Question: i have not seen a single question using these numbers. let alone a correct answer to part D. Here are some historical data on the

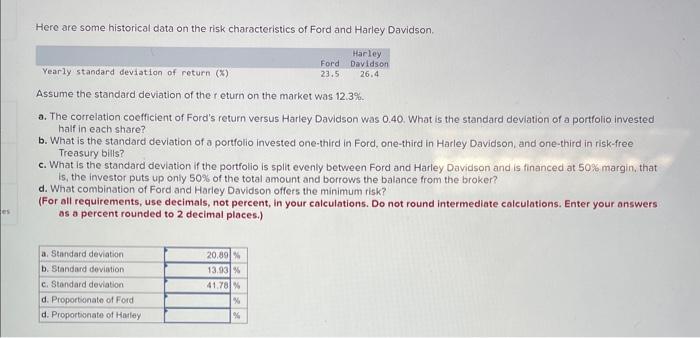

Here are some historical data on the risk characteristics of Ford and Harley Davidson. Assume the standard deviation of the r eturn on the market was 12.3%. a. The correlation coefficient of Ford's return versus Harley Davidson was 0.40. What is the standard deviation of a portfolio invested half in each share? b. What is the standard deviation of a portfolio invested one-third in Ford, one-third in Harley Davidson, and one-third in risk-free Treasury bills? c. What is the standard deviation if the portfolio is split evenly between Ford and Harley Davidson and is financed at 50% margin, that is, the investor puts up only 50% of the total amount and borrows the balance from the broker? d. What combination of Ford and Harley Davidson offers the minimum risk? (For all requirements, use decimals, not percent, in your calculations. Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal places.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts