Question: i want full answer if you can please. it will be helpful. However I can understand that according to your policy sometimes you can only

i want full answer if you can please. it will be helpful. However I can understand that according to your policy sometimes you can only answer 1 part. so if you gone answer only one part so please answer part g.

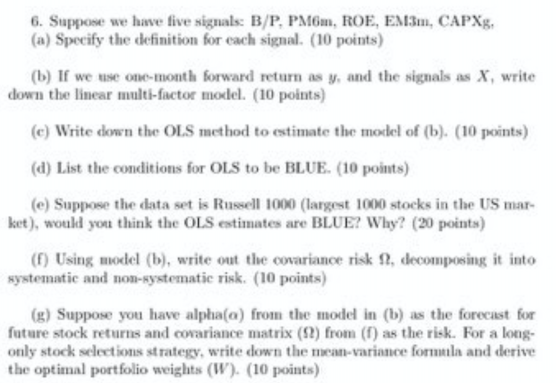

6. Suppose we have five signals: B/P, PM6m, ROE, EM3m, CAPXg, (a) Specify the definition for each signal. (10 points) (b) If we use one-month forward return as y, and the signals as X, write down the linear multi-factor model. (10 points) (c) Write down the OLS method to estimate the model of (b). (10 points) (d) List the conditions for OLS to be BLUE. (10 points) (e) Suppose the data set is Russell 1000 (largest 1000 stocks in the US mar- ket), would you think the OLS estimates are BLUE? Why? (20 points) (f) Using model (b), write out the covariance risk A, decomposing it into systematic and non-systematic risk. (10 points) (g) Suppose you have alpha(a) from the model in (b) as the forecast for future stock returns and covariance matrix (12) from (1) as the risk. For a long- only stock selections strategy, write down the mean-variance formula and derive the optimal portfolio weights (W). (10 points) 6. Suppose we have five signals: B/P, PM6m, ROE, EM3m, CAPXg, (a) Specify the definition for each signal. (10 points) (b) If we use one-month forward return as y, and the signals as X, write down the linear multi-factor model. (10 points) (c) Write down the OLS method to estimate the model of (b). (10 points) (d) List the conditions for OLS to be BLUE. (10 points) (e) Suppose the data set is Russell 1000 (largest 1000 stocks in the US mar- ket), would you think the OLS estimates are BLUE? Why? (20 points) (f) Using model (b), write out the covariance risk A, decomposing it into systematic and non-systematic risk. (10 points) (g) Suppose you have alpha(a) from the model in (b) as the forecast for future stock returns and covariance matrix (12) from (1) as the risk. For a long- only stock selections strategy, write down the mean-variance formula and derive the optimal portfolio weights (W). (10 points)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts