Question: I need calculation step by step. Thank you! Consider an investor with mean-variance preferences given by E [R_P] - 1/4 sigma^2 _P The investor faces

I need calculation step by step. Thank you!

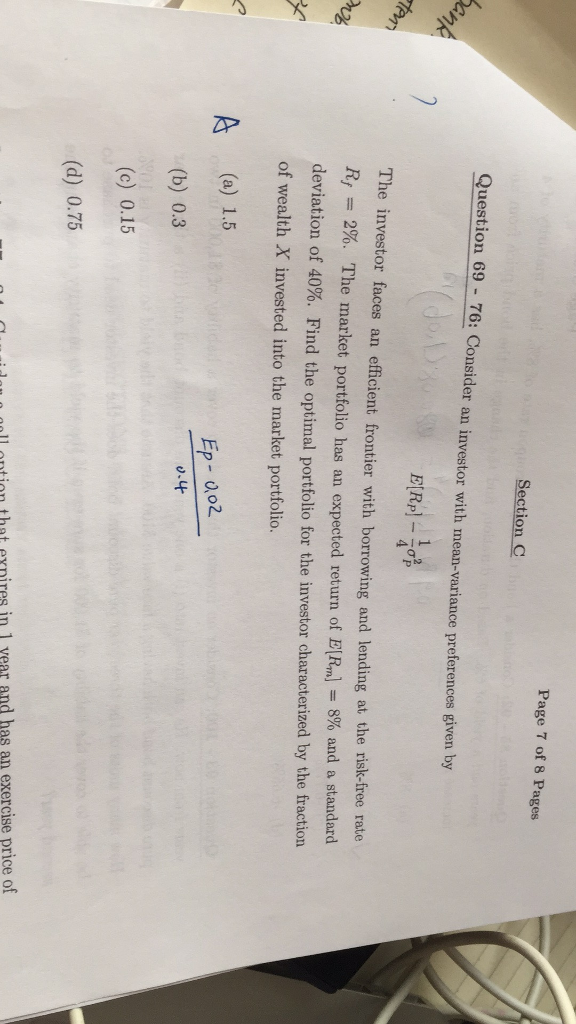

Consider an investor with mean-variance preferences given by E [R_P] - 1/4 sigma^2 _P The investor faces an efficient frontier with borrowing and lending at the risk-free rate R_f = 2%. The market portfolio has an expected return of E[R_m] = 8% and a standard deviation of 40%. Find the optimal portfolio for the investor characterized by the fraction of wealth X invested into the market portfolio. 1.5 0.3 0.15 0.75

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock