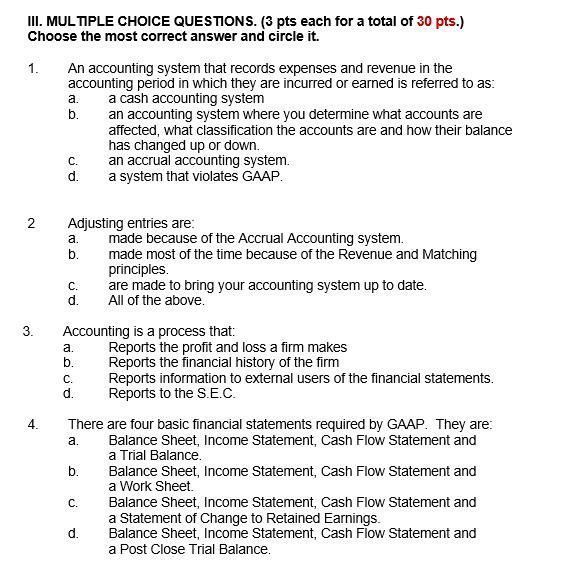

Question: III. MULTIPLE CHOICE QUESTIONS. (3 pts each for a total of 30 pts.) Choose the most correct answer and circle it. 1. An accounting system

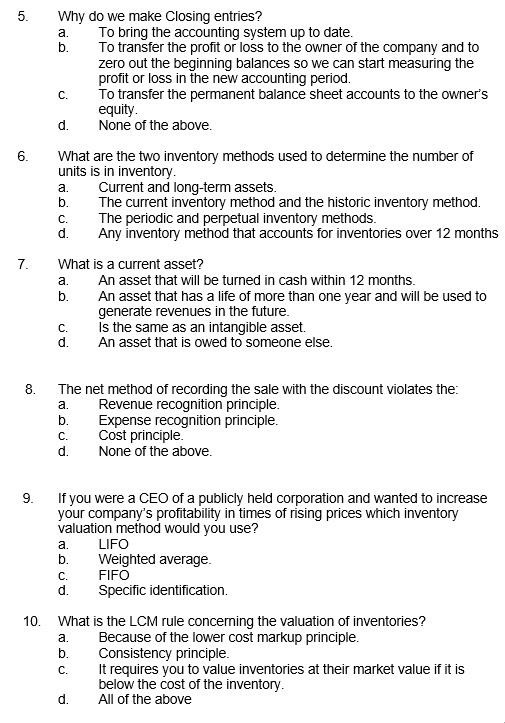

III. MULTIPLE CHOICE QUESTIONS. (3 pts each for a total of 30 pts.) Choose the most correct answer and circle it. 1. An accounting system that records expenses and revenue in the accounting period in which they are incurred or earned is referred to as: a cash accounting system b. an accounting system where you determine what accounts are affected, what classification the accounts are and how their balance has changed up or down. an accrual accounting system. d. a system that violates GAAP. a C. 2 a. 3. a. C. Adjusting entries are: made because of the Accrual Accounting system. b. made most of the time because of the Revenue and Matching principles. C. are made to bring your accounting system up to date. d. All of the above. Accounting is a process that: Reports the profit and loss a firm makes b. Reports the financial history of the firm Reports information to external users of the financial statements. d. Reports to the S.E.C. There are four basic financial statements required by GAAP. They are: Balance Sheet, Income Statement, Cash Flow Statement and a Trial Balance b. Balance Sheet, Income Statement, Cash Flow Statement and a Work Sheet C. Balance Sheet, Income Statement, Cash Flow Statement and a Statement of Change to Retained Earnings. d. Balance Sheet, Income Statement, Cash Flow Statement and a Post Close Trial Balance. 4. a. 5. a. b. C. 6. Why do we make Closing entries? To bring the accounting system up to date. To transfer the profit or loss to the owner of the company and to zero out the beginning balances so we can start measuring the profit or loss in the new accounting period. To transfer the permanent balance sheet accounts to the owner's equity. d. None of the above. What are the two inventory methods used to determine the number of units is in inventory. Current and long-term assets. b. The current inventory method and the historic inventory method. The periodic and perpetual inventory methods. d. Any inventory method that accounts for inventories over 12 months What is a current asset? An asset that will be turned in cash within 12 months. b. An asset that has a life of more than one year and will be used to generate revenues in the future. is the same as an intangible asset. d. An asset that is owed to someone else. a C. 7. a. C. 8. a. The net method of recording the sale with the discount violates the Revenue recognition principle. b. Expense recognition principle. C. Cost principle. d. None of the above. 9. a. C. If you were a CEO of a publicly held corporation and wanted to increase your company's profitability in times of rising prices which inventory valuation method would you use? LIFO b. Weighted average. FIFO d. Specific identification. What is the LCM rule concerning the valuation of inventories? Because of the lower cost markup principle. b. Consistency principle. C. It requires you to value inventories at their market value if it is below the cost of the inventory. All of the above 10. a. d

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts