Question: I'm not sure how they got that answer Suppose that a company enters into a FRA that is designed to ensure it will receive a

I'm not sure how they got that answer

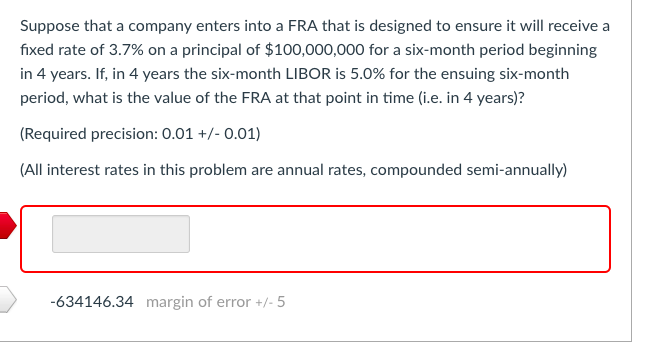

Suppose that a company enters into a FRA that is designed to ensure it will receive a fixed rate of 3.7% on a principal of $100,000,000 for a six-month period beginning in 4 years. If, in 4 years the six-month LIBOR is 5.0% for the ensuing six-month period, what is the value of the FRA at that point in time (i.e. in 4 years)? (Required precision: 0.01 +/- 0.01) All interest rates in this problem are annual rates, compounded semi-annually) -634146.34 margin of error+-5

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock