Question: I need the answer as soon as possible 9154 0.51. Consider the following data for the companies P and S: Company Beta Standard deviation Covariance

I need the answer as soon as possible

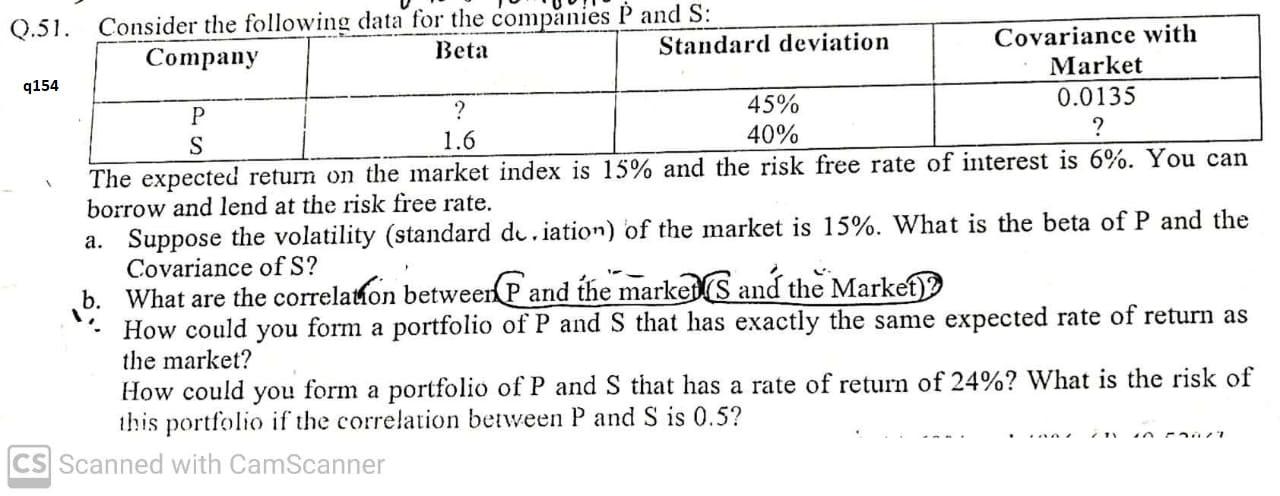

9154 0.51. Consider the following data for the companies P and S: Company Beta Standard deviation Covariance with Market ? 45% 0.0135 S 1.6 40% ? The expected return on the market index is 15% and the risk free rate of interest is 6%. You can borrow and lend at the risk free rate. a. Suppose the volatility (standard du.iation) of the market is 15%. What is the beta of P and the Covariance of S? b. What are the correlation between P and the market and the Market)? How could you form a portfolio of P and S that has exactly the same expected rate of return as the market? How could you form a portfolio of P and S that has a rate of return of 24%? What is the risk of this portfolio if the correlation between P and S is 0.5? CS Scanned with CamScanner

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts