Question: II. Asset Allocation (35 points) a) Define mean/variance asset allocation optimization. Include an appropriate objective function and two constraints in your answer (either in

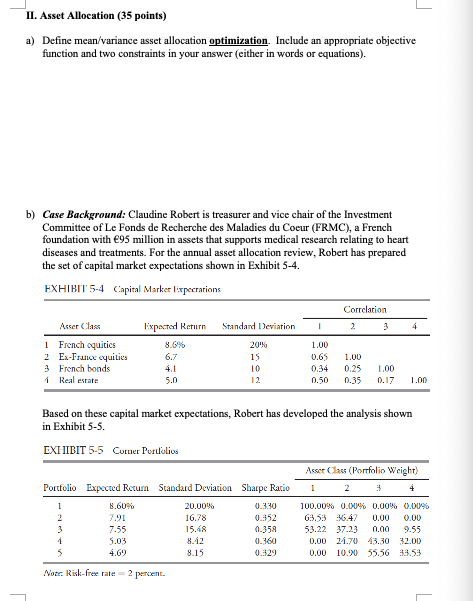

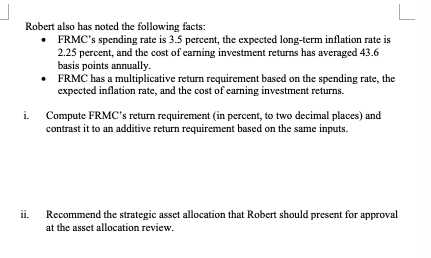

II. Asset Allocation (35 points) a) Define mean/variance asset allocation optimization. Include an appropriate objective function and two constraints in your answer (either in words or equations). b) Case Background: Claudine Robert is treasurer and vice chair of the Investment Committee of Le Fonds de Recherche des Maladies du Coeur (FRMC), a French foundation with 95 million in assets that supports medical research relating to heart diseases and treatments. For the annual asset allocation review, Robert has prepared the set of capital market expectations shown in Exhibit 5-4. EXHIBIT 5-4 Capital Marker lixpectations Correlation Asser Class Expected Return Standard Deviation 2 3 4 1 French equities 8.6% 20% 1.00 2 Ex-France equities 6.7 15 0.65 1.00 3 French bonds 4.1 10 0.34 0.25 1.00 1 Real estate 5.0 12 0.50 0.35 0.17 1.00 Based on these capital market expectations, Robert has developed the analysis shown in Exhibit 5-5. EXHIBIT 5-5 Corner Portfolios Asser Class (Portfolio Weight) Portfolio Expected Return Standard Deviation Sharpe Ratio 1 2 3 4 1 8.60% 20.00% 0.330 2 7.91 16.78 0.352 3 7.55 15.48 0.358 4 5.03 8.42 0.360 4.69 8.15 0.329 100.00% 0.00% 0.00% 0.00% 63.53 36.47 0.00 0.00 53.22 37.23 0.00 9.55 0.00 24.70 43.30 32.00 0.00 10.90 55.56 33.53 Note: Risk-free rate 2 percent. Robert also has noted the following facts: i. FRMC's spending rate is 3.5 percent, the expected long-term inflation rate is 2.25 percent, and the cost of earning investment returns has averaged 43.6 basis points annually. FRMC has a multiplicative return requirement based on the spending rate, the expected inflation rate, and the cost of earning investment returns. Compute FRMC's return requirement (in percent, to two decimal places) and contrast it to an additive return requirement based on the same inputs. ii. Recommend the strategic asset allocation that Robert should present for approval at the asset allocation review. L

Step by Step Solution

3.48 Rating (151 Votes )

There are 3 Steps involved in it

a MeanVariance Asset Allocation Optimization MeanVariance asset allocation optimization is a quantitative approach used to determine the optimal alloc... View full answer

Get step-by-step solutions from verified subject matter experts