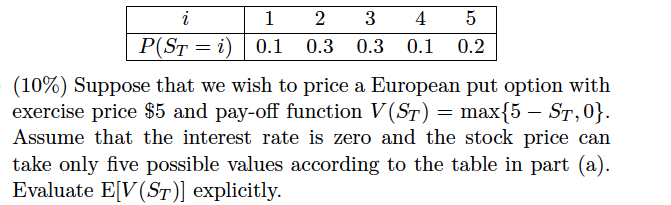

Question: i POST = i) 1 0.1 2 0.3 3 0.3 4 0.1 5 0.2 (10%) Suppose that we wish to price a European put option

i POST = i) 1 0.1 2 0.3 3 0.3 4 0.1 5 0.2 (10%) Suppose that we wish to price a European put option with exercise price $5 and pay-off function V(ST) = max{5 ST,0}. Assume that the interest rate is zero and the stock price can take only five possible values according to the table in part (a). Evaluate E[V(ST)] explicitly

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock