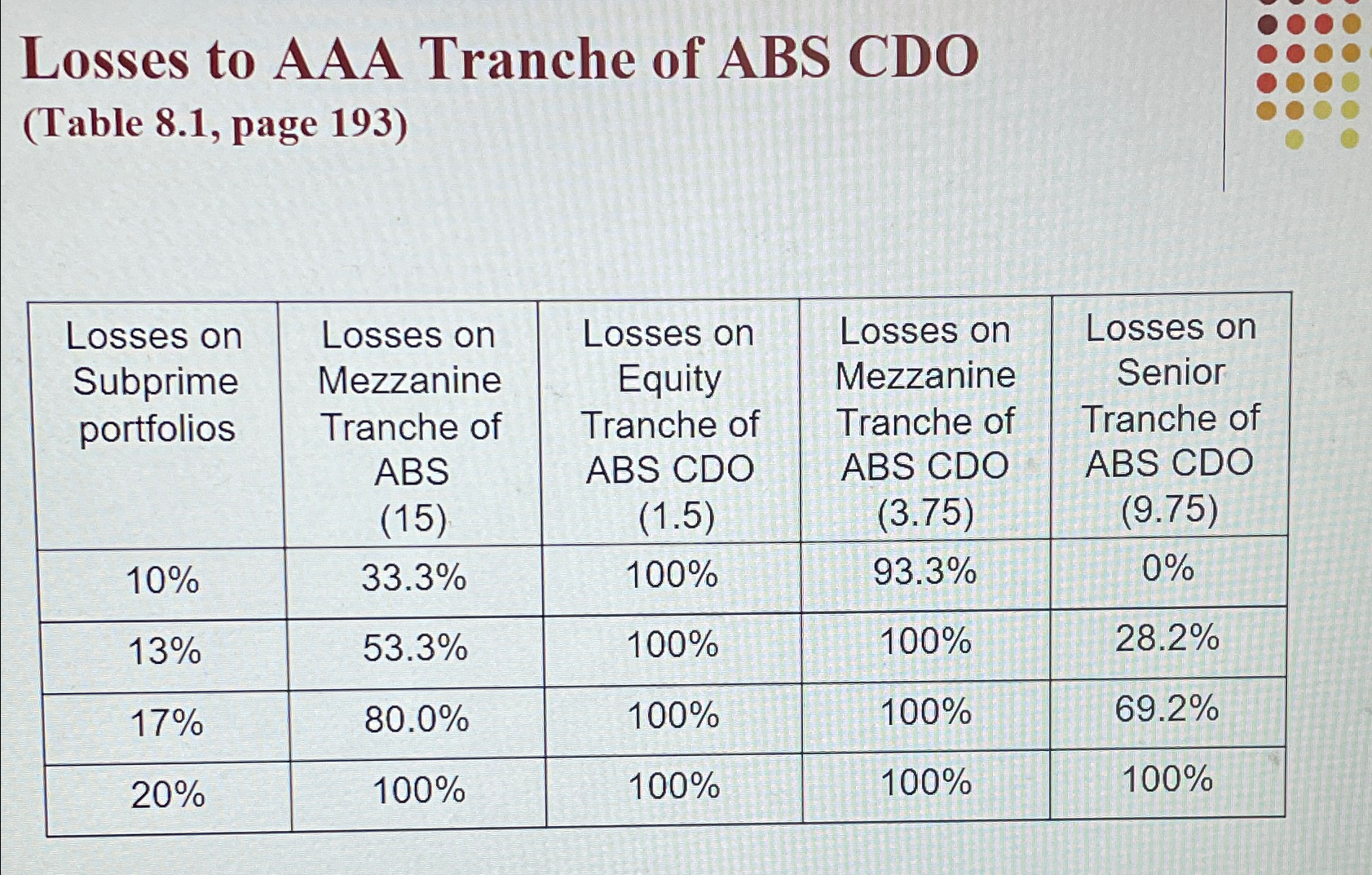

Losses to AAA Tranche of ABS CDO

Table page

tabletableLosses onSubprimeportfoliostableLosses onMezzanineTranche ofABShanks in advance!

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock