Question: I need help in this question, Please follow all the question and do not do it wrong. Please do it correctly and 100% BACKGROUND INFORMATION

I need help in this question, Please follow all the question and do not do it wrong. Please do it correctly and 100%

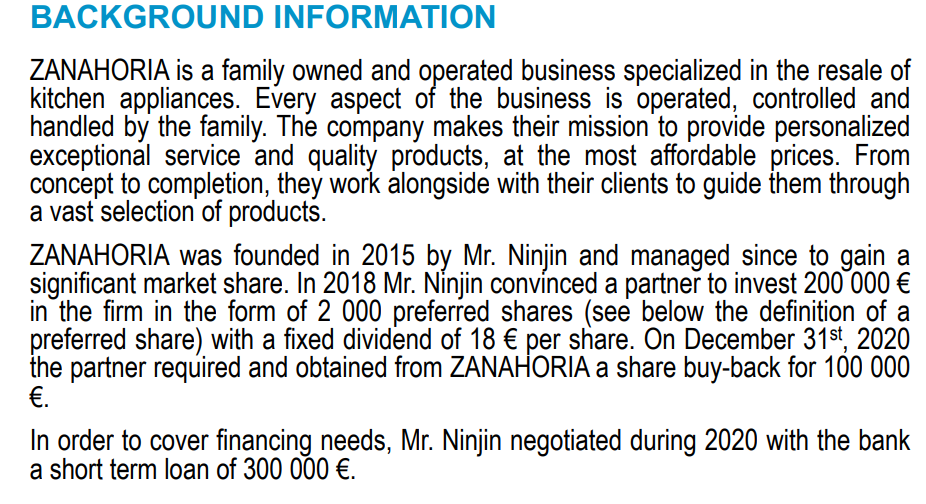

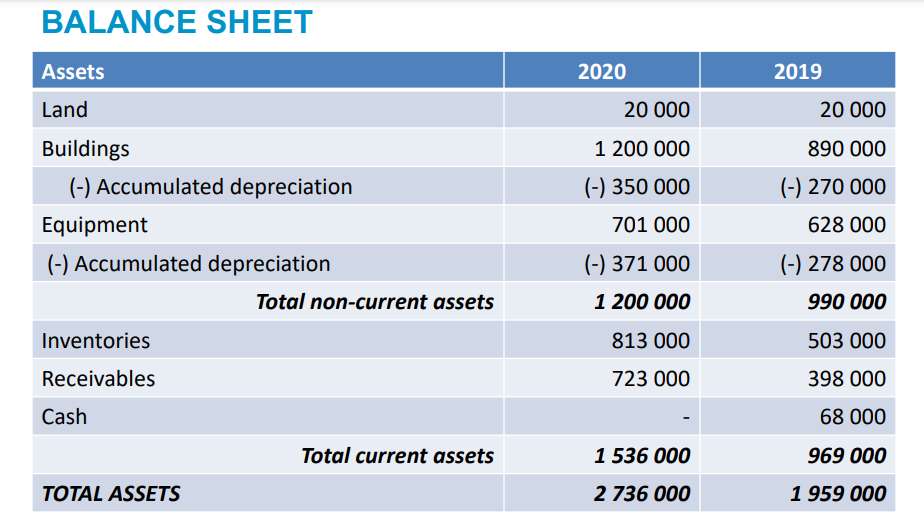

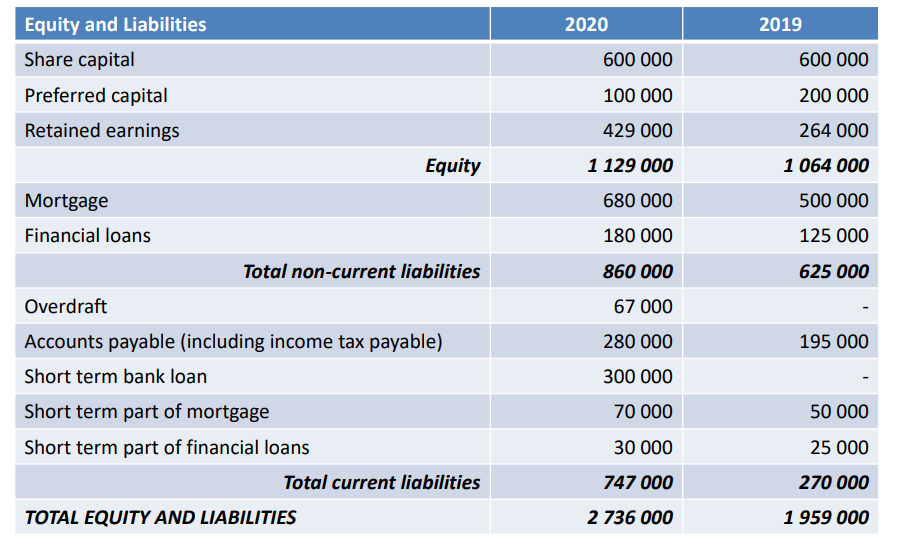

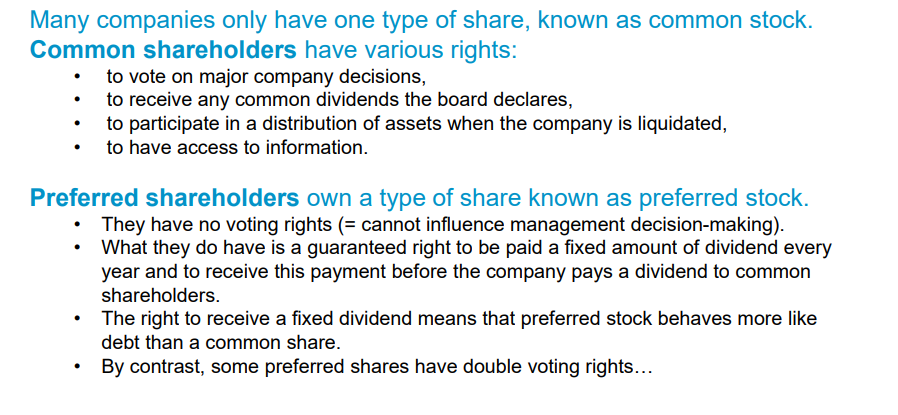

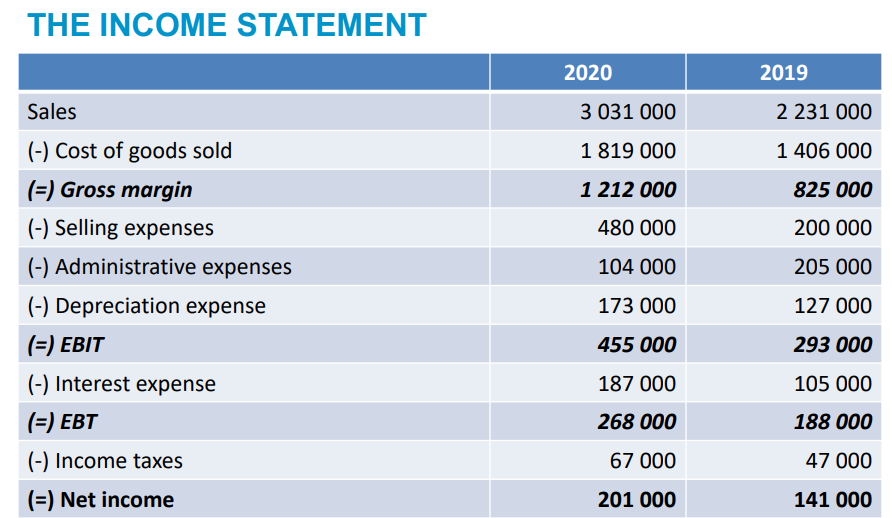

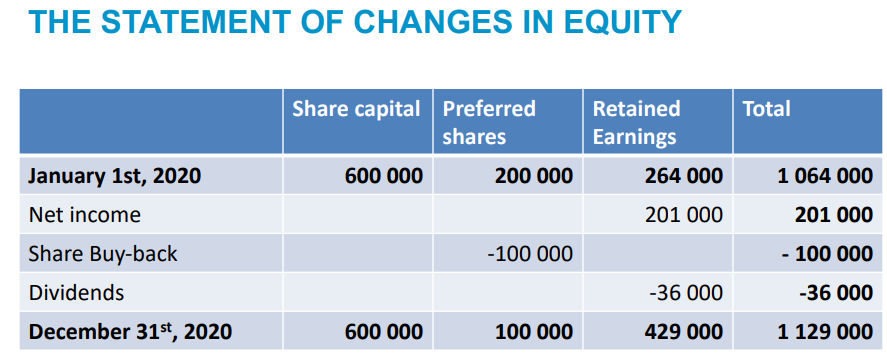

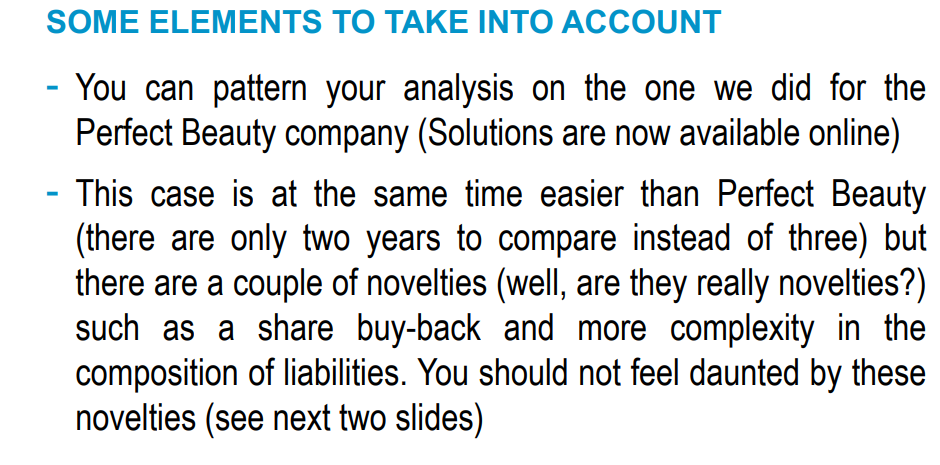

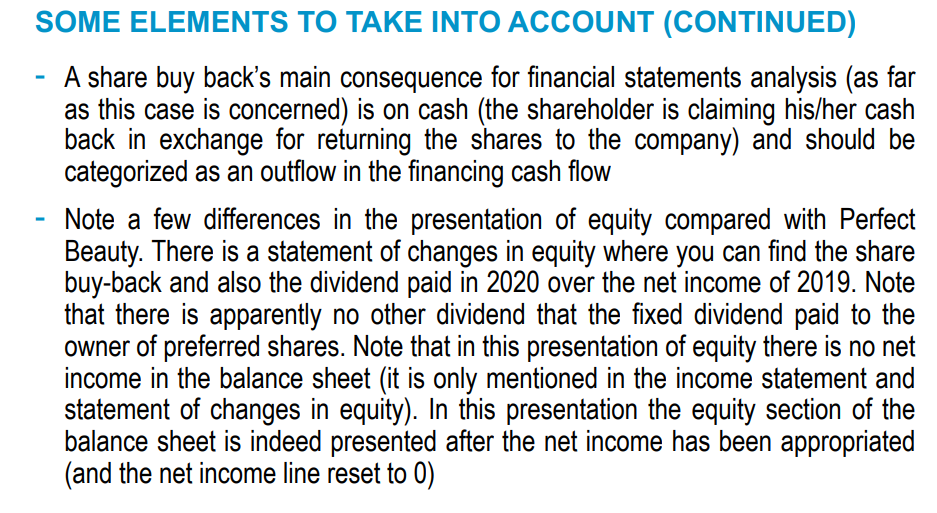

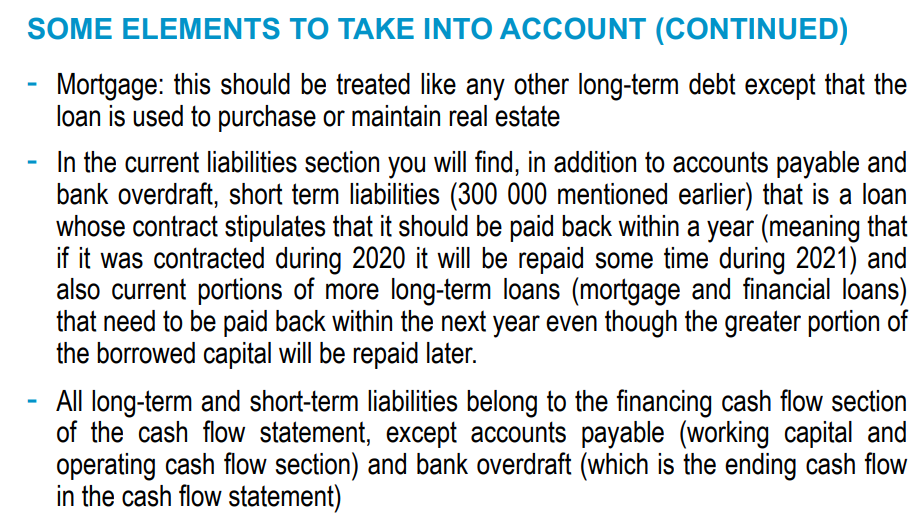

BACKGROUND INFORMATION ZANAHORIA is a family owned and operated business specialized in the resale of kitchen appliances. Every aspect of the business is operated, controlled and handled by the family. The company makes their mission to provide personalized exceptional service and quality products, at the most affordable prices. From concept to completion, they work alongside with their clients to guide them through a vast selection of products. ZANAHORIA was founded in 2015 by Mr. Ninjin and managed since to gain a significant market share. In 2018 Mr. Nnjin convinced a partner to invest 200 000 in the firm in the form of 2 000 preferred shares (see below the definition of a preferred share) with a fixed dividend of 18 per share. On December 31st , 2020 the partner required and obtained from ZANAHORIA a share buy-back for 100 000 . In order to cover financing needs, Mr. Ninjin negotiated during 2020 with the bank a short term loan of 300 000 . BALANCE SHEET Assets 2020 2019 Land 20 000 20 000 1 200 000 890 000 (-) 350 000 Buildings (-) Accumulated depreciation Equipment (-) Accumulated depreciation Total non-current assets (-) 270 000 628 000 701 000 (-) 371 000 (-) 278 000 1 200 000 990 000 Inventories 813 000 503 000 Receivables 723 000 398 000 Cash 68 000 Total current assets 1 536 000 969 000 TOTAL ASSETS 2 736 000 1 959 000 2019 2020 600 000 100 000 600 000 200 000 264 000 429 000 1 129 000 1 064 000 500 000 680 000 180 000 125 000 Equity and Liabilities Share capital Preferred capital Retained earnings Equity Mortgage Financial loans Total non-current liabilities Overdraft Accounts payable (including income tax payable) Short term bank loan Short term part of mortgage Short term part of financial loans Total current liabilities 625 000 860 000 67 000 280 000 195 000 300 000 70 000 50 000 30 000 25 000 747 000 270 000 TOTAL EQUITY AND LIABILITIES 2 736 000 1 959 000 Many companies only have one type of share, known as common stock. Common shareholders have various rights: to vote on major company decisions, to receive any common dividends the board declares, to participate in a distribution of assets when the company is liquidated, to have access to information. Preferred shareholders own a type of share known as preferred stock. They have no voting rights (= cannot influence management decision-making). What they do have is a guaranteed right to be paid a fixed amount of dividend every year and to receive this payment before the company pays a dividend to common shareholders. The right to receive a fixed dividend means that preferred stock behaves more like debt than a common share. By contrast, some preferred shares have double voting rights... . THE INCOME STATEMENT 2020 2019 Sales 3 031 000 2 231 000 1 819 000 1 406 000 1 212 000 825 000 480 000 200 000 104 000 205 000 127 000 (-) Cost of goods sold (=) Gross margin (-) Selling expenses (-) Administrative expenses (-) Depreciation expense =) EBIT (-) Interest expense (=) EBT (-) Income taxes (=) Net income 173 000 455 000 293 000 187 000 105 000 268 000 188 000 67 000 47 000 201 000 141 000 THE STATEMENT OF CHANGES IN EQUITY Total Share capital Preferred shares Retained Earnings January 1st, 2020 600 000 200 000 264 000 1 064 000 Net income 201 000 201 000 Share Buy-back -100 000 - 100 000 Dividends -36 000 -36 000 December 31st, 2020 600 000 100 000 429 000 1 129 000 REQUIRED Mr. Ninjin is very surprised by the situation of his company. He thought everything was on track as sales and profit had steadily progressed these past years. He had bought new storage space and had also invested in new equipment to optimize administrative tasks, something which had resulted in administrative expenses decreasing very substantially. What could have gone wrong and resulted in the company being out of cash at the end of 2020? Your task is to help Mr Ninjin make sense of the situation and suggest some solutions to improve the cash balance of the company. To this end you will carry out: REQUIRED - An analysis of cash-flows for the year 2020. To this end you will prepare the appropriate cash-flow statement with the help of the information provided in the income statements, balance sheets for the years 2019 and 2020 and of the additional information provided in the next slides You will also conduct an analysis based on appropriate ratios. You can either use the ratios that we successively saw in our classes (starting with the analysis of the income statement) or decompose the profitability of the company (measured by its return on equity) and present ratios as constituting a pyramid (I know we have not covered in detail this approach but you can also use the solutions to the Perfect Beauty case). With your analysis you will try and answer the following questions: is the company well managed from the point of view of its operations? From the point of view of its investment policy? Financial policy? Dividend policy? SOME ELEMENTS TO TAKE INTO ACCOUNT - You can pattern your analysis on the one we did for the Perfect Beauty company (Solutions are now available online) This case is at the same time easier than Perfect Beauty (there are only two years to compare instead of three) but there are a couple of novelties (well, are they really novelties?) such as a share buy-back and more complexity in the composition of liabilities. You should not feel daunted by these novelties (see next two slides) SOME ELEMENTS TO TAKE INTO ACCOUNT (CONTINUED) A share buy back's main consequence for financial statements analysis (as far as this case is concerned) is on cash (the shareholder is claiming his/her cash back in exchange for returning the shares to the company) and should be categorized as an outflow in the financing cash flow Note a few differences in the presentation of equity compared with Perfect Beauty. There is a statement of changes in equity where you can find the share buy-back and also the dividend paid in 2020 over the net income of 2019. Note that there is apparently no other dividend that the fixed dividend paid to the owner of preferred shares. Note that in this presentation of equity there is no net income in the balance sheet (it is only mentioned in the income statement and statement of changes in equity). In this presentation the equity section of the balance sheet is indeed presented after the net income has been appropriated (and the net income line reset to 0) SOME ELEMENTS TO TAKE INTO ACCOUNT (CONTINUED) Mortgage: this should be treated like any other long-term debt except that the loan is used to purchase or maintain real estate In the current liabilities section you will find, in addition to accounts payable and bank overdraft, short term liabilities (300 000 mentioned earlier) that is a loan whose contract stipulates that it should be paid back within a year (meaning that if it was contracted during 2020 it will be repaid some time during 2021) and also current portions of more long-term loans (mortgage and financial loans) that need to be paid back within the next year even though the greater portion of the borrowed capital will be repaid later. All long-term and short-term liabilities belong to the financing cash flow section of the cash flow statement, except accounts payable (working capital and operating cash flow section) and bank overdraft (which is the ending cash flow in the cash flow statement) BACKGROUND INFORMATION ZANAHORIA is a family owned and operated business specialized in the resale of kitchen appliances. Every aspect of the business is operated, controlled and handled by the family. The company makes their mission to provide personalized exceptional service and quality products, at the most affordable prices. From concept to completion, they work alongside with their clients to guide them through a vast selection of products. ZANAHORIA was founded in 2015 by Mr. Ninjin and managed since to gain a significant market share. In 2018 Mr. Nnjin convinced a partner to invest 200 000 in the firm in the form of 2 000 preferred shares (see below the definition of a preferred share) with a fixed dividend of 18 per share. On December 31st , 2020 the partner required and obtained from ZANAHORIA a share buy-back for 100 000 . In order to cover financing needs, Mr. Ninjin negotiated during 2020 with the bank a short term loan of 300 000 . BALANCE SHEET Assets 2020 2019 Land 20 000 20 000 1 200 000 890 000 (-) 350 000 Buildings (-) Accumulated depreciation Equipment (-) Accumulated depreciation Total non-current assets (-) 270 000 628 000 701 000 (-) 371 000 (-) 278 000 1 200 000 990 000 Inventories 813 000 503 000 Receivables 723 000 398 000 Cash 68 000 Total current assets 1 536 000 969 000 TOTAL ASSETS 2 736 000 1 959 000 2019 2020 600 000 100 000 600 000 200 000 264 000 429 000 1 129 000 1 064 000 500 000 680 000 180 000 125 000 Equity and Liabilities Share capital Preferred capital Retained earnings Equity Mortgage Financial loans Total non-current liabilities Overdraft Accounts payable (including income tax payable) Short term bank loan Short term part of mortgage Short term part of financial loans Total current liabilities 625 000 860 000 67 000 280 000 195 000 300 000 70 000 50 000 30 000 25 000 747 000 270 000 TOTAL EQUITY AND LIABILITIES 2 736 000 1 959 000 Many companies only have one type of share, known as common stock. Common shareholders have various rights: to vote on major company decisions, to receive any common dividends the board declares, to participate in a distribution of assets when the company is liquidated, to have access to information. Preferred shareholders own a type of share known as preferred stock. They have