Question: I only need answers for question 3 and question 7. Chapter 15 Revision of the Equity Portfolio 441 3. Consider the information in the following

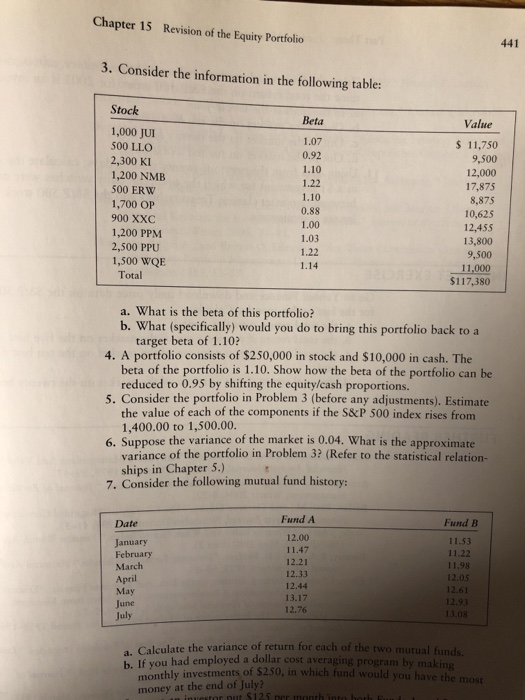

Chapter 15 Revision of the Equity Portfolio 441 3. Consider the information in the following table: Stock Beta Value 1,000 JUI 500 LLO 2,300 KI 1,200 NMB 500 ERW 1,700 OP 900 XXC 1,200 PPM 2,500 PPU 1,500 WQ 1.07 0.92 1.10 1.22 1.10 0.88 1.00 1.03 1.22 1.14 11,750 9,500 12,000 17,875 8,875 10,625 12,455 13,800 9,500 11,000 $117,380 Total a. What is the beta of this portfolio? b. What (specifically) would you do to bring this portfolio back to a target beta of 1.10? 4. A portfolio consists of $250,000 in stock and $10,000 in cash. The 5. Consider the portfolio in Problem 3 (before any adjustments). Estimate 6. Suppose the variance of the market is 0.04. What is the approximate 7. Consider the following mutual fund history: beta of the portfolio is 1.10. Show how the beta of the portfolio can be reduced to 0.95 by shifting the equity/cash proportions. the value of each of the components if the S&P 500 index rises from 1,400.00 to 1,500.00. variance of the portfolio in Problem 3? (Refer to the statistical relation- ships in Chapter 5.) Fund A Fund B 11.53 11.22 11.98 12.05 Date January February March April May 12.00 11.47 12.21 12.33 12.44 13.17 12.76 July a. Calculate the variance of return for each of the two mutual funds. b. If you had em ployed a dollar cost averaging program by makin onthly investments of $250, in which fund would you hav money at the end of July

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts