Question: I need help calculating the blanks for this problem Merge & Center $ %% 80 Conditional Format Cell Formatting as Table Styles B D E

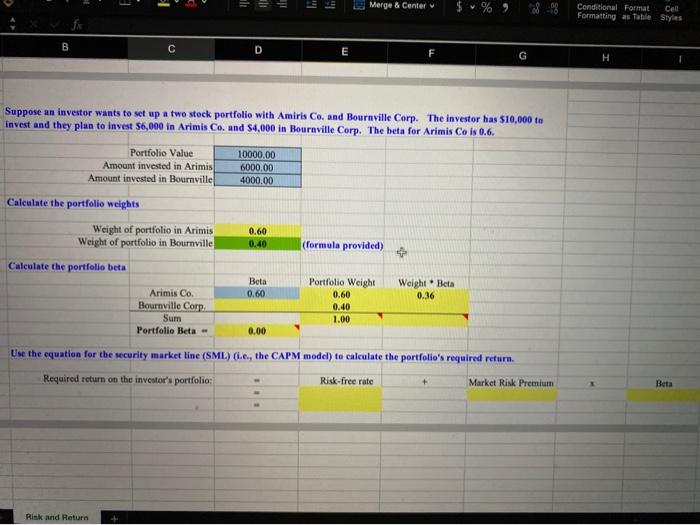

Merge & Center $ %% 80 Conditional Format Cell Formatting as Table Styles B D E H Suppose an investor wants to set up a two stock portfolio with Amiris Co, and Bournville Corp. The investor has $10,000 to invest and they plan to invest $6,000 in Arimis Co. and $4,000 in Bournville Corp. The beta for Arimis Co is 0.6. Portfolio Value Amount invested in Arimis Amount invested in Bournville 10000.00 6000.00 4000.00 Calculate the portfolio weights Weight of portfolio in Arimis Weight of portfolio in Bournville 0.6 0.40 (formula provided) Calculate the portfolio beta Beta 0.60 Portfolio Weight 0.60 0.40 1.00 Weight Beta 0.36 Arimis Co. Bournville Corp Sum Portfolio Beta - 0.00 Use the equation for the security market line (SML.) (.e., the CAPM model) to calculate the portfolio's required return Required return on the investor's portfolio: Risk free rate Market Risk Premium Beta Risk and Return Merge & Center $ %% 80 Conditional Format Cell Formatting as Table Styles B D E H Suppose an investor wants to set up a two stock portfolio with Amiris Co, and Bournville Corp. The investor has $10,000 to invest and they plan to invest $6,000 in Arimis Co. and $4,000 in Bournville Corp. The beta for Arimis Co is 0.6. Portfolio Value Amount invested in Arimis Amount invested in Bournville 10000.00 6000.00 4000.00 Calculate the portfolio weights Weight of portfolio in Arimis Weight of portfolio in Bournville 0.6 0.40 (formula provided) Calculate the portfolio beta Beta 0.60 Portfolio Weight 0.60 0.40 1.00 Weight Beta 0.36 Arimis Co. Bournville Corp Sum Portfolio Beta - 0.00 Use the equation for the security market line (SML.) (.e., the CAPM model) to calculate the portfolio's required return Required return on the investor's portfolio: Risk free rate Market Risk Premium Beta Risk and Return

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts