5 B C E F G Complete the steps below using cell references to given data...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

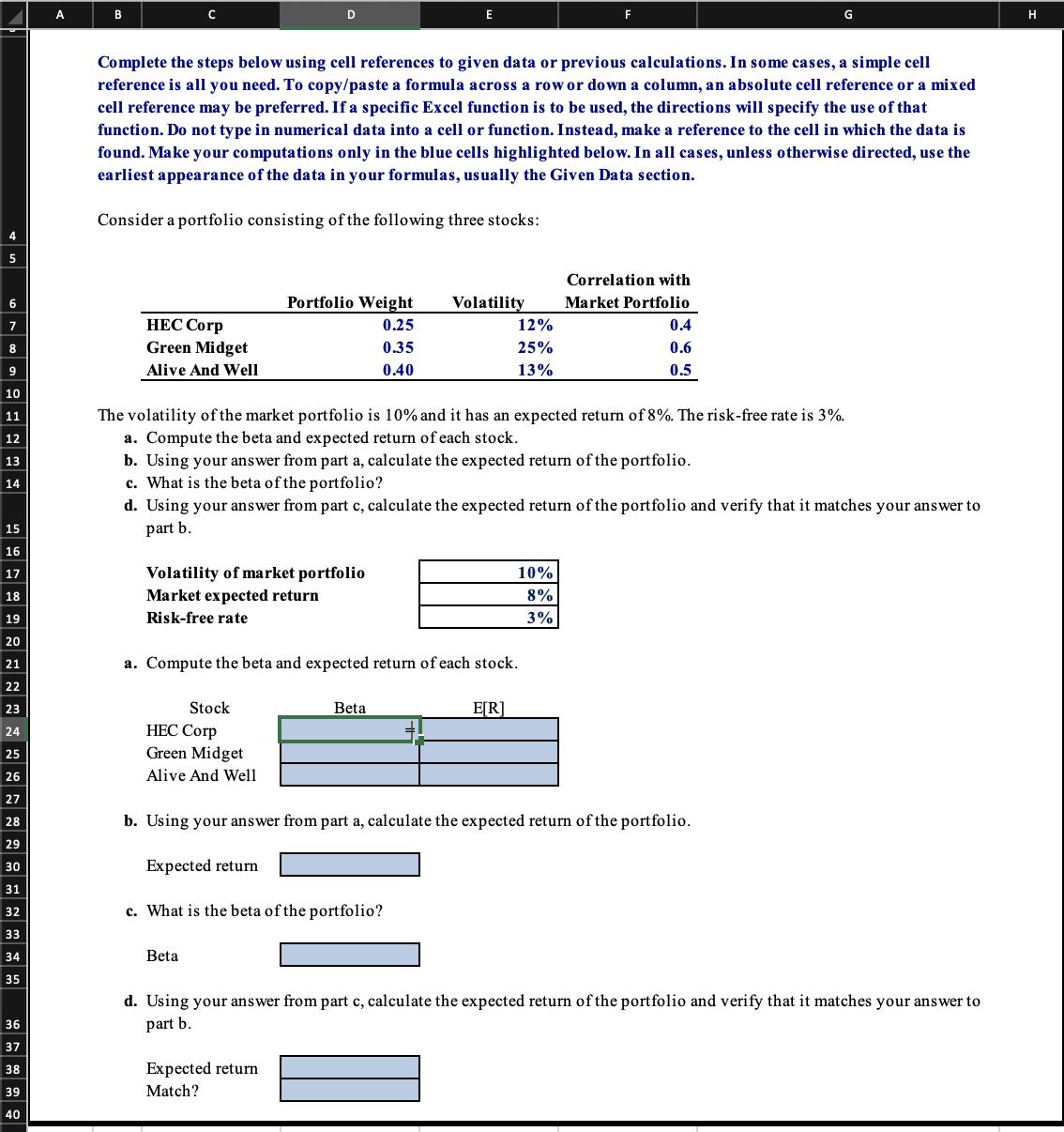

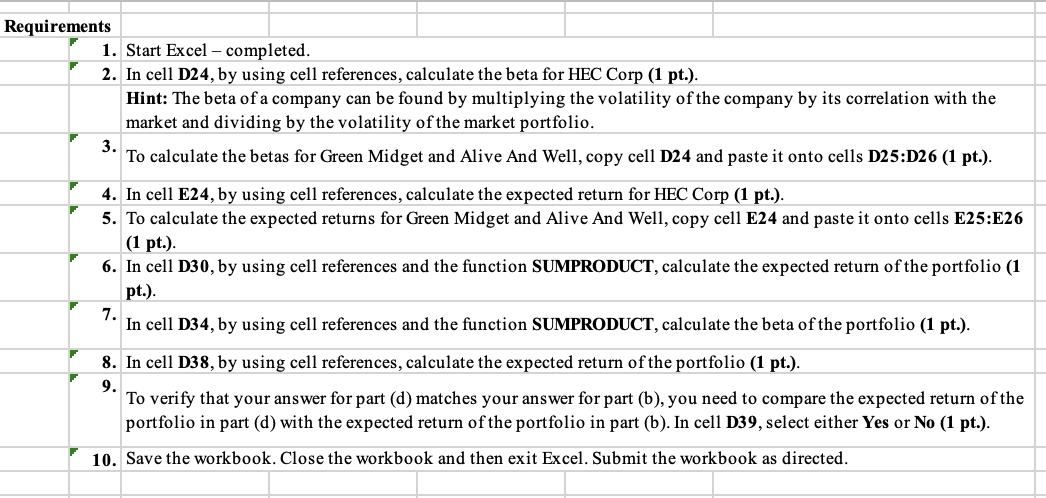

5 B C E F G Complete the steps below using cell references to given data or previous calculations. In some cases, a simple cell reference is all you need. To copy/paste a formula across a row or down a column, an absolute cell reference or a mixed cell reference may be preferred. If a specific Excel function is to be used, the directions will specify the use of that function. Do not type in numerical data into a cell or function. Instead, make a reference to the cell in which the data is found. Make your computations only in the blue cells highlighted below. In all cases, unless otherwise directed, use the earliest appearance of the data in your formulas, usually the Given Data section. Consider a portfolio consisting of the following three stocks: Correlation with 6 Portfolio Weight Volatility Market Portfolio 7 HEC Corp 0.25 12% 0.4 8 Green Midget 0.35 25% 0.6 9 Alive And Well 0.40 13% 0.5 10 11 12 The volatility of the market portfolio is 10% and it has an expected return of 8%. The risk-free rate is 3%. a. Compute the beta and expected return of each stock. 13 b. Using your answer from part a, calculate the expected return of the portfolio. 14 c. What is the beta of the portfolio? d. Using your answer from part c, calculate the expected return of the portfolio and verify that it matches your answer to part b. Volatility of market portfolio Market expected return Risk-free rate a. Compute the beta and expected return of each stock. 10% 8% 3% 15 16 17 18 19 20 21 22 23 Stock 24 HEC Corp 25 Green Midget 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 Beta E[R] Alive And Well b. Using your answer from part a, calculate the expected return of the portfolio. Expected return c. What is the beta of the portfolio? Beta d. Using your answer from part c, calculate the expected return of the portfolio and verify that it matches your answer to part b. Expected return Match? H Requirements 1. Start Excel - completed. 2. In cell D24, by using cell references, calculate the beta for HEC Corp (1 pt.). 3. Hint: The beta of a company can be found by multiplying the volatility of the company by its correlation with the market and dividing by the volatility of the market portfolio. To calculate the betas for Green Midget and Alive And Well, copy cell D24 and paste it onto cells D25:D26 (1 pt.). 4. In cell E24, by using cell references, calculate the expected return for HEC Corp (1 pt.). 5. To calculate the expected returns for Green Midget and Alive And Well, copy cell E24 and paste it onto cells E25:E26 (1 pt.). 6. In cell D30, by using cell references and the function SUMPRODUCT, calculate the expected return of the portfolio (1 pt.). 7. In cell D34, by using cell references and the function SUMPRODUCT, calculate the beta of the portfolio (1 pt.). 8. In cell D38, by using cell references, calculate the expected return of the portfolio (1 pt.). 9. To verify that your answer for part (d) matches your answer for part (b), you need to compare the expected return of the portfolio in part (d) with the expected return of the portfolio in part (b). In cell D39, select either Yes or No (1 pt.). 10. Save the workbook. Close the workbook and then exit Excel. Submit the workbook as directed. 5 B C E F G Complete the steps below using cell references to given data or previous calculations. In some cases, a simple cell reference is all you need. To copy/paste a formula across a row or down a column, an absolute cell reference or a mixed cell reference may be preferred. If a specific Excel function is to be used, the directions will specify the use of that function. Do not type in numerical data into a cell or function. Instead, make a reference to the cell in which the data is found. Make your computations only in the blue cells highlighted below. In all cases, unless otherwise directed, use the earliest appearance of the data in your formulas, usually the Given Data section. Consider a portfolio consisting of the following three stocks: Correlation with 6 Portfolio Weight Volatility Market Portfolio 7 HEC Corp 0.25 12% 0.4 8 Green Midget 0.35 25% 0.6 9 Alive And Well 0.40 13% 0.5 10 11 12 The volatility of the market portfolio is 10% and it has an expected return of 8%. The risk-free rate is 3%. a. Compute the beta and expected return of each stock. 13 b. Using your answer from part a, calculate the expected return of the portfolio. 14 c. What is the beta of the portfolio? d. Using your answer from part c, calculate the expected return of the portfolio and verify that it matches your answer to part b. Volatility of market portfolio Market expected return Risk-free rate a. Compute the beta and expected return of each stock. 10% 8% 3% 15 16 17 18 19 20 21 22 23 Stock 24 HEC Corp 25 Green Midget 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 Beta E[R] Alive And Well b. Using your answer from part a, calculate the expected return of the portfolio. Expected return c. What is the beta of the portfolio? Beta d. Using your answer from part c, calculate the expected return of the portfolio and verify that it matches your answer to part b. Expected return Match? H Requirements 1. Start Excel - completed. 2. In cell D24, by using cell references, calculate the beta for HEC Corp (1 pt.). 3. Hint: The beta of a company can be found by multiplying the volatility of the company by its correlation with the market and dividing by the volatility of the market portfolio. To calculate the betas for Green Midget and Alive And Well, copy cell D24 and paste it onto cells D25:D26 (1 pt.). 4. In cell E24, by using cell references, calculate the expected return for HEC Corp (1 pt.). 5. To calculate the expected returns for Green Midget and Alive And Well, copy cell E24 and paste it onto cells E25:E26 (1 pt.). 6. In cell D30, by using cell references and the function SUMPRODUCT, calculate the expected return of the portfolio (1 pt.). 7. In cell D34, by using cell references and the function SUMPRODUCT, calculate the beta of the portfolio (1 pt.). 8. In cell D38, by using cell references, calculate the expected return of the portfolio (1 pt.). 9. To verify that your answer for part (d) matches your answer for part (b), you need to compare the expected return of the portfolio in part (d) with the expected return of the portfolio in part (b). In cell D39, select either Yes or No (1 pt.). 10. Save the workbook. Close the workbook and then exit Excel. Submit the workbook as directed.

Expert Answer:

Related Book For

Managerial Statistics

ISBN: 9780534389314

1st Edition

Authors: S. Christian Albright, Wayne L. Winston, Christopher Zappe

Posted Date:

Students also viewed these finance questions

-

Shoppers enter Hamilton Place Mall at an average of 120 per hour. What is the probability that at least 35 shoppers will enter the mall between 5:00 and 5:10 pm?

-

The following accounts are used by Mouse Potato, Inc., a computer game maker. Required: For each of the following independent situations, give the journal entry by entering the appropriate code(s)...

-

Which window lists the projects and files included in a solution? a. Object b. Project c. Properties d. Solution Explorer

-

Aaron Reed, a photographer, was in a dispute with Ezelle Investment Properties, Inc., over Ezelle allegedly using one of Reeds photographs without permission. Reed sent Ezelle a cease-and-desist...

-

Wayne Hills Hospital in tiny Wayne, Nebraska, faces a problem common to large, urban hospitals as well as to small, remote ones like itself. That problem is deciding how much of each type of whole...

-

6. Some particles (certain atomic nuclei, and certain mediating particles) have spin 1. This means that in a Stern-Gerlach experiment they yield three measurements: h, 0, -h. This means that now we...

-

1. Analyze your strategies as a project manager (PM) for each of the following project [CO4,C4, risks. Marks:10] Initially, a traditional relational database management system (RDBMS) was used. But...

-

You just opened an online stock trading account. A friend that you trust advises you to put all your money in the stock of one certain company. Its done really well in the past, she states. The stock...

-

How will businesses adjust their production in response to each of the following changes to aggregate expenditure? a. Consumers become more confident in the economic outlook and increase their...

-

You are a purchasing manager for General Electric and need to decide whether you should buy stainless steel from a supplier in China or source it from a foundry in Pittsburgh. If you buy it from the...

-

For each of the following, should you use seasonally adjusted data? Why or why not? a. You are trying to look at economic growth over the past few quarters and you want to figure out the trend so...

-

If a subsidiary sells equipment to its parent and recognizes a loss on sale in the previous year and the loss is not indicative of an impairment loss, which of the following is true? True/False (a) A...

-

The frictionless collar at A has a mass of 25%o. Rope ABC passes over a frictionless pulley at B. Ignoring the size of the frictionless pulley, determine the mass at C. Use components. As always,...

-

Using Apple, demonstrate how the differentiation strategy can be well implemented.

-

A manufacturing company is interested in determining whether a significant difference exists between the variance of the number of units produced per day by one machine operator and the similar...

-

Examine the provided monthly time series data for total U.S. retail sales of building materials (which includes retail sales of building materials, hardware and garden supply stores, and mobile home...

-

The file P13_60.XLS contains data on the price of new and used Taurus sedans. All prices for used cars are from 1995. For example, a new Taurus bought in 1985 cost $11,790 and t wholesale used price...

-

A diffraction grating is a closely spaced array of apertures or obstacles forming a series of closely spaced slits. The simplest type in which an incoming wave front meets alternating opaque and...

-

Find the position of the first minimum for a single slit of width 0.04 \(\mathrm{mm}\) on a screen of \(2 \mathrm{~m}\) distance, when light from a He-Ne laser \(\lambda=\) 6328 is shone on the slit.

-

A GaAs p-n junction has a \(100 \mu \mathrm{m} \times 100 \mathrm{~m}\) cross section and a width of the depletion layer \(W=440 \mathrm{~nm}\). Consider the junction in thermal equilibrium without...

Study smarter with the SolutionInn App