Question: Immunizing a bond portfolio: a. An insurance company must make a payment of $19,487 in seven years. The market interest rate is 10%. You are

Immunizing a bond portfolio: a. An insurance company must make a payment of $19,487 in seven years. The market interest rate is 10%. You are the portfolio manager for the insurance company and you wish to fund this obligation with a three-year zero coupon bond and perpetuities paying annual coupons. How would you immunize the obligation? Step one: Calculate the duration of this liability. To get you started calculate the PV of the obligation. i.e. what is the PV of $19,487 needed in seven years discounted at 10%? The cash flow of this is identical to a zero-coupon bond. So the duration would be determined exactly the same. Step two: Calculate the duration of the asset portfolio. The portfolio duration is the weighted average of duration of each component asset, with weights proportional to the funds placed in each asset. So calculate the duration of the zero-coupon bond, and also the duration of the perpetuity. (the equation for calculating the duration of a perpetuity is (1+y)/y. Where y = market interest rate. What is the duration for each? The fraction of the portfolio invested in the zero coupon is called "w", and the fraction invested in the perpetuity is (1-w) w=weighted proportion. Hint: Asset Duration of the portfolio = ["w" X (duration of the zero-coupon bond)] + [(1-w) X the duration of the perpetuity.] Step three: Find the asset mix that sets the duration of assets equal to the duration of the liability, i.e. the needed payment (7 years) now solve for "w". This gives you the weights to be invested in the zero-coupon bond and the weight needed to be invested in the perpetuity. What are the weights? That is "w" = ? What are the amounts to be invested in the zero-coupon bond and the amount to be invested in the perpetuity? Step four: Fully fund the obligation. You will need to fund the PV of the liability or $10,000. What amount do you need to invest it the zero-coupon bond today? And what amount do you invest in the perpetuity today? 7. Rebalancing the bond portfolio: Now suppose one year has passed, and the market interest rates remain at 10%. You will need to reexamine your portfolio in #6 above. Is the position still fully funded? Is it still immunized? If not, what actions are required? a. Step one: Examine the funding. What is the PV of the liability now? (remember, one year as gone by, so there are only 6 years left in the required $19,487) b. What is the value now of you asset portfolio? (the zero-coupon bond and the perpetuity? That is, how much is the zero-coupon bond now worth? How much have you earned on the perpetuity? What is the amount still invested in the perpetuity? Is the obligation still fully funded? c. The portfolio weights must now be changed given a year has gone by. (the zero-coupon bond has only 2 years left now, while the perpetuity duration remains at 11 years. The obligation is now due in six years. The weights must now satisfy the equation: W X 2 + (1-w) X 11 = 6 yearswhat does "w" equal? To rebalance the portfolio and maintain the duration match, you must now invest a total of ___________ X "w" which equals ________ in the zero-coupon bond. You have earned _____ in interest from the perpetuity, which can be invested in the zero-coupon bond.Is this enough?If not, how much more will you need?_______

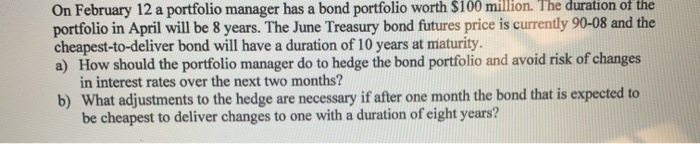

On February 12 a portfolio manager has a bond portfolio worth $100 million. The duration of the portfolio in April will be 8 years. The June Treasury bond futures price is currently 90-08 and the cheapest-to-deliver bond will have a duration of 10 years at maturity. a) How should the portfolio manager do to hedge the bond portfolio and avoid risk of changes in interest rates over the next two months? b) What adjustments to the hedge are necessary if after one month the bond that is expected to be cheapest to deliver changes to one with a duration of eight years?

Step by Step Solution

3.50 Rating (143 Votes )

There are 3 Steps involved in it

To calculate the standard deviation of a portfolio consisting of two stocks we need to take into a... View full answer

Get step-by-step solutions from verified subject matter experts