Question: I want the answer for this question, thanks! A derivative security of European style with expiration in 1 year has the following payoff+ max (0,

I want the answer for this question, thanks!

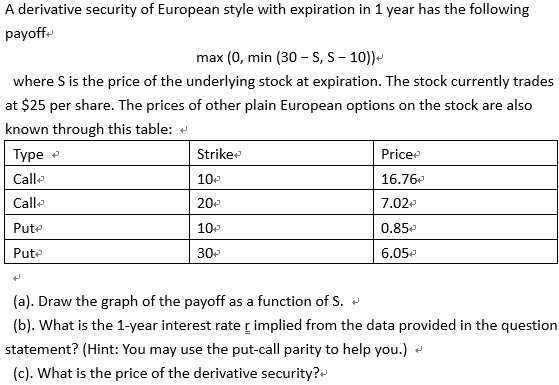

A derivative security of European style with expiration in 1 year has the following payoff+ max (0, min (30 - 5, 5 - 10))+ where S is the price of the underlying stock at expiration. The stock currently trades at $25 per share. The prices of other plain European options on the stock are also known through this table: + Type + Strike+ Price+ Call+ 10+ 16.76+ Call+ 20+ 7.02+ Put+ 10+ 0.85+ Put+ 6.05+7 (a). Draw the graph of the payoff as a function of S. + (b). What is the 1-year interest rate r implied from the data provided in the question statement? (Hint: You may use the put-call parity to help you.) . (c). What is the price of the derivative security?+

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts