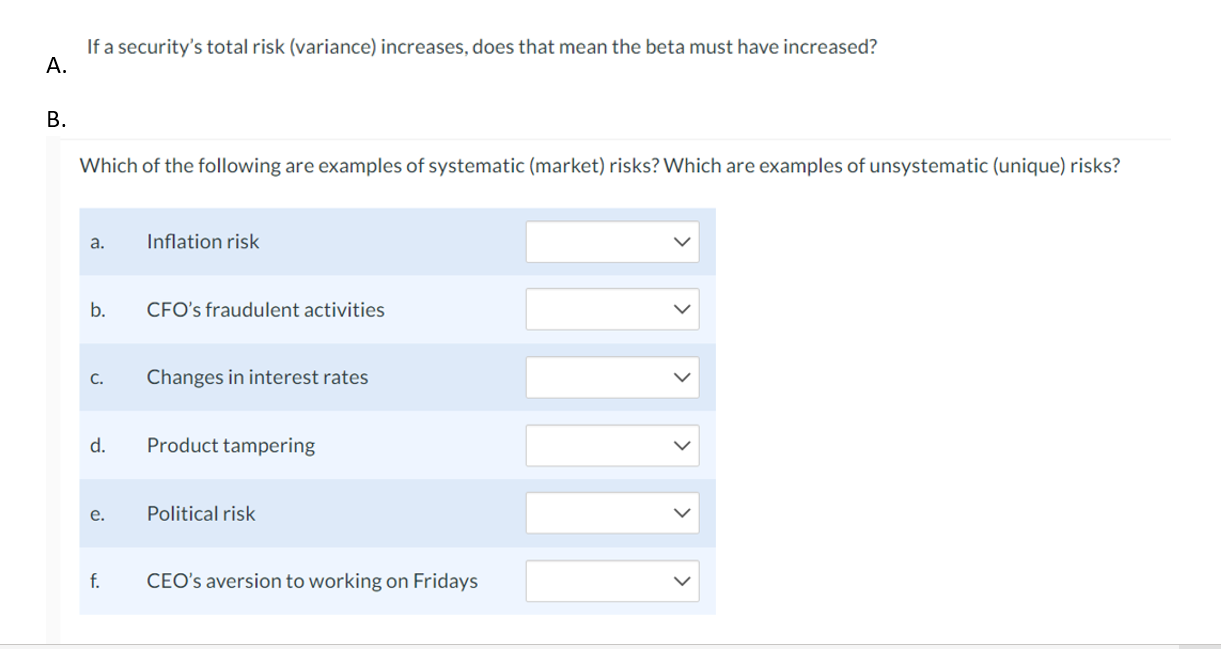

Question: If a security's total risk (variance) increases, does that mean the beta must have increased? Which of the following are examples of systematic (market) risks?

If a security's total risk (variance) increases, does that mean the beta must have increased? Which of the following are examples of systematic (market) risks? Which are examples of unsystematic (unique) risks

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock