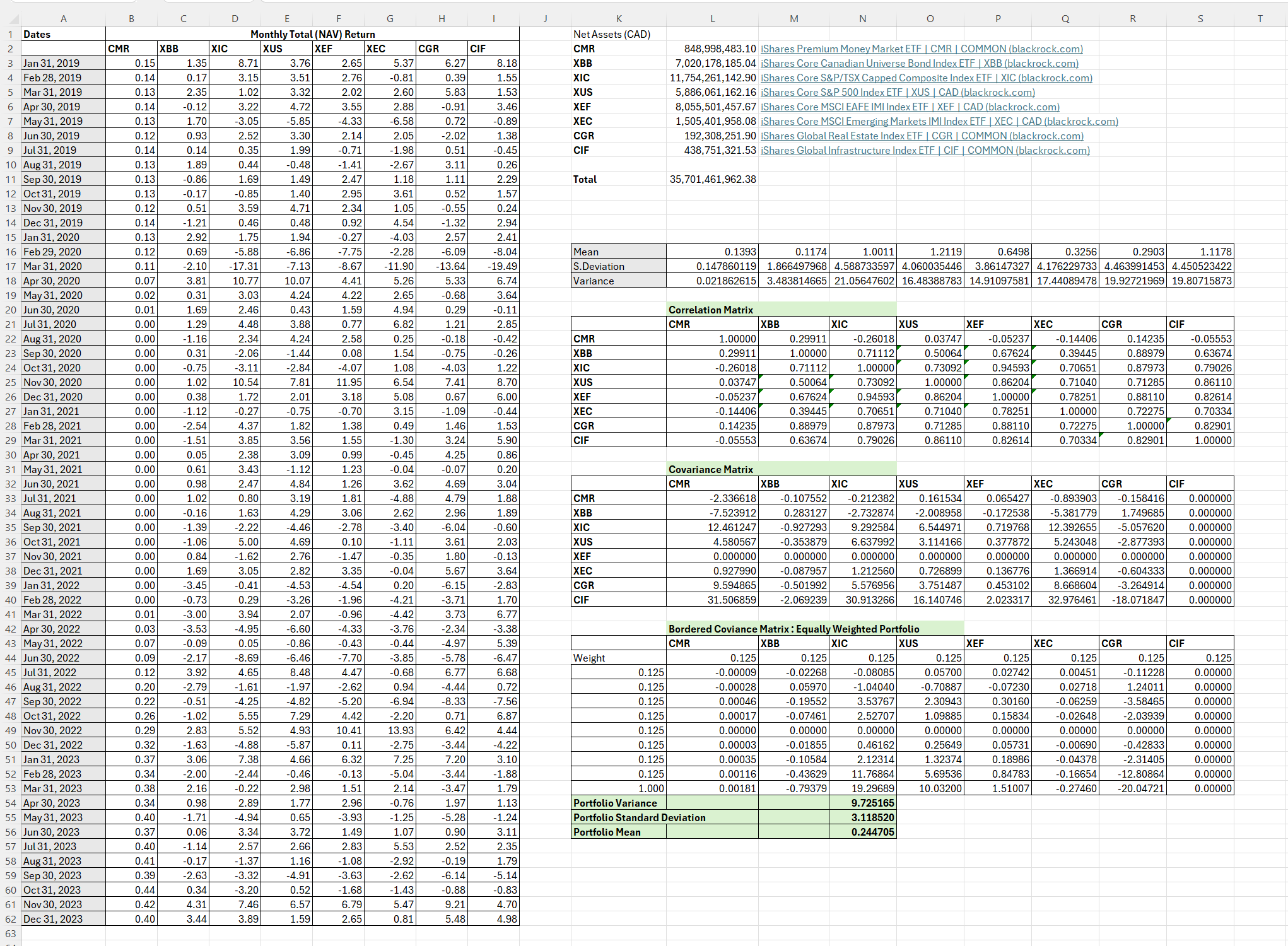

Question: I ' m really stuck on this assignment, and need help with the next steps. I calculated some of the matrix, but I don't know

Im really stuck on this assignment, and need help with the next steps. I calculated some of the matrix, but I don't know how to find the weightings of each asset, and I need help graphing the efficiency frontier. Please help! Here are the requirements:

You need to make an asset allocation recommendation based on the following asset classes and their respective benchmarks. To do this, you need to calculate the efficient frontier, determine the minimum variance and optimal risk portfolio for each of the following scenarios:

Scenario Short selling is permitted

aThe efficient frontier graph

bThe return, risk and composition of the minimum variance portfolio

cThe return, risk and composition of the optimal risky portfolio

Scenario Short selling is Not permitted

aThe efficient frontier graph

b The return, risk and composition of the minimum variance portfolio

cThe return, risk and composition of the optimal risky portfolio

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock