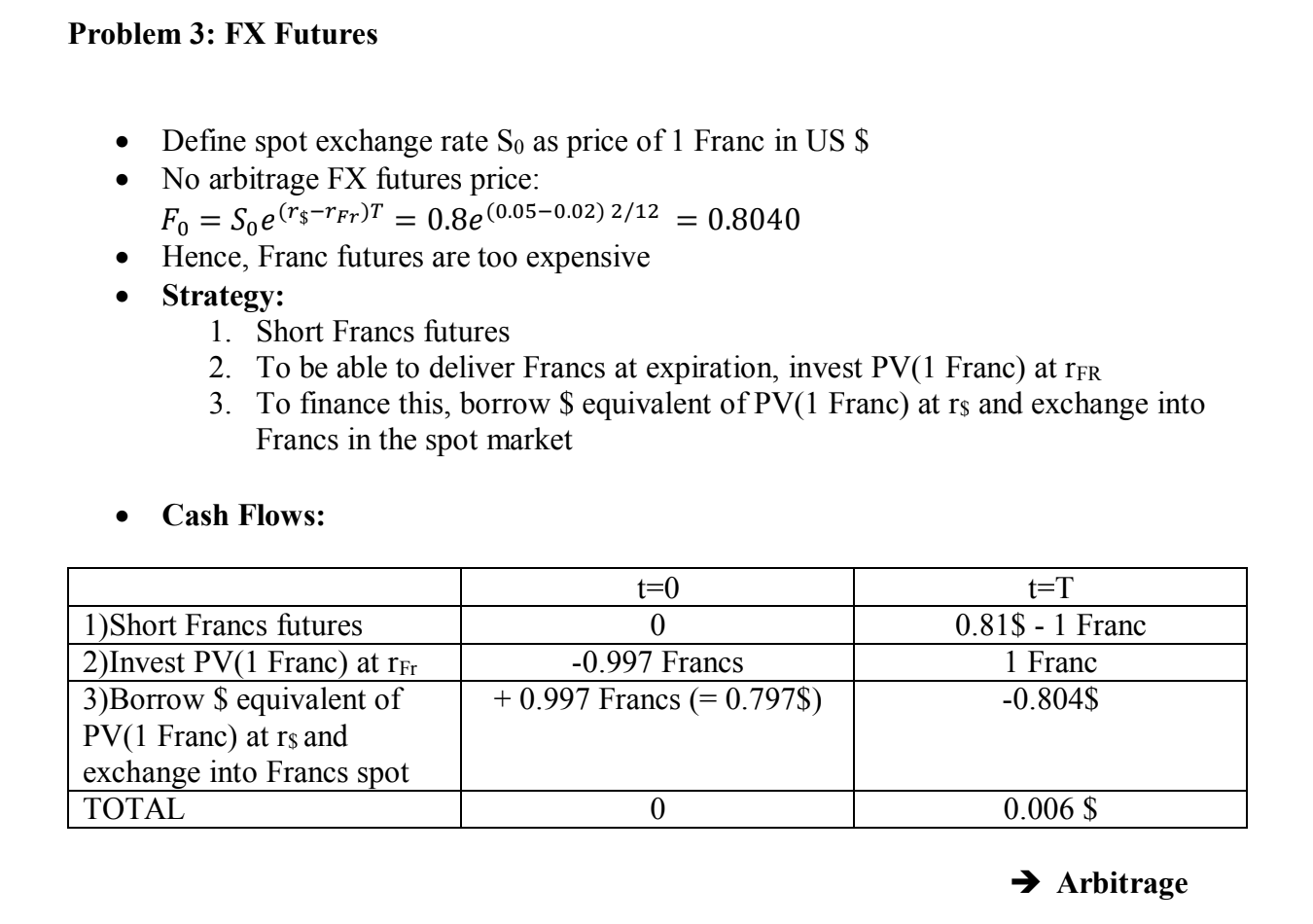

Question: I will send you the question and solution ( uploaded ) . I do not understand the solution. QUESTION: The two - month interest rates

I will send you the question and solution uploaded I do not understand the solution. QUESTION: The twomonth interest rates in Switzerland and the United States are and per annum, respectively, with continuous compounding. The spot price of the Swiss franc is $ The futures price for a contract deliverable in two months is $ What arbitrage opportunities does this create?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock