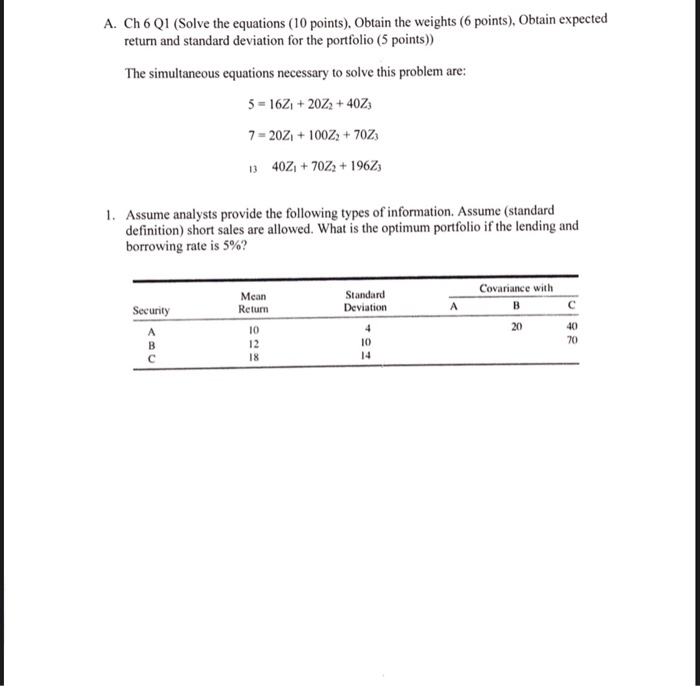

Question: I need help solving without the use of Microsoft Excel. I was also given the Z values: Z1: 0.292831 Z2: 0.009118 Z3: 0.003309 A. Ch

I need help solving without the use of Microsoft Excel.

I was also given the Z values:

Z1: 0.292831

Z2: 0.009118

Z3: 0.003309

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock