Question: i need excel solution Intro You found the expected returns and variance-covariance matrix of returns for 3 stocks: Amazon Walmart Exxon Er) 36.996 16.896 4.5%

i need excel solution

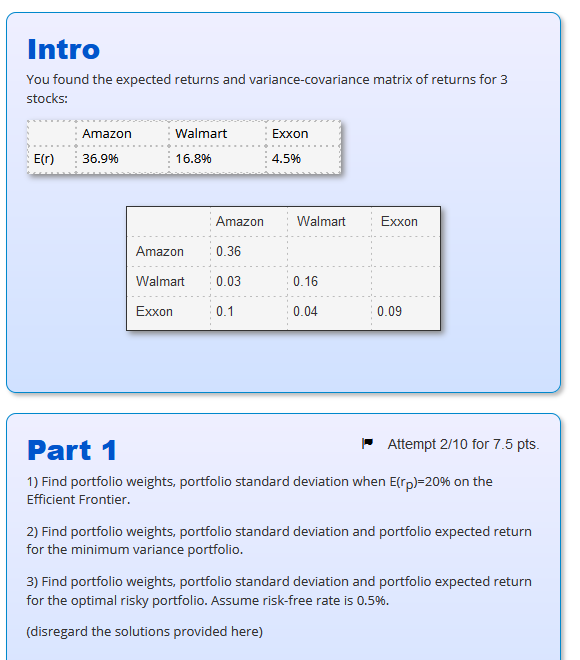

Intro You found the expected returns and variance-covariance matrix of returns for 3 stocks: Amazon Walmart Exxon Er) 36.996 16.896 4.5% Amazon Walmart Exxon Amazon 0.36 Walmart 0.03 0.16 Exxon 0.1 0.04 0.09 Part 1 Attempt 2/10 for 7.5 pts. 1) Find portfolio weights, portfolio standard deviation when E(rp)=20% on the Efficient Frontier 2) Find portfolio weights, portfolio standard deviation and portfolio expected return for the minimum variance portfolio. 3) Find portfolio weights, portfolio standard deviation and portfolio expected return for the optimal risky portfolio. Assume risk-free rate is 0.5%. (disregard the solutions provided here) Intro You found the expected returns and variance-covariance matrix of returns for 3 stocks: Amazon Walmart Exxon Er) 36.996 16.896 4.5% Amazon Walmart Exxon Amazon 0.36 Walmart 0.03 0.16 Exxon 0.1 0.04 0.09 Part 1 Attempt 2/10 for 7.5 pts. 1) Find portfolio weights, portfolio standard deviation when E(rp)=20% on the Efficient Frontier 2) Find portfolio weights, portfolio standard deviation and portfolio expected return for the minimum variance portfolio. 3) Find portfolio weights, portfolio standard deviation and portfolio expected return for the optimal risky portfolio. Assume risk-free rate is 0.5%. (disregard the solutions provided here)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts