Question: I need to process to solve those problem. Answer is 1. D, 2.C, 3.B, 4.A, 5.D, 6.A, 7.A, 8.B, 9.C, 10.A, 11.B, 12.C, 13.B, 14.A,

I need to process to solve those problem.

Answer is

1. D, 2.C, 3.B, 4.A, 5.D, 6.A, 7.A, 8.B, 9.C, 10.A,

11.B, 12.C, 13.B, 14.A, 15.C, 16.C, 17.D, 18.A, 19.C, 20.A,

21.D, 22.A, 23.A, 24.B, 25.A, 26.A, 27.C, 28.B, 29.C, 30.C

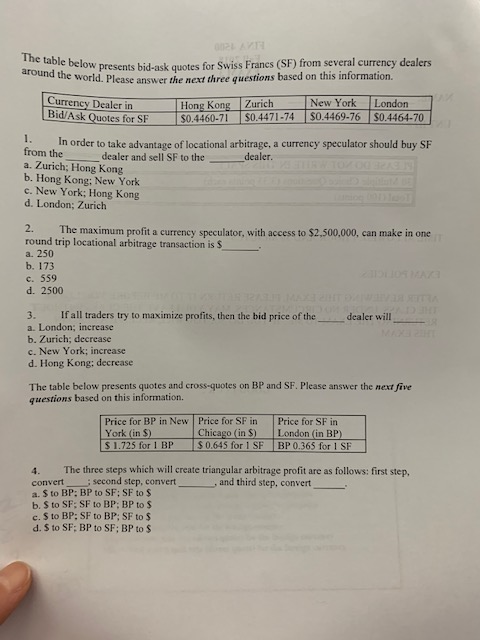

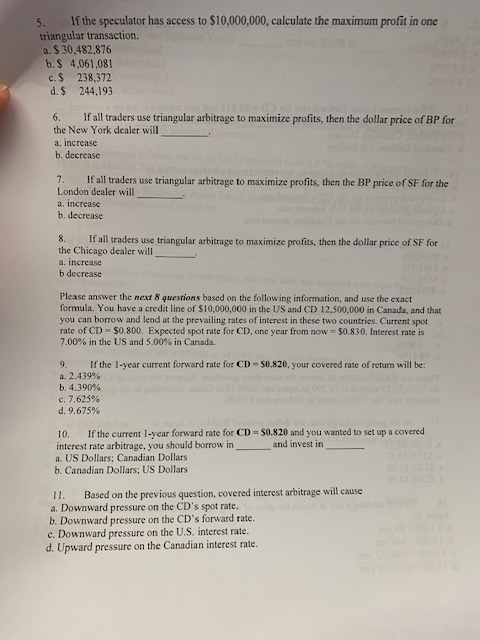

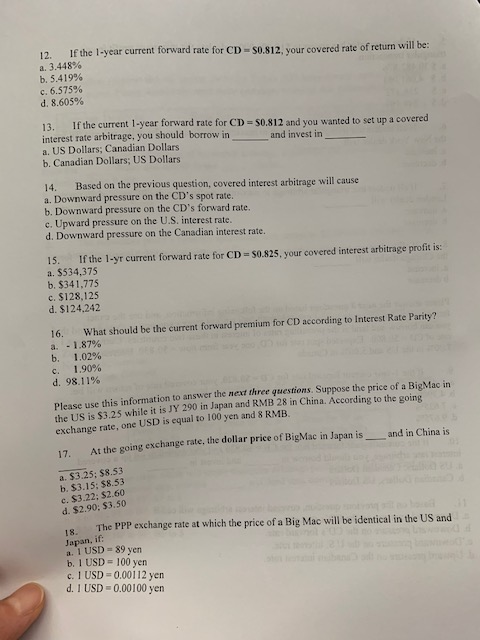

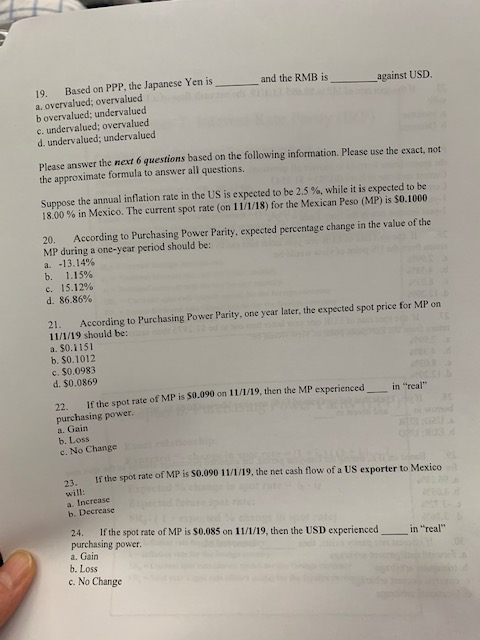

5. If the speculator has access to $10,000,000, calculate the maximum profit in one triangular transaction. a. $ 30,482,876 b. S 4,061,081 c, $ 238,372 d. $ 244,193 6. If all traders use triangular arbitrage to maximize profits, then the dollar price of BP for the New York dealer will a. increase b. decrease 7. If all traders use triangular arbitrage to maximize profits, then the BP price of SF for the London dealer will a. increase b decrease 8. If all traders use triangular arbitrage to maximize profits, then the dollar price of SF for the Chicago dealer will a. increase b decrease Please answer the next 8 questions based on the following information, and use the exact formula. You have a credit line of $10,000,000 in the US and CD 12,500,000 in Canada, and that you can borrow and lend at the prevailing rates of interest in these two countries. Current spot rate of CD- $0.800. Expected spot rate for CD, one year from now s0.830. Interest rate is 7.00% in the US and 5.00% in Canada. 9. If the 1-year current forward rate for CD- S0.820, your covered rate of return will be: a. 2.439% b. 4.39096 c. 7.625% d. 9.675% 10" If the current l-year forward rate for CD S0.820 and you wanted to set up a covered interest rate arbitrage, you should borrow inand invest in a. US Dollars; Canadian Dollars b. Canadian Dollars; US Dollars I1. Based on the previous question, covered interest arbitrage will cause a. Downward pressure on the CD's spot rate. b. Downward pressure on the CD's forward rate. c. Downward pressure on the U.S. interest rate. d. Upward pressure on the Canadian interest rate. 12. If the 1-year current forward rate for CD s0.812, your covered rate of return will a. 3.448% b, 5.41 9% C. 6.575% d. 8.60590 13. If the current 1-year forward rate for CD interest rate arbitrage, you should borrow in a. US Dollars; Canadian Dollars b. Canadian Dollars; US Dollars s0.812 and you wanted to set up a covered and invest in 14. Based on the previous question, covered interest arbitrage will cause a. Downward pressure on the CD's spot rate. b. Downward pressure on the CD's forward rate. c. Upward pressure on the U.S. interest rate. d. Downward pressure on the Canadian interest rate. 1S. If the I-yr current forward rate for CD- s0.825, your covered interest arbitrage profit is: a. $534,375 b. $341,775 c. $128,125 d. $124.242 16. What should be the current forward premium for CD according to Interest Rate Parity? a. -1.87% 1.02% 1.90% d. 98.11% Please use this information to answer the next three questions. Suppose the price of a BigMac in the US is $3.25 while it is JY 290 in Japan and RMB 28 in China. According to the going exchange rate, one USD is equal to 100 yen and 8 RMB. At the going exchange rate, the dollar priee of BigMac in Japan is and in China is 17. a. $3.25; $8.53 b. $3.15: $8.53 C. $3.22; $2.60 d. $2.90: $3.50 1&. The PPP exchange rate at which the price of a Big Mac will be identical in the US and Japan, i a. 1 USD 89 yen b. 1 USD 100 yen c. 1 USD-0.00112 yen f: d. I USD 0.00100 yen 19. Based on PPP, the Japanese Yen is a. overvalued; overvalued b overvalued; undervalued c. undervalued; overvalued d. undervalued; undervalued and the RMB is against USD. Please answer the next 6 questions based on the following information. Please use the exact, not the approximate formula to answer all questions Suppose the annual inflation rate in the US is expected to be 2.5 %, while it is expected to be 18.00 % in Mexico. The current spot rate (on 1 1/1/18) for the Mexican Peso (MP) is $0.1000 20. According to Purchasing Power Parity, expected percentage change in the value of the MP during a one-year period should be: a. -13.14% b. 1.15% c. 15.12% d. 86.86% 21. According to Purchasing Power Parity, one year later, the expected spot price for MP on 11/1/19 should be: a $0.1151 b. $0.1012 c. $0.0983 d. $0.0869 22. If the spot rate of MP is $0.090 on 11/1/19, then the MP ex purchasing power. a. Gain b. Loss c. No Change real" If the spot rate of MP is S0.090 11/1/19, the net cash flow of a US exporter to Mexico 23 will: a. Increase b. Decrease 24. If the spot rate of MP is $0.085 on 11/1/19, then the USD experiencedin"real" purchasing power a. Gain b. Loss c. No Change 25. If the spot rate of MP is s0.085 11/1/19, the net cash flow of a US importer from Mexico will: a. Increase b. Decrease Please answer the next 4 questions based on the following information. Please use the exact, not the approximate formula to answer all questions. Current spot rate of Euro (EUR) S1.3543 Current 1-year forward rate for EUR- $1.2908 1-year interest rate in the US,-3.5% 1-year interest rate in the Euro Zone-7.5% 26. If the spot rate of EUR one year latter turn out to be S1.2975, then uncovered rate of return from the US point of view would be: a. 2.99% b, 4.38% . 8.03% d. 12.20% 27. f the spot rate of EUR one year latter turn out to be $1.2975 then uncovered rate of return from the European point of view would be: a. 2.99% b. 4.38% c. 8.03% d. 12.20% 28. If you knew that the spot rate of EUR one year later would be $1.2975, then you should borrow inand invest in a. USD; EUR b. EUR: USD 29. Based on IFE, during the onc-year period, the expected percentage change in the spot rate for EUR should be: 296 28% b. 4.05% c.-3.72% d. 3.86% 30. If interest rate parity exists, thenis not feasible. a. forward realignment arbitrage b. triangular arbitrage c. covered interest arbitrage d. locational arbitrage

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts