Question: I'm not sure how to do part (e). How do i prove the equation? 1. [10 marks] CRR model: European contingent claim. Consider the CRR

I'm not sure how to do part (e). How do i prove the equation?

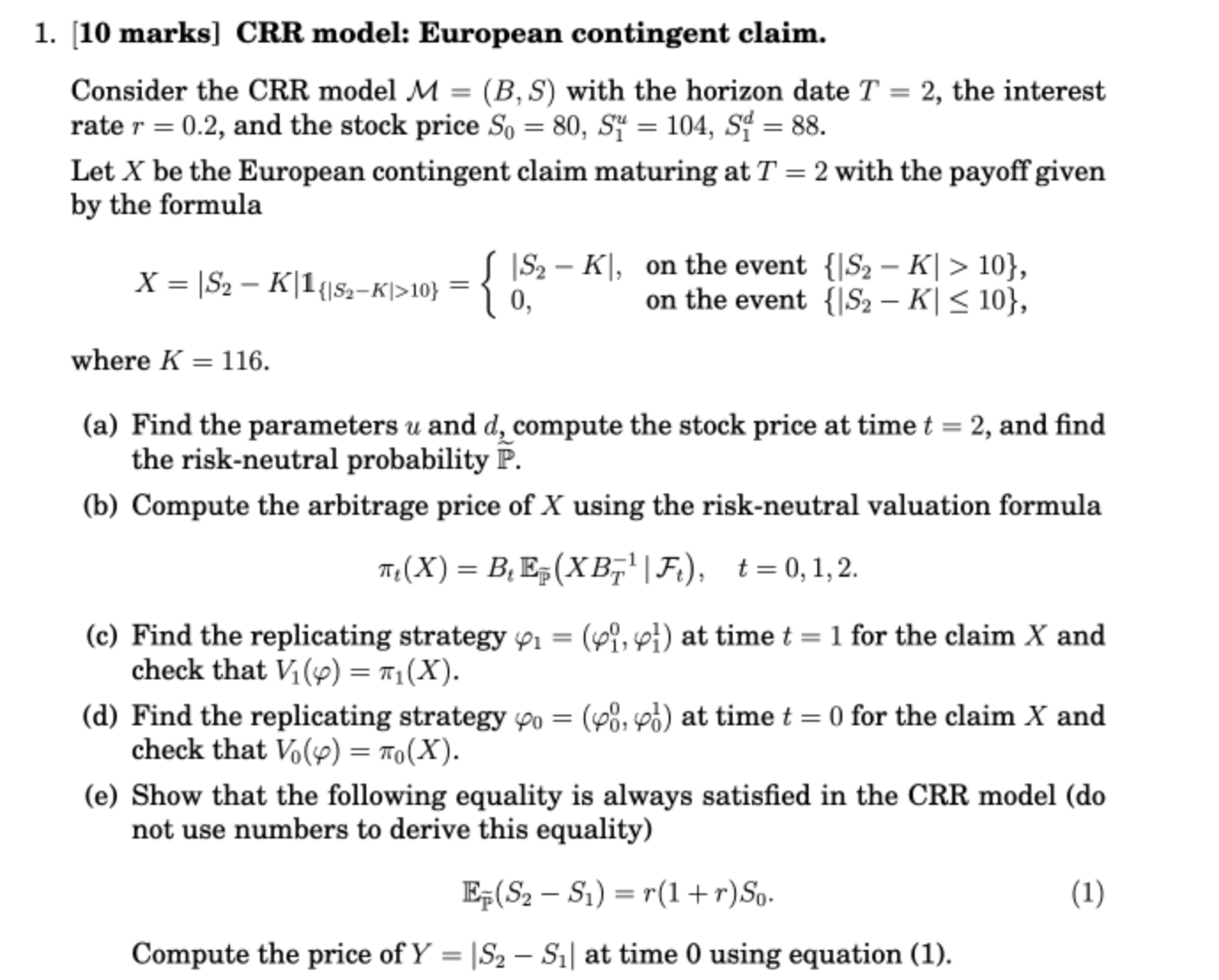

1. [10 marks] CRR model: European contingent claim. Consider the CRR model M = (B, S) with the horizon date T = 2, the interest rate r = 0.2, and the stock price So = 80, Sy = 104, S = 88. by the formula Let X be the European contingent claim maturing at T = 2 with the payoff given X = \\S2 - K|1($2-KI>10} = o, |$2 - K|, on the event {|$2 - K| > 10}, on the event {IS2 - K|

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock