Question: In 2016, Carson is claimed as a dependent on his parent's tax return. His parents' ordinary income marginal tax rate is 28 percent. Carson's parents

In 2016, Carson is claimed as a dependent on his parent's tax return. His parents' ordinary income marginal tax rate is 28 percent. Carson's parents provided most of his support.

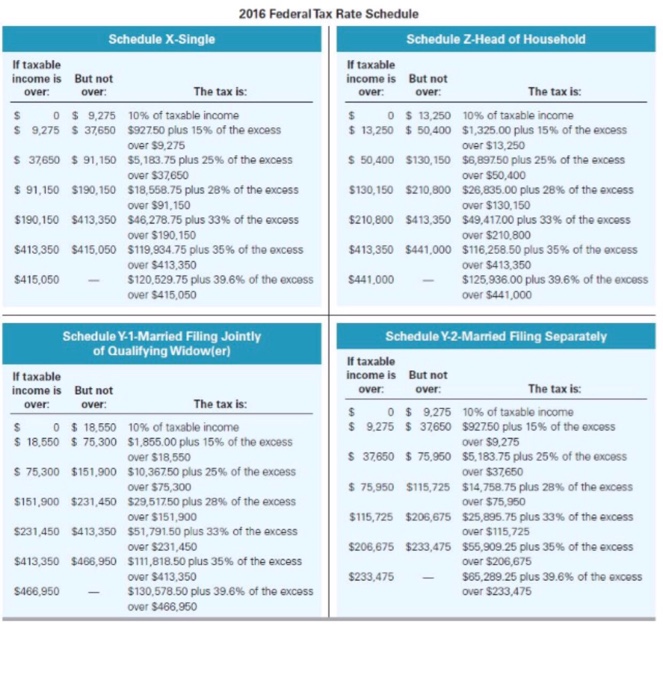

What is Carson's tax liability for the year in the following alternative circumstance? Use Tax Rate Schedule for reference.

a) Carson is 17 years old at year-end and earned $12,000 from his summer job and part-time job after school. This was his only source of income.

b) Carson is 23 years old at year-end. He is a full-time student and earned $12,000 from his summer internship and part-time job. He also received $5,000 of qualified dividend income.

2016 Federal Tax Rate Schedule Schedule X-Single Schedule Z-Head of Household If taxable If taxable income is But not income is But not The tax is: The tax is: over: 0 9,275 10% of taxable income 0 13,250 10% of taxable income 9,275 37650 $92750 plus 15% of the excess 13,250 50,400 $1,325.00 plus 15% of the excess over $9,275 over $13,250 37650 91,150 $5,183.75 plus 25% of the excess 50,400 $130,150 $6.89750 plus 25% of the excess over $37650 over $50,400 91,150 $190,150 $18,558.75 plus 28% of the excess $130,150 $210,800 $26.835.00 plus 28% of the excess over $91,150 over $130,150 $190,150 $413,350 $46.278.75 plus 33% of the excess $210,800 $413,350 $49,41700 plus 33% of the excess over $210,800 over $190,150 $413.350 $415.050 $119,934.75 plus 35% of the excess $413,350 $441,000 $116.258.50 plus 35% of the excess over $413,350 Over $413.350 $415,050 $120,529.75 plus 39.6% of the excess $441.000 $125,936.00 plus 39.6% of the excess over $415.050 over $441.000 Schedule Y 1-Married Filing Jointly Schedule Y 2-Married Filing Separately of Qualifying Widowier) If taxable If taxable income is But not The tax is: income is But not The tax is: over: over: 0 9,275 10% of taxable income 9.275 37650 $92750 plus 15% of the excess 0 18,550 10% of taxable income 18.550 75.300 $1,855.00 plus 15% of the excess over $9.275 37650 75.950 $5.183.75 plus 25% of the excess over $18,550 over $37650 75,300 $151,900 $10,36750 plus 25% of the excess over $75,300 75,950 $115,725 $14,758.75 plus 2B9% of the excess $151,900 $231,450 $29.51750 plus 289% of the excess over $75,950 over $151,900 $115,725 $206,675 $25,895.75 plus 33% of the excess $231,450 $413,350 $51,791.50 plus 339% of the excess over $115,725 over $231,450 $206,675 $233,475 $55,909.25 plus 35% of the excess $413,350 $466,950 $111,818.50 plus 35% of the excess over $206,675 over $413,350 $233,475 $65,289.25 plus 39.6% of the excess $466,950 $130,578.50 plus 39.6% of the excess over $233,475 over $466,950

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts