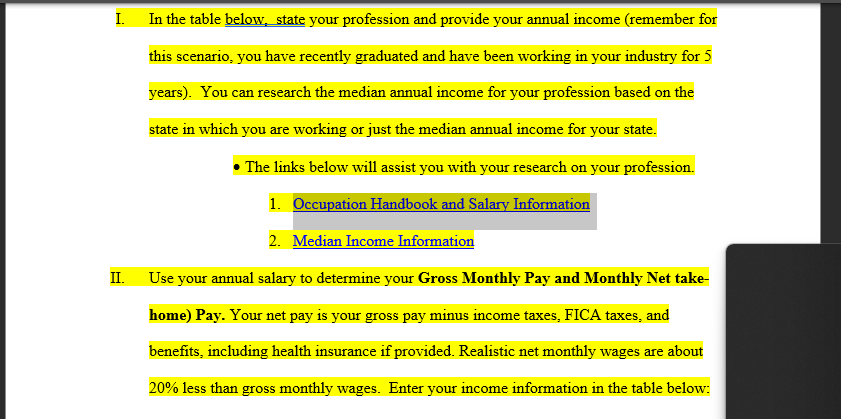

Question: I. In the table below, state your profession and provide your annual income (remember for this scenario, you have recently graduated and have been working

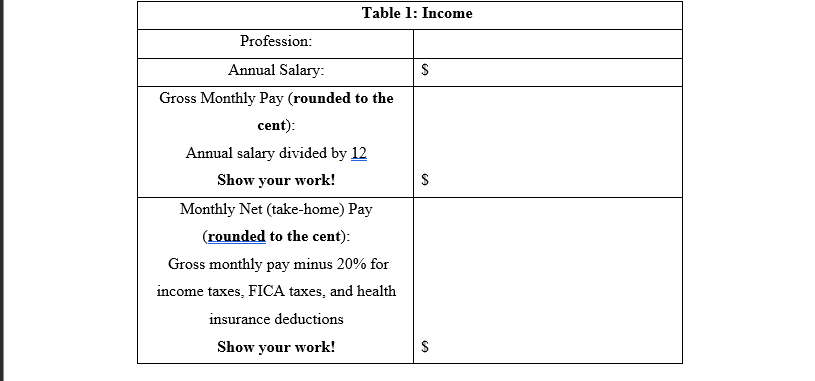

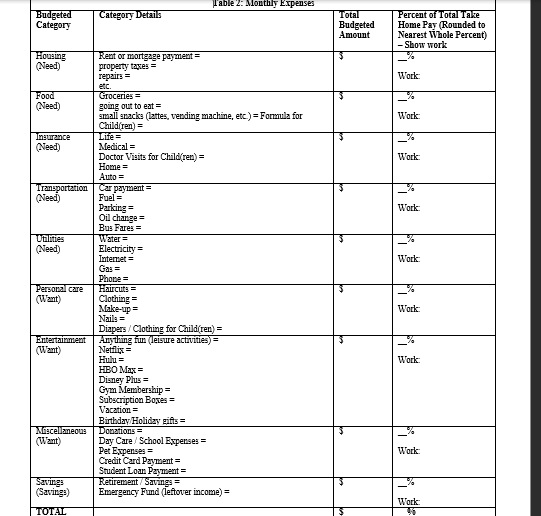

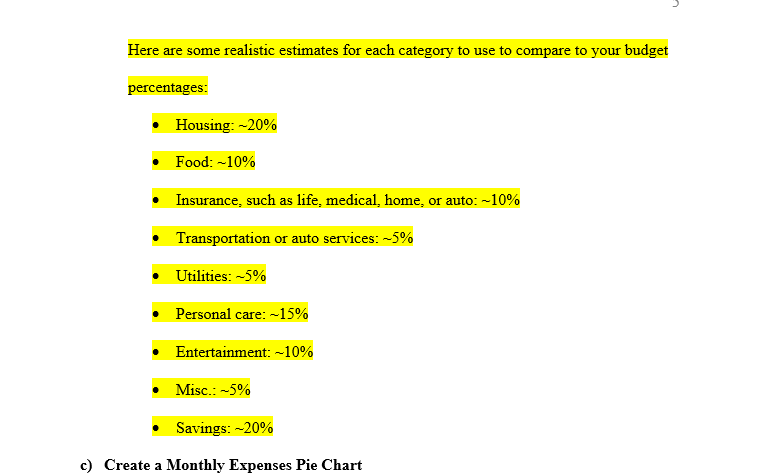

I. In the table below, state your profession and provide your annual income (remember for this scenario, you have recently graduated and have been working in your industry for 5 years). You can research the median annual income for your profession based on the state in which you are working or just the median annual income for your state. . The links below will assist you with your research on your profession. 1. Occupation Handbook and Salary Information 2. Median Income Information II. Use your annual salary to determine your Gross Monthly Pay and Monthly Net take- home) Pay. Your net pay is your gross pay minus income taxes, FICA taxes, and benefits, including health insurance if provided. Realistic net monthly wages are about 20% less than gross monthly wages. Enter your income information in the table below:Table 1: Income Profession: Annual Salary: Gross Monthly Pay (rounded to the cent): Annual salary divided by 12 Show your work! Monthly Net (take-home) Pay (rounded to the cent): Gross monthly pay minus 20% for income taxes, FICA taxes, and health insurance deductions Show your work! STable 2: Mouthy Expenses Budgeted Category Detail: Total Percent of Total Take Category Budgeted Home Pay (Rounded to Amount Nearest Whole Percent) - Show work Housing Rent or mortgage payment = (Need property taxes = Work etc Food Groceries = (Need) going out to eat = small emacke (lattes, vending machine, etc ) = Formula for Work Children) = Insurance Life = (Need) Medical = Doctor Visits for Child(en) = Work Home = Auto = Transportation Car payment = Need) Fuel = Parking = Work: Oil change = But Fare: = Juilities Water = (Need) Electricity = Internet = Work Phone = Personal care Haircut: = (Want) Clothing = Wake up = Work Nail = Diapers / Clothing for Children) = Entertainment Anything fun (leisure activities) = (Want) Netflix = Hulu = Work HBO MIK= Disney Phy = Gym Membership = Subscription Boxes = Vacation = Birthday Holiday gifts = Arecellameous Donations = (Want) Day Care / School Expense: = Pet Expenses = Work: Credit Card Payment = Student Loan Payment = Sawinge Retirement / Savings = (Saving:) Emergency Fund (leftover income) = WorkNote: Total budgeted amount column should add to your entire Monthly Net TakeHome Pay. Remainder of Monthly Net TakeHorne Pay should be calculated into the Emergency Fund category. Here are some realistic estimates for each category to use to compare to your budget percentages: . Housing: ~20% . Food: -10% Insurance, such as life, medical, home, or auto: -10% Transportation or auto services: ~5% . Utilities: ~5% . Personal care: ~15% Entertainment: -10% Misc.: -5% Savings: ~20% c) Create a Monthly Expenses Pie ChartI. Use the information from Table 2: Monthly Expenses to determine the proportion of your net pay currently allotted to needs, wants, and savings. Use Microsoft Excel to create a pie chart to represent the 3 categories. Add a chart title, a legend and include the percentage on each of the three pie slices (data labels). Paste your Microsoft Excel pie chart below. Use the following link to review how to create a pie chart in Excel. Use the below table to create your pie chart in Excel. Creating a pie chart in Excel. Needs (Housing + Food + Insurance + % Transportation + Utilities) Wants (Personal Care + Entertainment % + Miscellaneous) Savingsd) Compare your Monthly Expense Ratios to the 50-30-20 Rule Using the 50-30-20 rule each month, a person spends 50% of their money on needs, 30% on wants, and 20% on savings. Use the following link to assist you with your expense ratio comparison to the 50-30-20 rule: 50-30-20 Rule I. Describe how your pie chart (Part 1 c) compares to the 50-30-20 rule in 2-3 sentences. II. Indicate whether you plan to make any changes in your needs, wants, or savings based on the comparison to 50-30-20 rule. Be specific with your plan!!:1} Calculate your DebttoIncome Ratio Your debt-to-income ratio is all your monthly debt payments {car payments, housing payments, credit card payments, student loan payments, etc. food, utilities, etc. are not considered debut) divided by your gross monthly income. This number allows lenders to measure your ability to manage the monthly payments to repay the money you plan to borrow. Experts recommend your debttoincome ratio should not exceed 43%. Use the following link to assist you with your calculation for the debt-to-Income Ratio. Debttolncome Ratio I. Use the information 'om Table 2: Monthly Expenses (Part 1) to determine your Debt-to-Income Ratio. Show the complete breakdown of your work. II. Describe how your debttoincome ratio compares to the recommended ratio in 2-3 sentences. Is this good or bad? Depending on which, do you need to do anything to change your debt-to-income ratio? If so, how? b) Calculate your Life Insurance Policy Life insurance is used to replace income when you die. A younger person with dependents likely needs more life insurance than an older person with few to zero dependents. Experts recommend, on average, your life insurance should be 10 TIMES your gross annual income. For more information about life insurance and how much your could be worth, use the following link to assist you: 10X Your Annual Salary - Life Insurance RatioUH I. Use the information from Table 1: Income from Part 1 and the suggested average of 10 times your gross annual income to calculate your recommended life insurance policy. Show the complete breakdown of work. II. 1iJilliat are dependents? 1Why would someone who is younger with dependents need more life insurance than someone who is older with few or no dependents? Explain your answer in 34 sentences. c) Calculate your Retirement Savings Saving for retirement is something everyone should consider as soon as they can start saving. The "All About the Benjamin's Report" should be evidence that the earlier you can start saving, the more you should be able to save. I. Based on your current Savings from Table 2, calculate your retirement savings by the time you are 65. Calculate your retirement savings by the time you are 70. Show the complete breakdown of work. II. Based on your previous answer, discuss whether or not you believe you are saving enough each month to have enough money saved by age 65 to retire. What about age 70? If not, what specific actions can you take now to ensure you are saving enough for retirement? Write your answer in 3-4 sentences.d) Calculate your Emergency Fund Do you currently have an emergency fund? Financial experts recommend having at least 6 months of expenses saved up for emergencies. I. Calculate 6 TIMES your monthly expenses. Show the complete breakdown of work.\f9 II. Determine how long will it take you to save 6 months of expenses based on your monthly savings from Table 2: Monthly Expenses (in Part 1). Show the complete breakdown of your work. Round your answer to the nearest month.Mortgage, Monthly Payments, and Analysis When you apply for a mortgage, the lender will assess your ability to pay back the loan. The lender will look for collateral (assets), which could cover the loan in case of default. As a future homeowner, you also want to make sure you can save for the future. There will be documents you need to submit to the mortgage company for approval. a) Determine Documents for Mortgage Pre-Approval In 2-3 sentences, describe the documents you will need to submit to the mortgage company for a mortgage approval.b) Research Houses of Interest Use Zillow.com or Realtor.com to research 5 houses currently for sale that you would be interested in buying. Be sure to look in the city and state you are interested in and fill out the table below. Address, City, State List Price Number of Number of Square Bedrooms Bathrooms Footagec) Calculate Monthly Payment Calculate the monthly payment for each house based on a 30-year loan with a 5% interest rate and a down payment of $5.000. Use the following website to help you calculate the monthly payments. https://www.calculatorsoup.com/calculators/financial/loan- calculator.php House Address Monthly Paymenta) Calculate Housing Ratio Financial experts recommend your monthly housing costs should not exceed 20% of your take-home (net) pay. I. Calculate the housing ratio for each house. Show the complete breakdown of your work. House Address Housing Ratio (Show all work)a) Calculate Housing Ratio Financial experts recommend your monthly housing costs should not exceed 20% of your take-home (net) pay. I. Calculate the housing ratio for each house. Show the complete breakdown of your work. House Address Housing Ratio (Show all work)II. In 12 sentences: determine which houses are within your budget {remember= the housing ratio should be 2D% or lower to be considered within budget). e) Calculate Total Amount Paid and Interest Choose one house that is within your budget that you would like to purchase. I. Calculate the total amount paid over the 313 years. Show the complete breakdown ofyour work. II. Calculate the total amount of interest paid. Show the complete breakdown of your work. 1) Calculate Closing Costs Before taking ownership ofyour new house, you will need to pa").r closing costs. Closing cost fees will be approxinlately 5% of the list price of the house you are purchasing. Calculate the closing costs for the house you chose in part (e). Show the complete breakdown of your work. g) Financial Analysis Determine if you think you are ready to apply for a mortgage today, within 2 years, or more than 5 years in the future. Explain your answer in 3 - 4 sentences.W2P: Portfolio Project - Part 1 - Budget Basics - Click here to submit Deadline Due by the end of Week 2 at 11:59 pm, ET. Directions You will complete a portion of your Portfolio Project. For detailed directions, please refer to the Portfolio Project Directions and Rubric document available in the Course Assessments button. You will also need the following template document to complete your project. Each part will be added to this document so ensure you save it in a place you know where it is

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!