Question: I need help to solve the following question from the course Mathematical Finance. The related theory is the Fundamental Theory of Asset Pricing. Consider the

I need help to solve the following question from the course Mathematical Finance. The related theory is the Fundamental Theory of Asset Pricing.

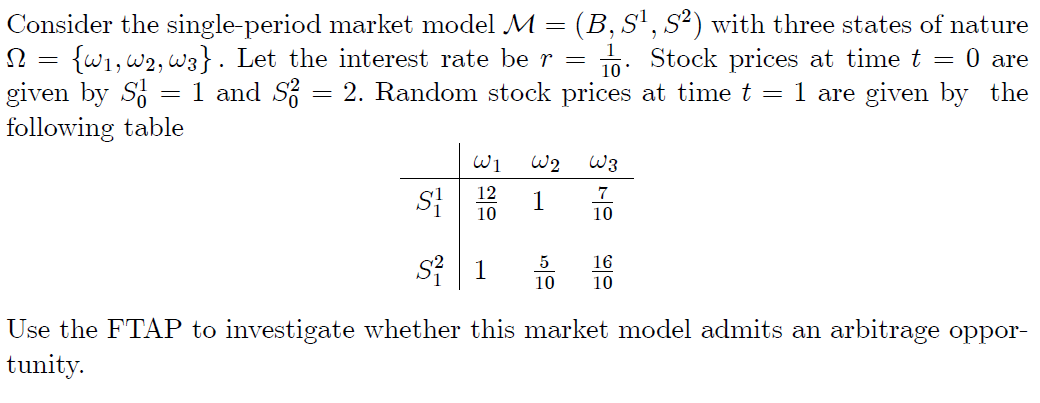

Consider the singleperiod market model M = (B, 81, 5'2) with three states of nature (2 : {M1,w2,w3}. Let the interest rate be S" : 110. Stock prices at time If : 0 are given by 5'6 : 1 and 33 : 2. Random stock prices at time t : 1 are given by the following table 001 M2 M3 1 1_2 1 81 10 1 10 2 5 16 Use the FTAP to investigate whether this market model admits an arbitrage oppor tunity

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock