Question: I need help with these two questions, please You see the current 3-month T-bill quoted on a discount basis at 1.9325-1.9250. The T-bill has a

I need help with these two questions, please

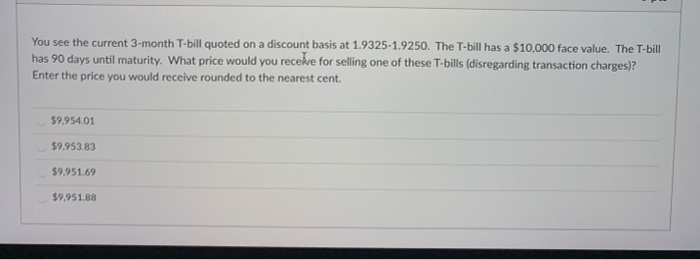

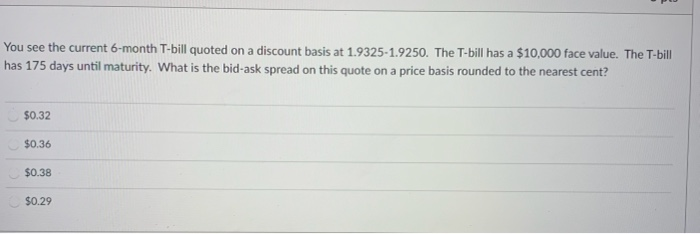

You see the current 3-month T-bill quoted on a discount basis at 1.9325-1.9250. The T-bill has a $10,000 face value. The T-bill has 90 days until maturity. What price would you receive for selling one of these T-bills (disregarding transaction charges)? Enter the price you would receive rounded to the nearest cent. $9.954.01 $9.953.83 $9.951.69 $9.951.88 You see the current 6-month T-bill quoted on a discount basis at 1.9325-1.9250. The T-bill has a $10,000 face value. The T-bill has 175 days until maturity. What is the bid-ask spread on this quote on a price basis rounded to the nearest cent? $0.32 $0.36 $0.38 $0.29

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock