Question: I would appreciate having a solution written with nice handwriting and detail explanations W is a positive definite covariance matrix. 4. covariance matrix of VNVQTb

I would appreciate having a solution written with nice handwriting and detail explanations

W is a positive definite covariance matrix.

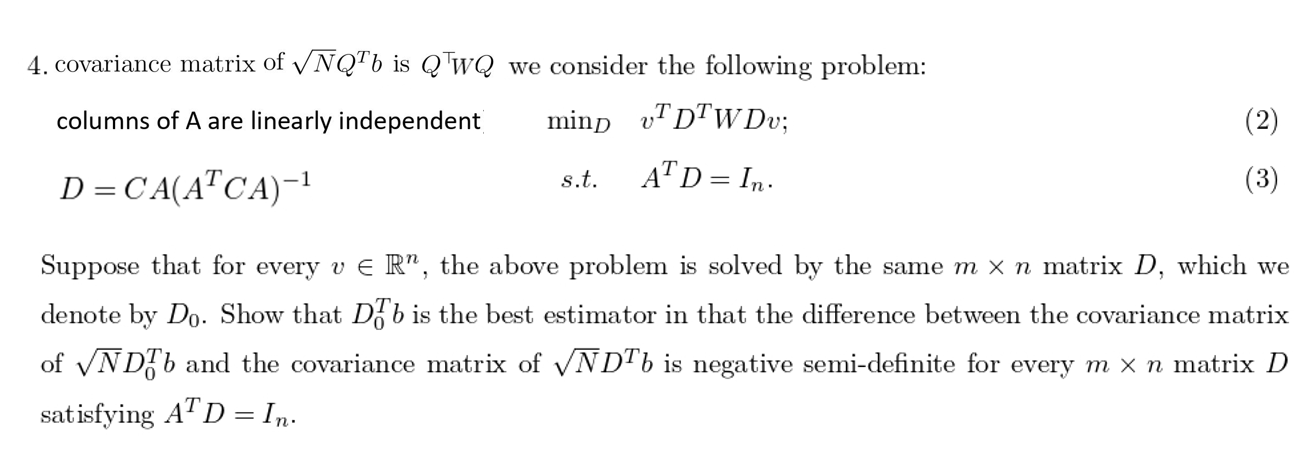

4. covariance matrix of VNVQTb is Q wQ we consider the following problem: columns of A are linearly independent ming UTDTWDv; (2) D = CA(ATCA)-1 s.t. ATD = In. (3) Suppose that for every v E R", the above problem is solved by the same m x n matrix D, which we denote by Do. Show that Do b is the best estimator in that the difference between the covariance matrix of VND, b and the covariance matrix of VND"b is negative semi-definite for every m x n matrix D satisfying ATD = In

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock