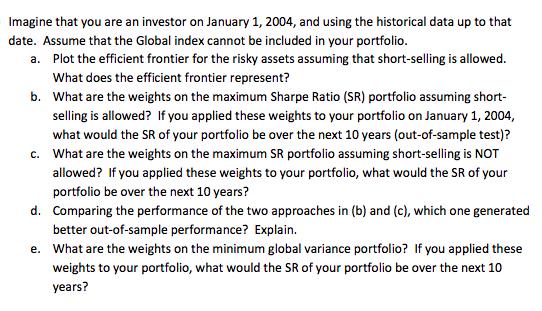

Imagine that you are an investor on January 1, 2004, and using the historical data up...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

Imagine that you are an investor on January 1, 2004, and using the historical data up to that date. Assume that the Global index cannot be included in your portfolio. a. Plot the efficient frontier for the risky assets assuming that short-selling is allowed. What does the efficient frontier represent? b. What are the weights on the maximum Sharpe Ratio (SR) portfolio assuming short- selling is allowed? If you applied these weights to your portfolio on January 1, 2004, what would the SR of your portfolio be over the next 10 years (out-of-sample test)? c. What are the weights on the maximum SR portfolio assuming short-selling is NOT allowed? If you applied these weights to your portfolio, what would the SR of your portfolio be over the next 10 years? d. Comparing the performance of the two approaches in (b) and (c), which one generated better out-of-sample performance? Explain. e. What are the weights on the minimum global variance portfolio? If you applied these weights to your portfolio, what would the SR of your portfolio be over the next 10 years? North Average Return 0.89% Std Dev Var Weights Sum= p* Std Dev Sharpe Average Sharpe Sharpe p STd G* 0.045227095 Averag G* 0.73% 0.36369691 0.043583 0.001899 83.53% 25% 100.00% 0.04427 0.91% 0.514417 Japan 0.23% Asia 0.00% 25% 1.00% Europe 0.060690946 0.060782 0.050854 0.003683391 0.003694 0.002586 16.47% 25% 0.80% 0.00% 25% 0.70% 0.26% Imagine that you are an investor on January 1, 2004, and using the historical data up to that date. Assume that the Global index cannot be included in your portfolio. a. Plot the efficient frontier for the risky assets assuming that short-selling is allowed. What does the efficient frontier represent? b. What are the weights on the maximum Sharpe Ratio (SR) portfolio assuming short- selling is allowed? If you applied these weights to your portfolio on January 1, 2004, what would the SR of your portfolio be over the next 10 years (out-of-sample test)? c. What are the weights on the maximum SR portfolio assuming short-selling is NOT allowed? If you applied these weights to your portfolio, what would the SR of your portfolio be over the next 10 years? d. Comparing the performance of the two approaches in (b) and (c), which one generated better out-of-sample performance? Explain. e. What are the weights on the minimum global variance portfolio? If you applied these weights to your portfolio, what would the SR of your portfolio be over the next 10 years? North Average Return 0.89% Std Dev Var Weights Sum= p* Std Dev Sharpe Average Sharpe Sharpe p STd G* 0.045227095 Averag G* 0.73% 0.36369691 0.043583 0.001899 83.53% 25% 100.00% 0.04427 0.91% 0.514417 Japan 0.23% Asia 0.00% 25% 1.00% Europe 0.060690946 0.060782 0.050854 0.003683391 0.003694 0.002586 16.47% 25% 0.80% 0.00% 25% 0.70% 0.26%

Expert Answer:

Answer rating: 100% (QA)

a The efficient frontier is the set of portfolios that offers the highest expected return for a give... View the full answer

Posted Date:

Students also viewed these accounting questions

-

For this final assignment, imagine that you are an HR Manager on a global HRM planning committee. You are required to present to upper management six (6) main concerns related to global human...

-

Comptroller, horse lady and crook, Part 1 of 2 How one woman (allegedly) embezzled $53 million Henry C. Smith, III, Ph.D., CFE, CMA, CCS; Vincent Alger, Kevin Genter, Nichole Lawhorn, Melissa Lee,...

-

Imagine that you are writing the data link layer software for a line used to send data to you but not from you. The other end uses HDLC, with a 3-bit sequence number and a window size of seven...

-

The following list of balances has been extracted from the records of company cowgale co as of 31 October 2017 the end of the most recent financial year. Notes 1. The balance on the corporation tax...

-

The business-wide overhead recovery rate and the cost-centre overhead recovery rate for Division 1 are, respectively: a) 55.55 and 62.50

-

Shortly after July 31, Morse Corporation received a bank statement containing the following information: December cash transactions and balances on Morse's records are shown in the following...

-

Which of the following is a related party transaction and, under AASB 124/IAS 24, requires disclosure in the annual financial statements? (a) A performance-related amount paid to the directors of the...

-

Using the classification scheme below for a multistep income statement, match each account with the letter of the category in which it belongs. a. Net sales b. Cost of sales c. Selling expenses d....

-

11.A simple LR circuit is connected to a battery at t = 0. The time instant at which rate of energy storage in inductor is half of power delivered by battery 2L (1) In 2 (3) In 2 (2) In (4) (4) In 3

-

For SKIMS by KIM KARDASHIAN Promotional Mix and IMC Tools Identify the key marketing communication methods and specific IMC tools you will use in your marketing campaign. How will you use each of...

-

[V1] 1. [*][**] Let y = Y2 be a random vector distributed as N(, E), where Ly3] 3 -1 [2] =|7| and - 3 3 2 -1 5 Y + y2 2y3 a) What is the distribution of u = b) What is the conditional distribution of...

-

Show that the direct-inverse Fourier transform pair of the correlation of two sequences is \[\sum_{n=-\infty}^{\infty} x_{1}(n) x_{2}(n+l) \longleftrightarrow X_{1}\left(\mathrm{e}^{-\mathrm{j}...

-

A wave traveling along a string has a speed of \(24 \mathrm{~m} / \mathrm{s}\) when the tension in the string is \(120 \mathrm{~N}\). What is the speed of the same wave if the tension is reduced to...

-

One end of a horizontal string that has a linear mass density of \(3.5 \mathrm{~kg} / \mathrm{m}\) is displaced vertically at a speed of \(45 \mathrm{~m} / \mathrm{s}\) for \(6.7 \mathrm{~ms}\). The...

-

Consider two waves \(X\) and \(Y\) traveling in the same medium. The two carry the same amount of energy per unit time, but \(\mathrm{X}\) has half the amplitude of \(\mathrm{Y}\). What is the ratio...

-

You pluck a guitar string so as to produce a standing wave for which \(\lambda=1.3 \mathrm{~m}\). What is the maximum value of the string's displacement at a position \(0.500 \mathrm{~m}\) from the...

-

READ: http://www.nytimes.com/2013/06/22/dining/paula-deen-is-a-no-show-on-today.html http://www.nytimes.com/2013/06/22/dining/paula-deen-is-a-no-show-on-today.html...

-

Explain the circumstances that could result in a long-term bank loan being shown in a statement of financial position as a current liability.

-

An economist believes that the median income of lawyers who recently graduated from law school is more than \(\$ 64,000\). He queries a random sample of 12 lawyers and obtains the accompanying data....

-

The median is different from 120. An analysis of the data reveals that there are 35 minus signs and 28 plus signs. Use the sign test to test the given alternative hypothesis at the \(\alpha=0.05\)...

-

One important variable to consider in trading stock is the daily volume. Volume is measured in number of shares traded in the stock. Stocks with lower volume tend to have more variability in the...

Study smarter with the SolutionInn App