Question: III - Dividend Discount Model Valuation (30 points - 60 minutes) June Withers is analyzing four stocks in the processed food industry as of 31

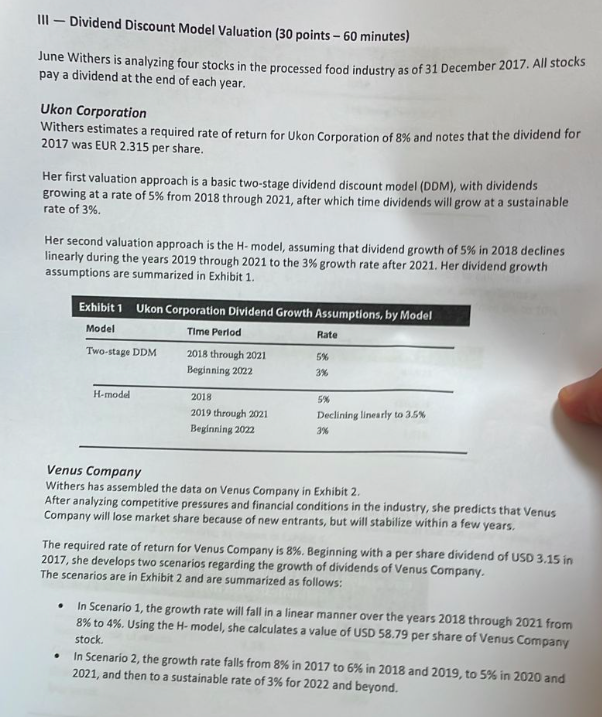

III - Dividend Discount Model Valuation (30 points - 60 minutes) June Withers is analyzing four stocks in the processed food industry as of 31 December 2017. All stocks pay a dividend at the end of each year. Ukon Corporation Withers estimates a required rate of return for Ukon Corporation of 8% and notes that the dividend for 2017 was EUR 2.315 per share. Her first valuation approach is a basic two-stage dividend discount model (DDM), with dividends growing at a rate of 5% from 2018 through 2021, after which time dividends will grow at a sustainable rate of 3%. Her second valuation approach is the H-model, assuming that dividend growth of 5% in 2018 declines linearly during the years 2019 through 2021 to the 3% growth rate after 2021. Her dividend growth assumptions are summarized in Exhibit 1. Time Period Exhibiti Ukon Corporation Dividend Growth Assumptions, by Model Model Two-stage DDM 2018 through 2021 Beginning 2022 Rate 5% 3% H-modd 2018 2019 through 2021 Beginning 2022 5% Declining linearly to 3.5% 3% Venus Company Withers has assembled the data on Venus Company in Exhibit 2. After analyzing competitive pressures and financial conditions in the industry, she predicts that Venus Company will lose market share because of new entrants, but will stabilize within a few years. The required rate of return for Venus Company is 8%. Beginning with a per share dividend of USD 3.15 in 2017, she develops two scenarios regarding the growth of dividends of Venus Company The scenarios are in Exhibit 2 and are summarized as follows: In Scenario 1, the growth rate will fall in a linear manner over the years 2018 through 2021 from 8% to 4%. Using the H-model, she calculates a value of USD 58.79 per share of Venus Company stock. In Scenario 2, the growth rate falls from 8% in 2017 to 6% in 2018 and 2019, to 5% in 2020 and 2021, and then to a sustainable rate of 3% for 2022 and beyond. Questions (Show your work when specified): 1. Based on Exhibit 1, when Withers applies the first valuation approach to Ukon Corporation, the estimated value of the stock at the end of the first stage represents the: A. present value of the dividends beyond year 2021. B. present value of the dividends for years 2018 through 2021. C. sum of the present value of the dividends for 2018 through 2021 and the present value of dividends beyond year 2021. Answer: 2. Using her first valuation approach and Exhibit 1, Withers's forecast of the per share stock value of Ukon Corporation at the end of 2017 should be closest to: A. EUR 48. B. EUR 50. C. EUR 51. Answer: (show your work below) III - Dividend Discount Model Valuation (30 points - 60 minutes) June Withers is analyzing four stocks in the processed food industry as of 31 December 2017. All stocks pay a dividend at the end of each year. Ukon Corporation Withers estimates a required rate of return for Ukon Corporation of 8% and notes that the dividend for 2017 was EUR 2.315 per share. Her first valuation approach is a basic two-stage dividend discount model (DDM), with dividends growing at a rate of 5% from 2018 through 2021, after which time dividends will grow at a sustainable rate of 3%. Her second valuation approach is the H-model, assuming that dividend growth of 5% in 2018 declines linearly during the years 2019 through 2021 to the 3% growth rate after 2021. Her dividend growth assumptions are summarized in Exhibit 1. Time Period Exhibiti Ukon Corporation Dividend Growth Assumptions, by Model Model Two-stage DDM 2018 through 2021 Beginning 2022 Rate 5% 3% H-modd 2018 2019 through 2021 Beginning 2022 5% Declining linearly to 3.5% 3% Venus Company Withers has assembled the data on Venus Company in Exhibit 2. After analyzing competitive pressures and financial conditions in the industry, she predicts that Venus Company will lose market share because of new entrants, but will stabilize within a few years. The required rate of return for Venus Company is 8%. Beginning with a per share dividend of USD 3.15 in 2017, she develops two scenarios regarding the growth of dividends of Venus Company The scenarios are in Exhibit 2 and are summarized as follows: In Scenario 1, the growth rate will fall in a linear manner over the years 2018 through 2021 from 8% to 4%. Using the H-model, she calculates a value of USD 58.79 per share of Venus Company stock. In Scenario 2, the growth rate falls from 8% in 2017 to 6% in 2018 and 2019, to 5% in 2020 and 2021, and then to a sustainable rate of 3% for 2022 and beyond. Questions (Show your work when specified): 1. Based on Exhibit 1, when Withers applies the first valuation approach to Ukon Corporation, the estimated value of the stock at the end of the first stage represents the: A. present value of the dividends beyond year 2021. B. present value of the dividends for years 2018 through 2021. C. sum of the present value of the dividends for 2018 through 2021 and the present value of dividends beyond year 2021. Answer: 2. Using her first valuation approach and Exhibit 1, Withers's forecast of the per share stock value of Ukon Corporation at the end of 2017 should be closest to: A. EUR 48. B. EUR 50. C. EUR 51. Answer: (show your work below)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts