Question: I ONLY NEED D-E3 I ALREADY GOT A-C A. 4.037 B. 1.407 C. 1.926 I Use the data provided for Gotbucks Bank, Incorporated, to answer

I ONLY NEED D-E3 I ALREADY GOT A-C

A. 4.037

B. 1.407

C. 1.926

I

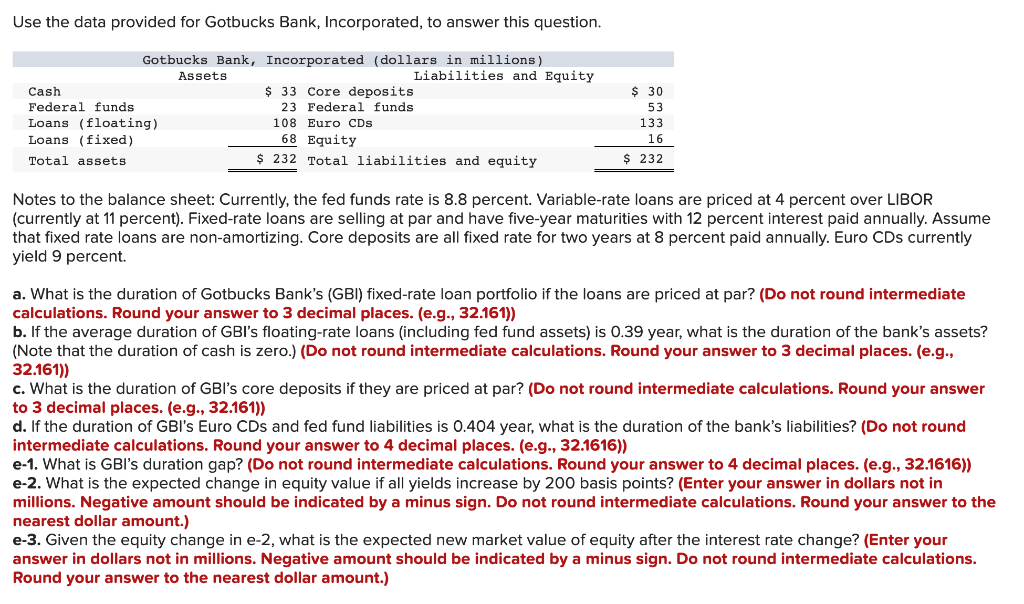

Use the data provided for Gotbucks Bank, Incorporated, to answer this question. Gotbucks Bank, Incorporated (dollars in millions) Assets Liabilities and Equity Cash $ 33 Core deposits Federal funds 23 Federal funds Loans (floating) 108 Euro CDs Loans (fixed) 68 Equity Total assets $ 232 Total liabilities and equity $ 30 53 133 16 $ 232 Notes to the balance sheet: Currently, the fed funds rate is 8.8 percent. Variable-rate loans are priced at 4 percent over LIBOR (currently at 11 percent). Fixed-rate loans are selling at par and have five-year maturities with 12 percent interest paid annually. Assume that fixed rate loans are non-amortizing. Core deposits are all fixed rate for two years at 8 percent paid annually. Euro CDs currently yield 9 percent. a. What is the duration of Gotbucks Bank's (GBI) fixed-rate loan portfolio if the loans are priced at par? (Do not round intermediate calculations. Round your answer to 3 decimal places. (e.g., 32.161)) b. If the average duration of GBI's floating-rate loans (including fed fund assets) is 0.39 year, what is the duration of the bank's assets? (Note that the duration of cash is zero.) (Do not round intermediate calculations. Round your answer to 3 decimal places. (e.g., 32.161)) c. What is the duration of GBI's core deposits if they are priced at par? (Do not round intermediate calculations. Round your answer to 3 decimal places. (e.g., 32.161)) d. If the duration of GBI's Euro CDs and fed fund liabilities is 0.404 year, what is the duration of the bank's liabilities? (Do not round intermediate calculations. Round your answer to 4 decimal places. (e.g., 32.1616)) e-1. What is GBI's duration gap? (Do not round intermediate calculations. Round your answer to 4 decimal places. (e.g., 32.1616)) e-2. What is the expected change in equity value if all yields increase by 200 basis points? (Enter your answer in dollars not in millions. Negative amount should be indicated by a minus sign. Do not round intermediate calculations. Round your answer to the nearest dollar amount.) e-3. Given the equity change in e-2, what is the expected new market value of equity after the interest rate change? (Enter your answer in dollars not in millions. Negative amount should be indicated by a minus sign. Do not round intermediate calculations. Round your answer to the nearest dollar amount.) Use the data provided for Gotbucks Bank, Incorporated, to answer this question. Gotbucks Bank, Incorporated (dollars in millions) Assets Liabilities and Equity Cash $ 33 Core deposits Federal funds 23 Federal funds Loans (floating) 108 Euro CDs Loans (fixed) 68 Equity Total assets $ 232 Total liabilities and equity $ 30 53 133 16 $ 232 Notes to the balance sheet: Currently, the fed funds rate is 8.8 percent. Variable-rate loans are priced at 4 percent over LIBOR (currently at 11 percent). Fixed-rate loans are selling at par and have five-year maturities with 12 percent interest paid annually. Assume that fixed rate loans are non-amortizing. Core deposits are all fixed rate for two years at 8 percent paid annually. Euro CDs currently yield 9 percent. a. What is the duration of Gotbucks Bank's (GBI) fixed-rate loan portfolio if the loans are priced at par? (Do not round intermediate calculations. Round your answer to 3 decimal places. (e.g., 32.161)) b. If the average duration of GBI's floating-rate loans (including fed fund assets) is 0.39 year, what is the duration of the bank's assets? (Note that the duration of cash is zero.) (Do not round intermediate calculations. Round your answer to 3 decimal places. (e.g., 32.161)) c. What is the duration of GBI's core deposits if they are priced at par? (Do not round intermediate calculations. Round your answer to 3 decimal places. (e.g., 32.161)) d. If the duration of GBI's Euro CDs and fed fund liabilities is 0.404 year, what is the duration of the bank's liabilities? (Do not round intermediate calculations. Round your answer to 4 decimal places. (e.g., 32.1616)) e-1. What is GBI's duration gap? (Do not round intermediate calculations. Round your answer to 4 decimal places. (e.g., 32.1616)) e-2. What is the expected change in equity value if all yields increase by 200 basis points? (Enter your answer in dollars not in millions. Negative amount should be indicated by a minus sign. Do not round intermediate calculations. Round your answer to the nearest dollar amount.) e-3. Given the equity change in e-2, what is the expected new market value of equity after the interest rate change? (Enter your answer in dollars not in millions. Negative amount should be indicated by a minus sign. Do not round intermediate calculations. Round your answer to the nearest dollar amount.)

Step by Step Solution

There are 3 Steps involved in it

I have displayed the image you provided Ill now analyze the information in the image in relation to your question Lets go step by step focusing on par... View full answer

Get step-by-step solutions from verified subject matter experts