no voting rights (= cannot influence management decision-making). What they do have is a guaranteed right to be paid a fixed amount of dividend every year and to receive this payment before the company pays a dividend to common shareholders. The right to receive a fixed dividend means that preferred stock behaves more like debt than a common share. By contrast, some preferred shares have double voting rights... . THE INCOME STATEMENT 2020 2019 Sales 3 031 000 2 231 000 1 819 000 1 406 000 1 212 000 825 000 480 000 200 000 104 000 205 000 127 000 (-) Cost of goods sold (=) Gross margin (-) Selling expenses (-) Administrative expenses (-) Depreciation expense =) EBIT (-) Interest expense (=) EBT (-) Income taxes (=) Net income 173 000 455 000 293 000 187 000 105 000 268 000 188 000 67 000 47 000 201 000 141 000 THE STATEMENT OF CHANGES IN EQUITY Total Share capital Preferred shares Retained Earnings January 1st, 2020 600 000 200 000 264 000 1 064 000 Net income 201 000 201 000 Share Buy-back -100 000 - 100 000 Dividends -36 000 -36 000 December 31st, 2020 600 000 100 000 429 000 1 129 000 REQUIRED Mr. Ninjin is very surprised by the situation of his company. He thought everything was on track as sales and profit had steadily progressed these past years. He had bought new storage space and had also invested in new equipment to optimize administrative tasks, something which had resulted in administrative expenses decreasing very substantially. What could have gone wrong and resulted in the company being out of cash at the end of 2020? Your task is to help Mr Ninjin make sense of the situation and suggest some solutions to improve the cash balance of the company. To this end you will carry out: REQUIRED - An analysis of cash-flows for the year 2020. To this end you will prepare the appropriate cash-flow statement with the help of the information provided in the income statements, balance sheets for the years 2019 and 2020 and of the additional information provided in the next slides You will also conduct an analysis based on appropriate ratios. You can either use the ratios that we successively saw in our classes (starting with the analysis of the income statement) or decompose the profitability of the company (measured by its return on equity) and present ratios as constituting a pyramid (I know we have not covered in detail this approach but you can also use the solutions to the Perfect Beauty case). With your analysis you will try and answer the following questions: is the company well managed from the point of view of its operations? From the point of view of its investment policy? Financial policy? Dividend policy? SOME ELEMENTS TO TAKE INTO ACCOUNT - You can pattern your analysis on the one we did for the Perfect Beauty company (Solutions are now available online) This case is at the same time easier than Perfect Beauty (there are only two years to compare instead of three) but there are a couple of novelties (well, are they really novelties?) such as a share buy-back and more complexity in the composition of liabilities. You should not feel daunted by these novelties (see next two slides) SOME ELEMENTS TO TAKE INTO ACCOUNT (CONTINUED) A share buy back's main consequence for financial statements analysis (as far as this case is concerned) is on cash (the shareholder is claiming his/her cash back in exchange for returning the shares to the company) and should be categorized as an outflow in the financing cash flow Note a few differences in the presentation of equity compared with Perfect Beauty. There is a statement of changes in equity where you can find the share buy-back and also the dividend paid in 2020 over the net income of 2019. Note that there is apparently no other dividend that the fixed dividend paid to the owner of preferred shares. Note that in this presentation of equity there is no net income in the balance sheet (it is only mentioned in the income statement and statement of changes in equity). In this presentation the equity section of the balance sheet is indeed presented after the net income has been appropriated (and the net income line reset to 0) SOME ELEMENTS TO TAKE INTO ACCOUNT (CONTINUED) Mortgage: this should be treated like any other long-term debt except that the loan is used to purchase or maintain real estate In the current liabilities section you will find, in addition to accounts payable and bank overdraft, short term liabilities (300 000 mentioned earlier) that is a loan whose contract stipulates that it should be paid back within a year (meaning that if it was contracted during 2020 it will be repaid some time during 2021) and also current portions of more long-term loans (mortgage and financial loans) that need to be paid back within the next year even though the greater portion of the borrowed capital will be repaid later. All long-term and short-term liabilities belong to the financing cash flow section of the cash flow statement, except accounts payable (working capital and operating cash flow section) and bank overdraft (which is the ending cash flow in the cash flow statement)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts