Question: I need help here. Suppose that the current time corresponds to / =5 and that the force of interest has been a constant 4% pa

I need help here.

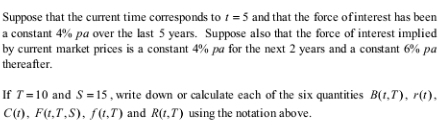

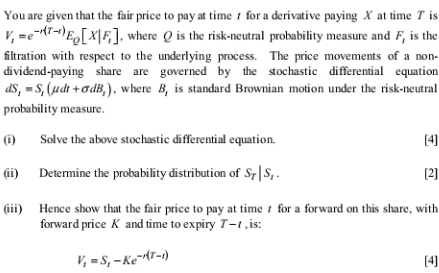

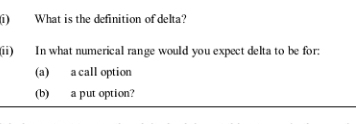

Suppose that the current time corresponds to / =5 and that the force of interest has been a constant 4% pa over the last 5 years. Suppose also that the force of interest implied by current market prices is a constant 4% pa for the next 2 years and a constant 6% pa thereafter. If 7 =10 and $ = 15, write down or calculate each of the six quantities B(r,D). r() C(n), F(,T.S). f(1.") and R(r, T) using the notation above.You are given that the fair price to pay at time / for a derivative paying X" at time T is V. =e-MY-DE XF, . where O is the risk-neutral probability measure and F, is the filtration with respect to the underlying process. The price movements of a non- dividend-paying share are governed by the stochastic differential equation dS, - S, (udi + GdB, ), where B, is standard Brownian motion under the risk-neutral probability measure. Solve the above stochastic differential equation. [4] Determine the probability distribution of Sy | S, - [2] Hence show that the fair price to pay at time r for a forward on this share, with forward price K and time to expiry 7-1 , is: V, -S, -Ke (T-1) [4]What is the definition of delta? In what numerical range would you expect delta to be for: (a) a call option (b) a put option

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts