Question: I need some help solving these questions, can you provide the formulas and detailed step by step solutions? Midterm Exam Version A FIN'QTQT: Options Markets.

I need some help solving these questions, can you provide the formulas and detailed step by step solutions?

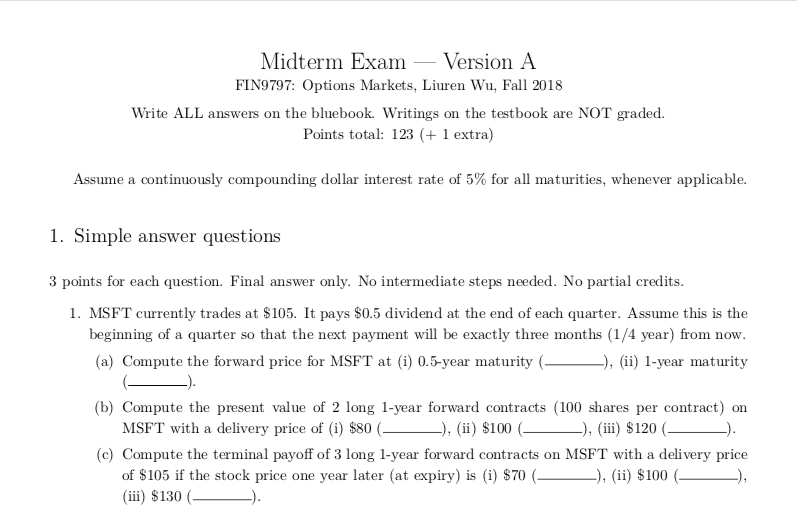

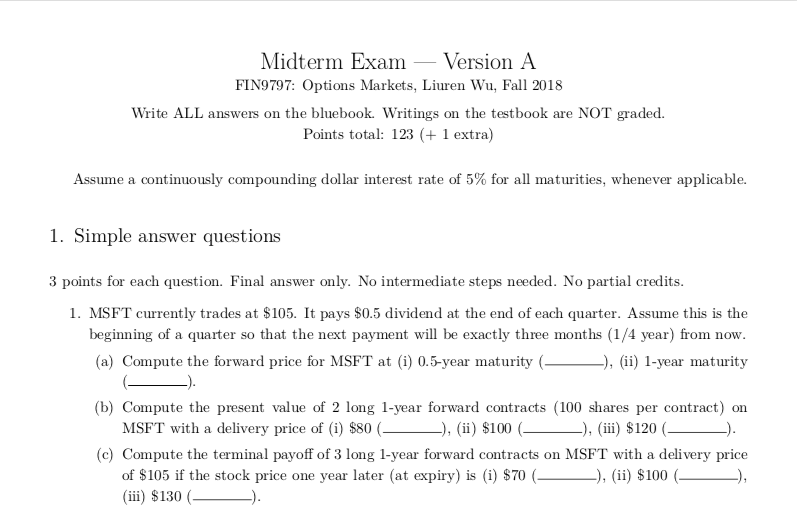

Midterm Exam Version A FIN'QTQT: Options Markets. Liuren Wu. Fall 2013 "Hte ALL answers on the hluehook. Writings on the testhook are NOT graded. Points total: 123 (+ 1 extra} Assume a continuously compounding dollar interest rate of 5% for all maturities1 whenever applicable. 1. Simple answer questions 3 points for each question. Final answer only. No intermediate steps needed. No partial credits. 1. MSF T currently trades at $105. It pays $0.5 dividend at the end of each quarter. Assume this is the beginning of a quarter so that the next payment will be exactly three months (1ft! year} -om now. {a} Compute the forward price for MSFT at (i) 0. 5year maturity (JI. (ii) 1-year maturity (l- {h} Compute the present value of 2 long 1year forward contracts {100 shares per contract} on MSFT with a delivery price of {i} $30 {JI. {ii} $100 {JI. {iii} $120 {}_ {c} Compute the terminal payoff of 3 long 1-year forward contracts on MSFT' with a delivery price of $105 if the stock price one year later (at expiry]I is (i) $10 (JI. (ii) $100 (}. {iii} $130 {_}

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts