Question: IAS 3 8 - Intangible Assets - was primarily issued in order to identify the criteria that need to be present before expenditure on intangible

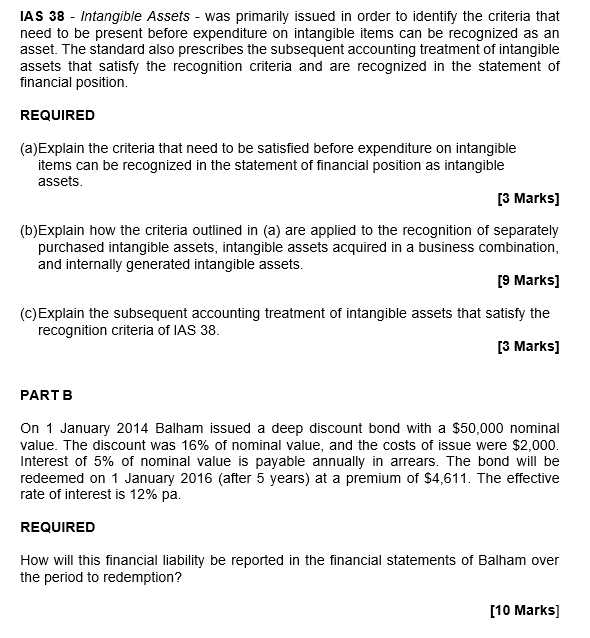

IAS Intangible Assets was primarily issued in order to identify the criteria that need to be present before expenditure on intangible items can be recognized as an asset. The standard also prescribes the subsequent accounting treatment of intangible assets that satisfy the recognition criteria and are recognized in the statement of financial position. REQUIRED aExplain the criteria that need to be satisfied before expenditure on intangible items can be recognized in the statement of financial position as intangible assets. MarksbExplain how the criteria outlined in a are applied to the recognition of separately purchased intangible assets, intangible assets acquired in a business combination, and internally generated intangible assets. Marksc Explain the subsequent accounting treatment of intangible assets that satisfy the recognition criteria of IAS Marks PART B On January Balham issued a deep discount bond with a $ nominal value. The discount was of nominal value, and the costs of issue were $ Interest of of nominal value is payable annually in arrears. The bond will be redeemed on January after years at a premium of $ The effective rate of interest is pa REQUIRED How will this financial liability be reported in the financial statements of Balham over the period to redemption?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock