Question: Implement (in Excel) the Black's formula for European calls and puts on forwards. Calculate the prices of a call and a put using the following

Implement (in Excel) the Black's formula for European calls and puts on forwards.

Calculate the prices of a call and a put using the following assumptions:

F 50

K 50

Volatility 0.4

r 0.05

T- t 0.5

Calculate delta, gamma, rho, vega, and theta using the method of finite differences.

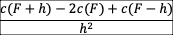

Note: The formula for G of a call option

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock