Question: I have a solution for the question, but I don't know how to get those numbers. Like, how do I get 1,800? I need a

I have a solution for the question, but I don't know how to get those numbers. Like, how do I get 1,800?

I need a detailed step-by-step solution.

Question:

You have been asked by the accountant of Charlton Ltd to prepare the tax-effect accounting adjustments for the year ended 30 June 2023. Investigations revealed the following information.

- In September 2021, the Australian government reduced the company tax rate from 40 cents to 30 cents in the dollar, effective from 1 July 2022.

- The profit for the year ended 30 June 2023 was $1 350 000.

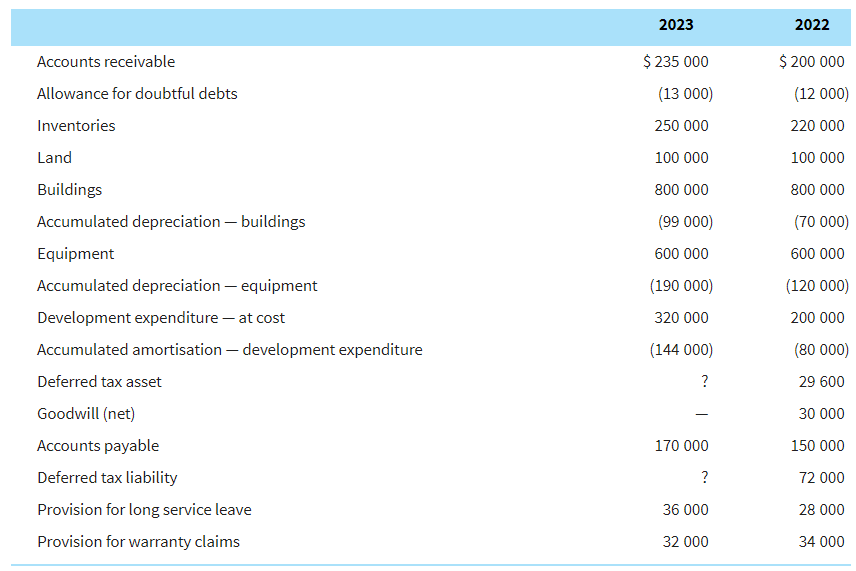

- The assets and liabilities at 30 June 2022 and 30 June 2023 were:

- The company is entitled to claim a tax deduction of 125% for development expenditure in the year of expenditure. The company has adopted the accounting policy of capitalising and then amortising the expenditure over five years.

- Revenue for the year included:

- Expenses brought to account included:

- Accumulated depreciation on equipment for tax purposes was $180 000 on 30 June 2022, and $285 000 on 30 June 2023.

- Bad debts of $14 000 were written off during the year, and warranty repairs to the value of $22 000 were carried out. There was no tax deduction for long service leave in the current year.

- Buildings are depreciated in the accounting records but no deduction is allowed for tax purposes.

Required

Prepare the journal entry to account for the change in the income tax rate announced by the Australian Government in September 2021

Answer:

Change in tax rate

Deferred tax liability Dr 18 000

Deferred tax asset Cr 7 400

Income tax expense Cr 10 600

(Recognition of change of tax rate)

DTA DTL

Opening balance $29 600 $72 000

Adjustment for change in tax rate: (40% - 30%) / 40% (7 400) (18 000)

$22 200 $54 000

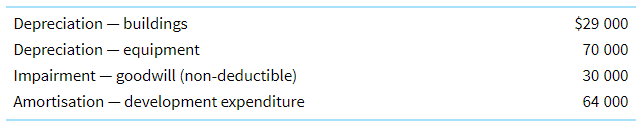

\begin{tabular}{lr} \hline Non-taxable income & $138000 \\ \hline \end{tabular} \begin{tabular}{lr} \hline Depreciation - buildings & $29000 \\ Depreciation - equipment & 70000 \\ Impairment - goodwill (non-deductible) & 30000 \\ Amortisation - development expenditure & 64000 \\ \hline \end{tabular} \begin{tabular}{lr} \hline Non-taxable income & $138000 \\ \hline \end{tabular} \begin{tabular}{lr} \hline Depreciation - buildings & $29000 \\ Depreciation - equipment & 70000 \\ Impairment - goodwill (non-deductible) & 30000 \\ Amortisation - development expenditure & 64000 \\ \hline \end{tabular}

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts