Question: If no commodity arbitrage exists, then mention that no arbitrage strategy exists. Question 3 The following table contains information on spot and forward exchange rates

If no commodity arbitrage exists, then mention that no arbitrage strategy exists.

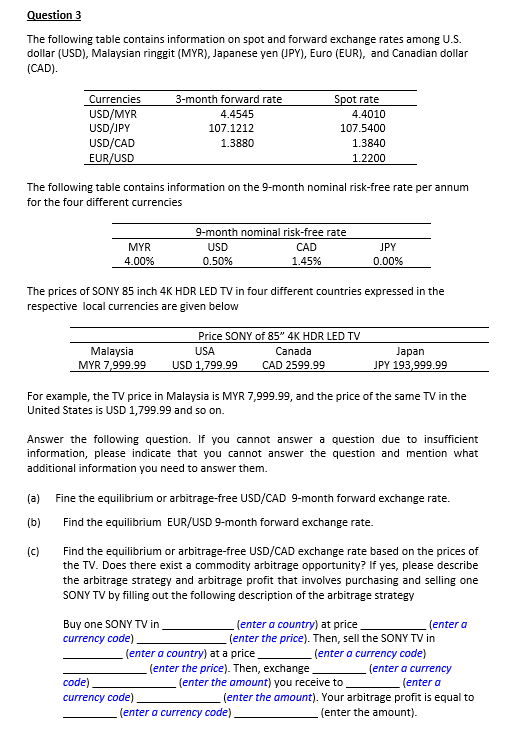

Question 3 The following table contains information on spot and forward exchange rates among U.S. dollar (USD), Malaysian ringgit (MYR), Japanese yen (JPY), Euro (EUR), and Canadian dollar (CAD). Currencies USD/MYR USD/JPY USD/CAD EUR/USD 3-month forward rate 4.4545 107.1212 1.3880 Spot rate 4.4010 107.5400 1.3840 1.2200 The following table contains information on the 9-month nominal risk-free rate per annum for the four different currencies MYR 4.00% 9-month nominal risk-free rate USD CAD 0.50% 1.45% JPY 0.00% The prices of SONY 85 inch 4K HDR LED TV in four different countries expressed in the respective local currencies are given below Malaysia MYR 7,999.99 Price SONY of 85" 4K HDR LED TV USA Canada USD 1,799.99 CAD 2599.99 Japan JPY 193,999.99 For example, the TV price in Malaysia is MYR 7,999.99, and the price of the same TV in the United States is USD 1,799.99 and so on. Answer the following question. If you cannot answer a question due to insufficient information, please indicate that you cannot answer the question and mention what additional information you need to answer them. (a) Fine the equilibrium or arbitrage-free USD/CAD 9-month forward exchange rate. (b) Find the equilibrium EUR/USD 9-month forward exchange rate. (c) Find the equilibrium or arbitrage-free USD/CAD exchange rate based on the prices of the TV. Does there exist a commodity arbitrage opportunity? If yes, please describe the arbitrage strategy and arbitrage profit that involves purchasing and selling one SONY TV by filling out the following description of the arbitrage strategy Buy one SONY TV in (enter a country) at price (enter a currency code). lenter the price). Then, sell the SONY TV in (enter a country) at a price (enter a currency code) (enter the price). Then, exchange (enter a currency code) (enter the amount) you receive to (enter a currency code) (enter the amount). Your arbitrage profit is equal to (enter a currency code) (enter the amount)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts