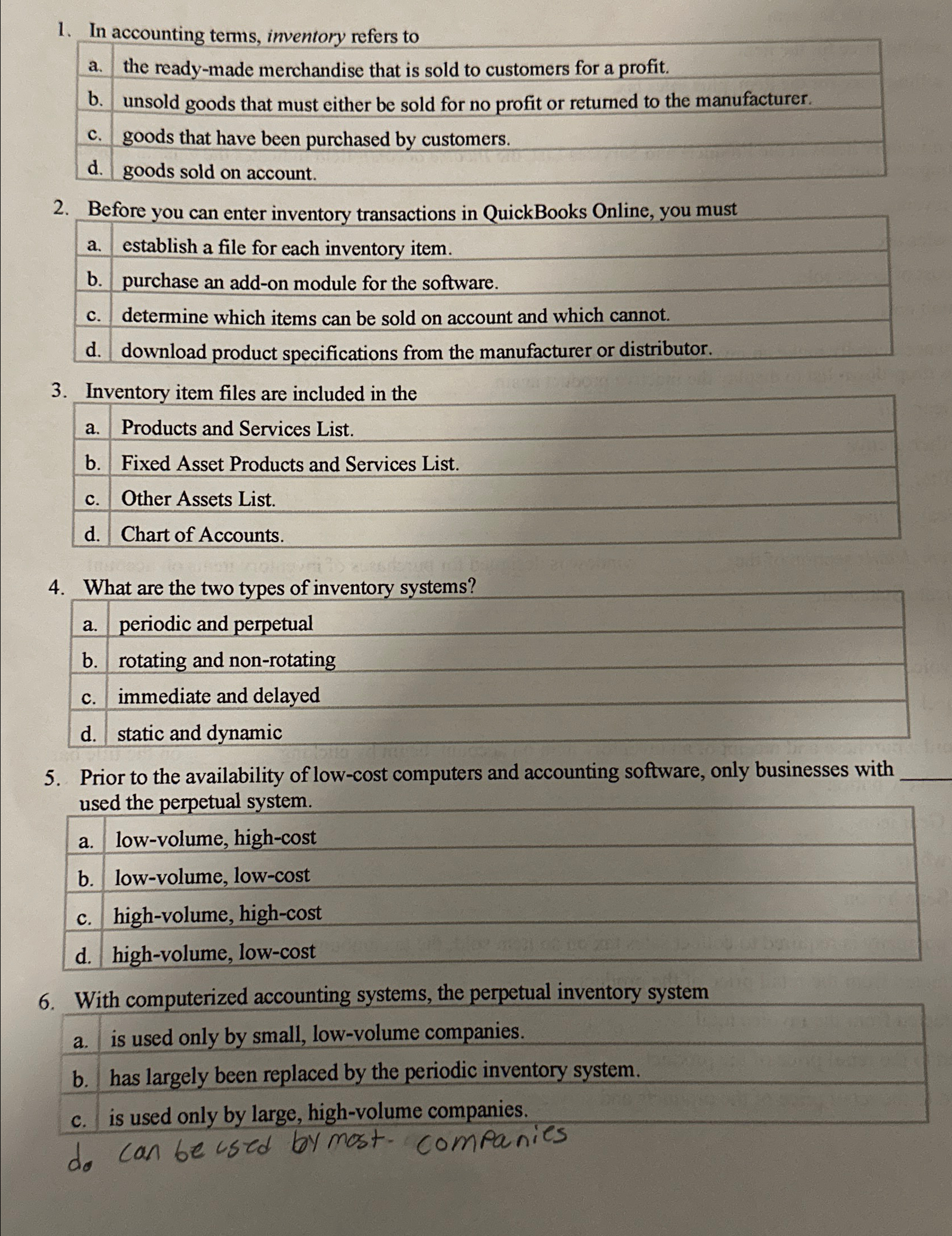

Question: In accounting terms, inventory refers to a . the ready - made merchandise that is sold to customers for a profit. b . unsold goods

In accounting terms, inventory refers to

a the readymade merchandise that is sold to customers for a profit.

b unsold goods that must either be sold for no profit or returned to the manufacturer.

c goods that have been purchased by customers.

d goods sold on account.

Before you can enter inventory transactions in QuickBooks Online, you must

a establish a file for each inventory item.

b purchase an addon module for the software.

c determine which items can be sold on account and which cannot.

d download product specifications from the manufacturer or distributor.

Inventory item files are included in the

a Products and Services List.

b Fixed Asset Products and Services List.

c Other Assets List.

d Chart of Accounts.

What are the two types of inventory systems?

a periodic and perpetual

b rotating and nonrotating

c immediate and delayed

d static and dynamic

Prior to the availability of lowcost computers and accounting software, only businesses with used the perpetual system.

a lowvolume, highcost

b lowvolume, lowcost

c highvolume, highcost

d highvolume, lowcost

With computerized accounting systems, the perpetual inventory system

a is used only by small, lowvolume companies.

b has largely been replaced by the periodic inventory system.

c is used only by large, highvolume companies.

do can be used bymost companies

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock