Question: In a single-index model, the following table gives the expected returns, alphas (a)standard deviation (o), beta () and firm-specific standard deviation (o) for the market,

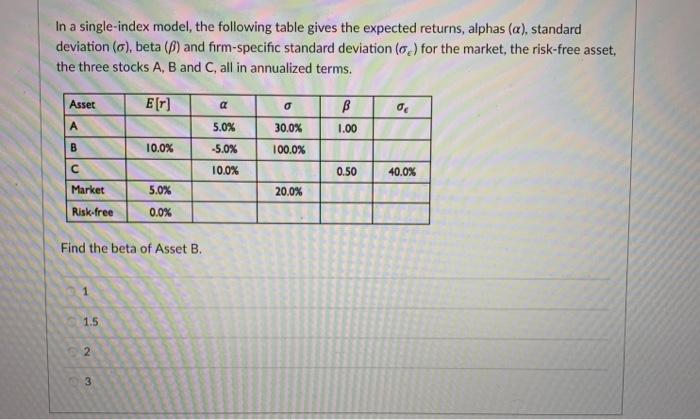

In a single-index model, the following table gives the expected returns, alphas (a)standard deviation (o), beta () and firm-specific standard deviation (o) for the market, the risk-free asset, the three stocks A, B and C, all in annualized terms. Asset E[r] a o B 0 5.0% 30.0% 1.00 B 10.0% -5.0% 100.0% 10.0% 0.50 40.0% Market 5.0% 20.0% Risk-free 0.0% Find the beta of Asset B. 1 1.5 2 3

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock